Fifty years ago, Milton Friedman in the New York Times magazine proclaimed that the social responsibility of business is to increase its profits. Directors have the duty to do what is in the interests of their masters, the shareholders, to make as much profit as possible. Friedman was hostile to the New Deal and European models of social democracy and urged business to use its muscle to reduce the effectiveness of unions, blunt environmental and consumer protection measures, and defang antitrust law. He sought to reduce consideration of human concerns within the corporate boardroom and legal requirements on business to treat workers, consumers, and society fairly.

Over the last 50 years, Friedman’s views became increasingly influential in the U.S. As a result, the power of the stock market and wealthy elites soared and consideration of the interests of workers, the environment, and consumers declined. Profound economic insecurity and inequality, a slow response to climate change, and undermined public institutions resulted. Using their wealth and power in the pursuit of profits, corporations led the way in loosening the external constraints that protected workers and other stakeholders against overreaching.

Under the dominant Friedman paradigm, corporations were constantly harried by all the mechanisms that shareholders had available—shareholder resolutions, takeovers, and hedge fund activism—to keep them narrowly focused on stockholder returns. And pushed by institutional investors, executive remuneration systems were increasingly focused on total stock returns. By making corporations the playthings of the stock market, it became steadily harder for corporations to operate in an enlightened way that reflected the real interests of their human investors in sustainable growth, fair treatment of workers, and protection of the environment.

Half a century later, it is clear that this narrow, stockholder-centered view of corporations has cost society severely. Well before the COVID-19 pandemic, the single-minded focus of business on profits was criticized for causing the degradation of nature and biodiversity, contributing to global warming, stagnating wages, and exacerbating economic inequality. The result is best exemplified by the drastic shift in gain sharing away from workers toward corporate elites, with stockholders and top management eating more of the economic pie.

Corporate America understood the threat that this way of thinking was having on the social compact and reacted through the 2019 corporate purpose statement of the Business Roundtable, emphasizing responsibility to stakeholders as well as shareholders. But the failure of many of the signatories to protect their stakeholders during the coronavirus pandemic has prompted cynicism about the original intentions of those signing the document, as well as their subsequent actions.

Stockholder advocates are right when then they claim that purpose statements on their own achieve little: Calling for corporate executives who answer to only one powerful constituency—stockholders in the form of highly assertive institutional investors—and have no legal duty to other stakeholders to run their corporations in a way that is fair to all stakeholders is not only ineffectual, it is naive and intellectually incoherent.

What is required is to match commitment to broader responsibility of corporations to society with a power structure that backs it up. That is what has been missing. Corporate law in the U.S. leaves it to directors and managers subject to potent stockholder power to give weight to other stakeholders. In principle, corporations can commit to purposes beyond profit and their stakeholders, but only if their powerful investors allow them to do so. Ultimately, because the law is permissive, it is in fact highly restrictive of corporations acting fairly for all their stakeholders because it hands authority to investors and financial markets for corporate control.

Absent any effective mechanism for encouraging adherence to the Roundtable statement, the system is stacked against those who attempt to do so. There is no requirement on corporations to look after their stakeholders and for the most part they do not, because if they did, they would incur the wrath of their shareholders. That was illustrated all too clearly by the immediate knee-jerk response of the Council of Institutional Investors to the Roundtable declaration last year, which expressed its disapproval by stating that the Roundtable had failed to recognize shareholders as owners as well as providers of capital, and that “accountability to everyone means accountability to no one.”

If the Roundtable is serious about shifting from shareholder primacy to purposeful business, two things need to happen. One is that the promise of the New Deal needs to be renewed, and protections for workers, the environment, and consumers in the U.S. need to be brought closer to the standards set in places like Germany and Scandinavia.

But to do that first thing, a second thing is necessary. Changes within company law itself must occur, so that corporations are better positioned to support the restoration of that framework and govern themselves internally in a manner that respects their workers and society. Changing the power structure within corporate law itself—to require companies to give fair consideration to stakeholders and temper their need to put profit above all other values—will also limit the ability and incentives for companies to weaken regulations that protect workers, consumers, and society more generally.

