Nouvelles diverses | Page 13

actualités internationales engagement et activisme actionnarial Gouvernance

Démocratie actionnariale : bilan de l’AMF France

Ivan Tchotourian 27 novembre 2020 Ivan Tchotourian

Bonjour à toutes et à tous, article intéressant de Les Échos.fr « Les assemblées générales à huis clos ont porté atteinte aux droits des actionnaires » (24 novembre 2020).

Extrait :

Les assemblées générales (AG) 2021 se passeront-elles dans les mêmes conditions que les précédentes ? Les actionnaires qui n’ont cessé de déplorer depuis septembre d’avoir été privés de leurs droits fondamentaux (comme de révoquer ou de nommer un administrateur en séance) aux dernières AG attendent avec impatience l’ordonnance que doit publier le gouvernement . Ce qui ne devrait plus tarder car l’effet du précédent texte prend fin le 30 novembre. Or, une AG est prévue dès le 3 décembre – celle de Bonduelle.

Dans ce contexte, les actionnaires guettaient donc la publication du rapport de l’AMF (Autorité des Marchés Financiers) sur le gouvernement d’entreprise. Car ce rapport revient en détail sur la tenue des AG 2020. Le régulateur en tire « un bilan contrasté. »

À la prochaine…

actualités canadiennes Gouvernance Normes d'encadrement normes de droit

Capital-actions à classe multiple : commentaire de COGECO

Ivan Tchotourian 23 novembre 2020 Ivan Tchotourian

Dans Le Devoir, M. Gérard Bérubé offre une belle analyse du capital-actions à classe multiple pour laquelle il se montre enthousiaste en s’appuyant sur le cas de COGECO : « Sauver nos fleurons » (21 novembre 2020).

Extrait :

Québec peut, certes, envoyer un message clair proclamant la non-disponibilité de nos fleurons clés aux intérêts hors Québec, comme il l’a fait avec Cogeco, mais l’expérience de Rona est venue démontrer la portée limitée du geste. Lors de son premier essai, en 2012, Lowe’s avait

reçu le message clair du gouvernement libéral qu’il n’était pas le bienvenu à la tête de Rona. En 2016, près de quatre ans et un autre essai plus tard, le géant américain a remis cela avec une offre 65 % plus élevée que les actionnaires de Rona ne pouvaient, cette fois, refuser.

Et il restera toujours la taille des sommes en jeu, pouvant rendre difficile d’ériger une position de blocage.

Pour reprendre la position de l’Institut sur la gouvernance (IGOPP), la meilleure protection sera toujours celle de l’actionnariat de contrôle et les structures d’actions à droit de vote multiples. Y greffer une stratégie gouvernementale face aux entreprises à impact systémique dans le respect de cette réalité voulant que le Québec abrite, grosso modo, trois fois plus de prédateurs que de proies viendra renforcer la résistance. Mais la présence de grands investisseurs institutionnels, tels les fonds fiscalisés et la Caisse de dépôt, capables à leur échelle d’accompagner leurs interventions de « clauses québécoises » ou d’orchestrer une position de blocage, est devenue incontournable.

Et François Dauphin, p.-d.g. de l’IGOPP, d’évoquer qu’une dynamique de renouvellement, voire d’élargissement, du portefeuille de « fleurons » au Québec ne peut qu’ajouter à la vitalité.

À la prochaine…

Gouvernance Normes d'encadrement Nouvelles diverses Valeur actionnariale vs. sociétale

Varieties of Shareholderism: Three Views of the Corporate Purpose Cathedral

Ivan Tchotourian 12 novembre 2020 Ivan Tchotourian

À lire cet intéressant article du professeur Licht : Amir Licht, « Varieties of Shareholderism: Three Views of the Corporate Purpose Cathedral », 19 octobre 2020, European Corporate Governance Institute – Law Working Paper No. 547/2020.

Résumé :

This Chapter seeks to make three modest contributions by offering views of the corporate purpose cathedral that bear on the role of law in it. These views underscore the difference and the tension between an individual perspective and a societal/national legal perspective on the purpose of the corporation. First, it reviews a novel dataset on national legal shareholderism – namely, the degree to which national corporate laws endorse shareholder primacy – as an exercise in operationalizing legal constructs. Second, it anchors the two archetypal approaches of shareholderism and takeholderism in personal human values. It is this connection with the fundamental conceptions of the desirable which animates attitudes and choices in this context. The upshot is potentially subversive: Legal injunctions to directors on corporate purpose might be an exercise in futility. Third, this Chapter highlights the importance of acknowledging the tensions between the two levels of analysis by looking at the works of prominent writers. Adolf Berle, Victor Brudney, and Leo Strine have been careful to keep this distinction in mind, which has enabled them to hold multiple views of the cathedral without losing sight of it.

