Activisme : quel bilan en 2018 ?

Bonjour à toutes et à tous, MM. Lipton et Podolsky publient un bel article sur le blogue Harvard Law School Forum on Corporate Governance and Financial Regulation intitulé : « Activism: The State of Play at Year-End 2018 ».

As we noted [in 2018], the threat of activism continues to be high, and has become a global phenomenon. The conclusion of a volatile and dynamic 2018 prompts a brief update of the state of play.

- Activist assets under management remain at elevated levels, encouraging continued attacks on large successful companies in the U.S. and abroad. In many cases, activists have been taking advantage of recent stock market declines to achieve attractive entry points for new positions. These trends have been highlighted in several recent media reports, including in The Wall Street Journal and Bloomberg.

- While the robust M&A environment of much of 2018 has recently subsided, deal-related activism remains prevalent, with activists instigating deal activity, challenging announced transactions (e.g., the “bumpitrage” strategy of pressing for a price increase) and/or pressuring the target into a merger or a private equity deal with the activist itself.

- “Short” activists, who seek to profit from a decline in the target’s market value, remain highly aggressive in both the equity and corporate debt markets. In debt markets, we have also recently seen a rise in “default activism,” where investors purchase debt on the theory that a borrower is already in default and then actively seek to enforce that default in a manner by which they stand to profit.

- Elliott Management was the most active and in many cases aggressive activist of 2018. The Wall Street Journal noted that Elliott has publicly targeted 24 companies in 2018, with Icahn and Starboard runners-up with nine public targets each. The New Yorker published a lengthy profile of Paul Singer and Elliott in August, “Paul Singer, Doomsday Investor”. “Singer has excelled in this field in part because of a canny ability to discern his opponents’ weaknesses and a seeming imperviousness to public disapproval.”

- Enhanced ESG disclosure remains a topic of great interest to institutional investors and the corporate governance community. In October, two prominent business law professors, supported by investors and other entities with over $5 trillion in assets under management, filed a petition for rulemaking calling for the SEC to “develop a comprehensive framework requiring issuers to disclose identified environmental, social, and governance (ESG) aspects of each public-reporting company’s operations.” In November, the Embankment Project of the Coalition for Inclusive Capitalism issued its report outlining proposed ways to measure long-term sustainable value creation beyond financial results. And earlier this month, ESG disclosure was the subject of a lively discussion at a meeting of the SEC’s Investor Advisory Committee, with various views expressed regarding the merits of regulatory efforts versus private ordering in this area.

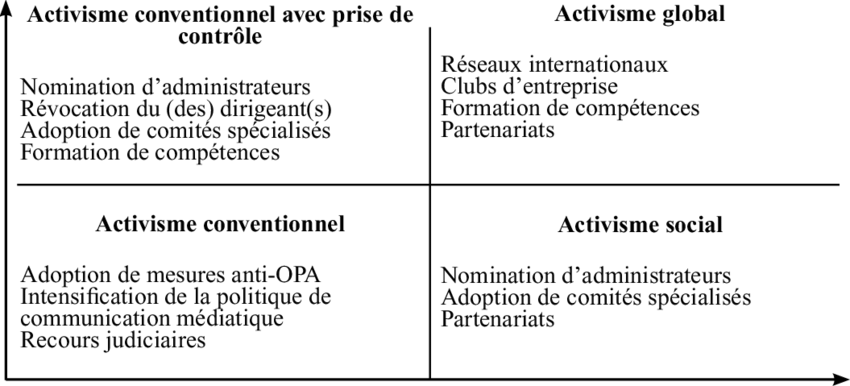

Merci à Jacques Grisé de cette information relayée sur son blogue (ici). Je lui ai emprunté le tableau que vous avez ci-dessus !

À la prochaine…

Ivan

Ce contenu a été mis à jour le 3 octobre 2019 à 12 h 00 min.

Commentaires