To make this change, corporate purpose has to be enshrined in the heart of corporate law as an expression of the broader responsibility of corporations to society and the duty of directors to ensure this. Laws already on the books of many states in the U.S. do exactly that by authorizing the public benefit corporation (PBC). A PBC has an obligation to state a public purpose beyond profit, to fulfill that purpose as part of the responsibilities of its directors, and to be accountable for so doing. This model is meaningfully distinct from the constituency statutes in some states that seek to strengthen stakeholder interests, but that stakeholder advocates condemn as ineffectual. PBCs have an affirmative duty to be good corporate citizens and to treat all stakeholders with respect. Such requirements are mandatory and meaningful, while constituency statutes are mushy.

The PBC model is growing in importance and is embraced by many younger entrepreneurs committed to the idea that making money in a way that is fair to everyone is the responsible path forward. But the model’s ultimate success depends on longstanding corporations moving to adopt it.

Even in the wake of the Roundtable’s high-minded statement, that has not yet happened, and for good reason. Although corporations can opt in to become a PBC, there is no obligation on them to do so and they need the support of their shareholders. It is relatively easy for founder-owned companies or companies with a relatively low number of stockholders to adopt PBC forms if their owners are so inclined. It is much tougher to obtain the approval of a dispersed group of institutional investors who are accountable to an even more dispersed group of individual investors. There is a serious coordination problem of achieving reform in existing corporations.

That is why the law needs to change. Instead of being an opt-in alternative to shareholder primacy, the PBC should be the universal standard for societally important corporations, which should be defined as ones with over $1 billion of revenues, as suggested by Sen. Elizabeth Warren. In the U.S., this would be done most effectively by corporations becoming PBCs under state law. The magic of the U.S. system has rested in large part on cooperation between the federal government and states, which provides society with the best blend of national standards and nimble implementation. This approach would build on that.

Corporate shareholders and directors enjoy substantial advantages and protections through U.S. law that are not extended to those who run their own businesses. In return for offering these privileges, society can reasonably expect to benefit, not suffer, from what corporations do. Making responsibility in society a duty in corporate law will reestablish the legitimacy of incorporation.

There are three pillars to this. The first is that corporations must be responsible corporate citizens, treating their workers and other stakeholders fairly, and avoiding externalities, such as carbon emissions, that cause unreasonable or disproportionate harm to others. The second is that corporations should seek to make profit by benefiting others. The third is that they should be able to demonstrate that they fulfill both criteria by measuring and reporting their performances against them.

The PBC model embraces all three elements and puts legal, and thus market, force behind them. Corporate managers, like most of us, take obligatory duties seriously. If they don’t, the PBC model allows for courts to issue orders, such as injunctions, holding corporations to their stakeholder and societal obligations. In addition, the PBC model requires fairness to all stakeholders at all stages of a corporation’s life, even when it is sold. The PBC model shifts power to socially responsible investment and index funds that focus on the long term and cannot gain from unsustainable approaches to growth that harm society.

Our proposal to amend corporate law to ensure responsible corporate citizenship will prompt a predictable outcry from vested interests and traditional academic quarters, claiming that it will be unworkable, devastating for entrepreneurship and innovation, undermine a capitalist system that has been an engine for growth and prosperity, and threaten jobs, pensions, and investment around the world. If putting the purpose of a business at the heart of corporate law does all of that, one might well wonder why we invented the corporation in the first place.

Of course, it will do exactly the opposite. Putting purpose into law will simplify, not complicate, the running of businesses by aligning what the law wants them to do with the reason why they are created. It will be a source of entrepreneurship, innovation, and inspiration to find solutions to problems that individuals, societies, and the natural world face. It will make markets and the capitalist system function better by rewarding positive contributions to well-being and prosperity, not wealth transfers at the expense of others. It will create meaningful, fulfilling jobs, support employees in employment and retirement, and encourage investment in activities that generate wealth for all.

We are calling for the universal adoption of the PBC for large corporations. We do so to save our capitalist system and corporations from the devastating consequences of their current approaches, and for the sake of our children, our societies, and the natural world.

Dans un article du Financial Times (« European companies were more keen to cut divis than executive pay », 9 septembre 2020), il est observé que les assemblées annuelles de grandes entreprises européennes montrent des disparités concernant la protection des salariés et la réduction des dividendes.

Extrait :

Businesses in Spain, Italy, the Netherlands and the UK were more likely to cut dividends than executive pay this year, despite calls from shareholders for bosses to share the financial pain caused by the pandemic.

More than half of Spanish businesses examined by Georgeson, a corporate governance consultancy, cancelled, postponed or reduced dividends in 2020. Only 29 per cent introduced a temporary reduction in executive pay. In Italy, 44 per cent of companies changed their dividend policies because of Covid-19, but just 29 per cent cut pay for bosses, according to the review of the annual meeting season in Europe.