À la prochaine…

actualités canadiennes Gouvernance normes de droit

Droit de parole en assemblée : le MÉDAC mécontent

Ivan Tchotourian 6 novembre 2020 Ivan Tchotourian

Sous le titre suivant « Droit de parole verbal des actionnaires aux assemblées annuelles des sociétés par actions », le MÉDAC a partagé son expérience des dernières assemblées annuelles et son désarroi…

Je reproduis la lettre ci-dessous :

Montréal, vendredi le 30 octobre 2020

Éric Girard, ministre des Finances

390, boulevard Charest Est, 8e étage

Québec (Québec) G1K 3H4

Chrystia Freeland, ministre des Finances

90, rue Elgin

Ottawa (Ontario) K1A 0G5

Madame Freeland, Monsieur Girard, ministres des Finances,

La pandémie frappe le monde entier et il n’est pas possible de savoir quand le régime d’exception actuel prendra fin. Aussi, dans les circonstances, les assemblées annuelles des sociétés par actions, dont toutes les plus grandes, ont lieu virtuellement.

La tenue de pareilles assemblées virtuelles constitue une solution logique aux problèmes engendrés par la rigueur des consignes sanitaires de l’État. Cependant, les principes qui devraient encadrer ces assemblées ne sont pas respectés. Nous en témoignons. Calquer la pratique étasunienne ne suffit certes pas.

L’assemblée annuelle d’une société constitue le socle de sa légitimité quant à la délégation du contrôle de ses affaires aux administrateurs, par les actionnaires. Il en est ainsi depuis plusieurs centaines d’années. L’assemblée annuelle réunit les actionnaires. C’est leur assemblée à eux. Ceux-ci devraient pouvoir y prendre la parole verbalement, sur chaque point à l’ordre du jour. C’était du moins la pratique auparavant.

Les assemblées virtuelles devraient avoir pour objectif de reproduire, le plus fidèlement possible, l’ensemble des caractéristiques essentielles des véritables assemblées en personne, notamment le droit de parole verbal des actionnaires, en priorité.

Or, lors des assemblées virtuelles de cette année, de manière très générale, le droit de parole verbal a été refusé aux actionnaires. Nous le déplorons vivement.

Les Lois et les règlements devraient rendre ce droit de parole verbal explicite, comme il l’est dans la coutume, tel que confirmé dans la jurisprudence et repris par la doctrine. Le déni actuel de ce droit dans la pratique constitue un précédent inacceptable. Il faut agir.

Il s’agit là d’un seul problème parmi tous les autres qui doivent être réglés au sujet des assemblées virtuelles. C’est cependant le problème le plus important, à la source de plusieurs autres. Nous ne sommes pas seuls à penser cela. Par conséquent, nous vous invitons tous les deux à intervenir formellement pour régler la situation.

Nous demeurons bien évidemment disponibles pour discuter du détail de nos positions sur cette question (comme sur plusieurs autres), déjà communiquées à l’Autorité des marchés financiers (AMF), par ailleurs.

Prière d’agréer, Madame la ministre, Monsieur le ministre, notre considération cordiale.

actualités internationales Divulgation Gouvernance normes de droit

Réforme allemande à venir en gouvernance

Ivan Tchotourian 26 octobre 2020 Ivan Tchotourian

Dans Le Monde, Mme Cécile Boutelet propose une belle synthèse de réformes à venir du côté allemand suite au scandale Wirecard : « Après le scandale Wirecard, la finance allemande à la veille d’une profonde réforme » (Le Monde, 26 octobre 2020).

Extrait :

Après les révélations sur l’entreprise, qui avait manipulé son bilan, un projet de loi en discussion souhaite notamment renforcer les pouvoirs du gendarme de la Bourse allemand.

La finance allemande a-t-elle des pratiques malsaines ? Depuis la faillite au mois de juin de l’ancienne star de la finance Wirecard, après qu’elle a reconnu avoir lourdement manipulé son bilan, les révélations sur l’affaire se sont accumulées, soulignant les graves insuffisances du système de contrôle des marchés financiers outre-Rhin. Des manquements qui sont devenus un enjeu politique majeur. Sous pression, le ministre des finances, Olaf Scholz, pousse en faveur d’une réforme rapide du système. Son projet de loi, en discussion depuis mercredi 21 octobre dans les ministères, doit être voté « avant l’été », a-t-il annoncé.

Le texte, porté également par la ministre de la justice, Christine Lambrecht, révèle en creux les limites de l’approche allemande en matière de surveillance des entreprises cotées, et le tournant culturel amorcé par le scandale Wirecard. Le système reposait jusqu’ici sur la responsabilisation et la participation consensuelle des sociétés au processus de contrôle des bilans. L’examen des comptes était confié non pas à la BaFin, le gendarme allemand de la Bourse, mais à une association privée, la DPR (« organisme de contrôle des bilans »), qui disposait de très peu de moyens réels. L’affaire Wirecard a montré l’impuissance de cette approche dans le cas d’une fraude délibérément orchestrée. La future loi doit renforcer considérablement les pouvoirs de la BaFin, qui disposera d’un droit d’investigation pour examiner elle-même les bilans des entreprise

(…) Les cabinets d’audit, dont le manque de zèle à alerter sur les irrégularités de bilan a été mis au jour par le scandale, devront aussi se soumettre à une réforme. Leur mandat au service d’une même entreprise ne pourra excéder dix ans. Le projet de loi exige qu’une séparation plus nette soit faite, au sein de ces cabinets, entre leur activité d’audit et leur activité de conseil, afin d’éviter les conflits d’intérêts.

À la prochaine…

Gouvernance Nouvelles diverses parties prenantes Responsabilité sociale des entreprises

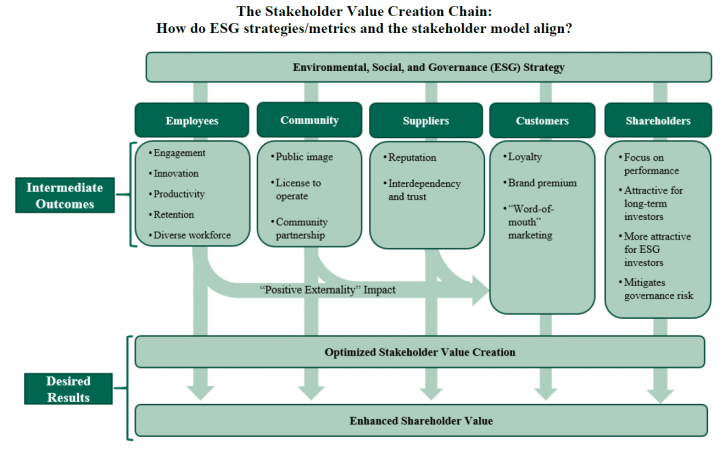

The Stakeholder Model and ESG

Ivan Tchotourian 17 septembre 2020 Ivan Tchotourian

Intéressant article sur l’Harvard Law School Forum on Corporate Governance consacré au modèle partie prenante et à ses liens avec les critères ESG : « The Stakeholder Model and ESG » (Ira Kay, Chris Brindisi et Blaine Martin, 14 septembre 2020).

Extrait :

Is your company ready to set or disclose ESG incentive goals?

ESG incentive metrics are like any other incentive metric: they should support and reinforce strategy rather than lead it. Companies considering ESG incentive metrics should align planning with the company’s social responsibility and environmental strategies, reporting, and goals. Another essential factor in determining readiness is the measurability/quantification of the specific ESG issue.

Companies will generally fall along a spectrum of readiness to consider adopting and disclosing ESG incentive metrics and goals:

- Companies Ready to Set Quantitative ESG Goals: Companies with robust environmental, sustainability, and/or social responsibility strategies including quantifiable metrics and goals (e.g., carbon reduction goals, net zero carbon emissions commitments, Diversity and Inclusion metrics, employee and environmental safety metrics, customer satisfaction, etc.).

- Companies Ready to Set Qualitative Goals: Companies with evolving formalized tracking and reporting but for which ESG matters have been identified as important factors to customers, employees, or other These companies likely already have plans or goals around ESG factors (e.g., LEED [Leadership in Energy and Environmental Design]-certified office space, Diversity and Inclusion initiatives, renewable power and emissions goals, etc.).

- Companies Developing an ESG Strategy: Some companies are at an early stage of developing overall ESG/stakeholder strategies. These companies may be best served to focus on developing a strategy for environmental and social impact before considering linking incentive pay to these priorities.

We note it is critically important that these ESG/stakeholder metrics and goals be chosen and set with rigor in the same manner as financial metrics to ensure that the attainment of the ESG goals will enhance stakeholder value and not serve simply as “window dressing” or “greenwashing.” [9] Implementing ESG metrics is a company-specific design process. For example, some companies may choose to implement qualitative ESG incentive goals even if they have rigorous ESG factor data and reporting.

Will ESG metrics and goals contribute to the company’s value-creation?

The business case for using ESG incentive metrics is to provide line-of-sight for the management team to drive the implementation of initiatives that create significant differentiated value for the company or align with current or emerging stakeholder expectations. Companies must first assess which metrics or initiatives will most benefit the company’s business and for which stakeholders. They must also develop challenging goals for these metrics to increase the likelihood of overall value creation. For example:

- Employees: Are employees and the competitive talent market driving the need for differentiated environmental or social initiatives? Will initiatives related to overall company sustainability (building sustainability, renewable energy use, net zero carbon emissions) contribute to the company being a “best in class” employer? Diversity and inclusion and pay equity initiatives have company and social benefits, such as ensuring fair and equitable opportunities to participate and thrive in the corporate system.

- Customers: Are customer preferences driving the need to differentiate on sustainable supply chains, social justice initiatives, and/or the product/company’s environmental footprint?

- Long-Term Sustainability: Are long-term macro environmental factors (carbon emissions, carbon intensity of product, etc.) critical to the Company’s ability to operate in the long term?

- Brand Image: Does a company want to be viewed by all constituencies, including those with no direct economic linkage, as a positive social and economic contributor to society?

There is no one-size-fits-all approach to ESG metrics, and companies fall across a spectrum of needs and drivers that affect the type of ESG factors that are relevant to short- and long-term business value depending on scale, industry, and stakeholder drivers. Most companies have addressed, or will need to address, how to implement ESG/stakeholder considerations in their operating strategy.

Conceptual Design Parameters for Structuring Incentive Goals

For those companies moving to implement stakeholder/ESG incentive goals for the first time, the design parameters range widely, which is not different than the design process for implementing any incentive metric. For these companies, considering the following questions can help move the prospect of an ESG incentive metric from an idea to a tangible goal with the potential to create value for the company:

- Quantitative goals versus qualitative milestones. The availability and quality of data from sustainability or social responsibility reports will generally determine whether a company can set a defined quantitative goal. For other companies, lack of available ESG data/goals or the company’s specific pay philosophy may mean ESG initiatives are best measured by setting annual milestones tailored to selected goals.

- Selecting metrics aligned with value creation. Unlike financial metrics, for which robust statistical analyses can help guide the metric selection process (e.g., financial correlation analysis), the link between ESG metrics and company value creation is more nuanced and significantly impacted by industry, operating model, customer and employee perceptions and preferences, etc. Given this, companies should generally apply a principles-based approach to assess the most appropriate metrics for the company as a whole (e.g., assessing significance to the organization, measurability, achievability, etc.) Appendix 1 provides a list of common ESG metrics with illustrative mapping to typical stakeholder impact.

- Determining employee participation. Generally, stakeholder/ESG-focused metrics would be implemented for officer/executive level roles, as this is the employee group that sets company-wide policy impacting the achievement of quantitative ESG goals or qualitative milestones. Alternatively, some companies may choose to implement firm-wide ESG incentive metrics to reinforce the positive employee engagement benefits of the company’s ESG strategy or to drive a whole-team approach to achieving goals.

- Determining the range of metric weightings for stakeholder/ESG goals. Historically, US companies with existing environmental, employee safety, and customer service goals as well as other stakeholder metrics have been concentrated in the extractive, industrial, and utility industries; metric weightings on these goals have ranged from 5% to 20% of annual incentive scorecards. We expect that this weighting range would continue to apply, with the remaining 80%+ of annual incentive weighting focused on financial metrics. Further, we expect that proxy advisors and shareholders may react adversely to non-financial metrics weighted more than 10% to 20% of annual incentive scorecards.

- Considering whether to implement stakeholder/ESG goals in annual versus long-term incentive plans. As noted above, most ESG incentive goals to date have been implemented as weighted metrics in balanced scorecard annual incentive plans for several reasons. However, we have observed increased discussion of whether some goals (particularly greenhouse gas emission goals) may be better suited to long-term incentives. [10] There is no right answer to this question—some milestone and quantitative goals are best set on an annual basis given emerging industry, technology, and company developments; other companies may have a robust long-term plan for which longer-term incentives are a better fit.

- Considering how to operationalize ESG metrics into long-term plans. For companies determining that sustainability or social responsibility goals fit best into the framework of a long-term incentive, those companies will need to consider which vehicles are best to incentivize achievement of strategically important ESG goals. While companies may choose to dedicate a portion of a 3-year performance share unit plan to an ESG metric (e.g., weighting a plan 40% relative total shareholder return [TSR], 40% revenue growth, and 20% greenhouse gas reduction), there may be concerns for shareholders and/or participants in diluting the financial and shareholder-value focus of these incentives. As an alternative, companies could grant performance restricted stock units, vesting at the end of a period of time (e.g., 3 or 4 years) contingent upon achievement of a long-term, rigorous ESG performance milestone. This approach would not “dilute” the percentage of relative TSR and financial-based long-term incentives, which will remain important to shareholders and proxy advisors.

Conclusion

As priorities of stakeholders continue to evolve, and addressing these becomes a strategic imperative, companies may look to include some stakeholder metrics in their compensation programs to emphasize these priorities. As companies and Compensation Committees discuss stakeholder and ESG-focused incentive metrics, each organization must consider its unique industry environment, business model, and cultural context. We interpret the BRT’s updated statement of business purpose as a more nuanced perspective on how to create value for all stakeholders, inclusive of shareholders. While optimizing profits will remain the business purpose of corporations, the BRT’s statement provides support for prioritizing the needs of all stakeholders in driving long-term, sustainable success for the business. For some companies, implementing incentive metrics aligned with this broader context can be an important tool to drive these efforts in both the short and long term. That said, appropriate timing, design, and communication will be critical to ensure effective implementation.

À la prochaine…

actualités internationales Gouvernance Normes d'encadrement parties prenantes Responsabilité sociale des entreprises

Pour un comité social et éthique en matière de gouvernance

Ivan Tchotourian 17 septembre 2020 Ivan Tchotourian

Dans BoardAgenda, Gavin Hinks propose une solution pour que les parties prenantes soient mieux pris en compte : la création d’un comité social et éthique (déjà en fonction en Afrique du Sud) : « Companies ‘need new mechanism’ to integrate stakeholder interests » (4 septembre 2020).

Extrait :

While section 172 of the Companies Act—the key law governing directors’ duties—has been sufficiently flexible to enable companies to re-align themselves with stakeholders so far, it provides no guarantee they will maintain that disposition.

In their recent paper, MacNeil and Esser argue more regulation is needed and in particular a mandatory committee drawing key stakeholder issues to the board and then reporting on them to shareholders.

Known as the “social and ethics committee” in South Africa, a similar mandatory committee in the UK considering ESG (environmental, social and governance) issues “will provide a level playing field for stakeholder engagement,” write MacNeil and Esser.

Recent evidence, they concede, suggests the committees in South Africa are still evolving, but there are advantages, with the committee “uniquely placed with direct access to the main board and a mandate to reach into the depths of the business”.

“As a result, it is capable of having a strong influence on the way a company heads down the path of sustained value creation.”

Will stakeholderism stick?

The issue of making “stakeholder” capitalism stick has vexed others too. The issue was a dominant agenda item at the World Economic Forum’s Davos conference this year, as well as becoming a key element in the presidential campaign of Democrat candidate Joe Biden.

Others worry that stakeholderism is a talking point only, prompting no real change in some companies. Indeed, when academics examined the practical policy outcomes from the now famous 2019 pledge by the Business Roundtable—a group of US multinationals—to shift their focus from shareholders to stakeholders, they found the companies wanting.

In the UK, at least, some are taking the issue very seriously. The Institute of Directors recently launched a new governance centre with its first agenda item being how stakeholderism can be integrated into current governance structures.

Further back the Royal Academy, an august British research institution, issued its own principles for becoming a “purposeful business”, another idea closely associated with stakeholderism.

The stakeholder debate has a long way to run. If the idea is to gain traction it will undoubtedly need a stronger commitment in regulation than it currently has, or companies could easily wander from the path. That may depend on public demand and political will. But Esser and MacNeil may have at least indicated one way forward.

À la prochaine…