This disparity between protection of salaries and bonuses at the top while shareholders have been hit with widespread dividend cuts is emerging as a flashpoint for investors. Asset managers such as Schroders and M&G have spoken out about the need for companies to show restraint on pay if they are cutting dividends or receiving government support. “Executive remuneration remains a key focal point for investors and was amongst the most contested resolutions in the majority of the markets,” said Georgeson’s Domenic Brancati.

But he added that despite this focus, shareholder revolts over executive pay had fallen slightly across Europe compared with 2019 — suggesting that investors were giving companies some leeway on how they dealt with the pandemic. Investors could become more vocal about this issue next year, he said.

One UK-based asset manager said it was “still having lots of conversations with companies around pay” but for this year had decided not to vote against companies on the issue. But it added the business would watch remuneration and dividends closely next year.

Companies around the world have cut or cancelled dividends in response to the crisis, hitting income streams for many investors. According to Janus Henderson, global dividends had their biggest quarterly fall in a decade during the second quarter, with more than $100bn wiped off their value. The Georgeson data shows that almost half of UK companies changed their dividend payout, while less than 45 per cent altered executive remuneration. In the Netherlands, executive pay took a hit at 29 per cent of companies, while 34 per cent adjusted dividends. In contrast, a quarter of Swiss executives were hit with a pay cut but only a fifth of companies cut or cancelled their dividend.

The Georgeson research also found that the pandemic had a significant impact on the AGM process across Europe, with many companies postponing their annual meetings or stopping shareholders from voting during the event.

Business, and the dominant legal form of business, that is, the corporation, must be involved in the transition to sustainability, if we are to succeed in securing a safe and just space for humanity. The corporate board has a crucial role in determining the strategy and the direction of the corporation. However, currently, the function of the corporate board is constrained through the social norm of shareholder primacy, reinforced through the intermediary structures of capital markets. This article argues that an EU law reform is key to integrating sustainability into mainstream corporate governance, into the corporate purpose and the core duties of the corporate board, to change corporations from within. While previous attempts at harmonizing core corporate law at the EU level have failed, there are now several drivers for reform that may facilitate a change, including the EU Commission’s increased emphasis on sustainability. Drawing on this momentum, this article presents a proposal to reform corporate purpose and duties of the board, based on the results of the EU-funded research project, Sustainable Market Actors for Responsible Trade (SMART, 2016–2020).

Le High Pay Centre anglais vient de publier son rapport 2019 sur la rémunération des hauts dirigeants : « HPC/CIPD Annual FTSE 100 CEO Pay Review – CEO pay flat in 2019 ». Je vous laisse découvrir les chiffres, mais j’attire votre attention sur les conséquences de la COVID-19.

Extrait :

Covid-19 pay cuts

36 FTSE 100 companies have announced cuts to executive pay in response to the COVID-19 crisis and economic downturn.

While most of the 36 companies have used a combination of measures to cut pay, the report suggests these are mainly superficial or short-term. The most common measure, taken by 14 companies, has been to cut salaries at the top by 20%. However, salaries typically only make up a small part of a FTSE 100 CEO’s total pay package.

11 companies have cancelled Short-Term Incentive Plans (STIPs) for their CEOs while two other firms have deferred salary increases for their CEOs. None of the 36 companies have chosen to reduce their CEO’s Long-Term Incentive Plan (LTIP), which typically makes up half of a CEO’s total pay package.

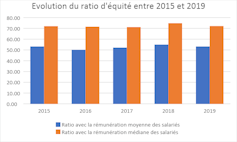

Bel article de Vanessa Serret et Mohamed Khemissi dans The conversation (27 juillet 2020) : « Rémunération des dirigeants : la transparence ne fait pas tout ». Cet article revient sur le ratio d’équité : non seulement son utilité, mais encore son niveau (20 ? 100 ?…)

Le ratio d’équité apprécie l’écart entre la rémunération de chaque dirigeant et le salaire (moyen et médian) des salariés à temps plein de son entreprise. Il est prévu un suivi de l’évolution de ce ratio au cours des cinq derniers exercices et sa mise en perspective avec la performance financière de la société. Ces comparaisons renseignent sur la dynamique du partage de la création de valeur entre le dirigeant et les salariés.

(…)

Un premier état des lieux

Sur la base des rémunérations versées en 2019 par les entreprises composant l’indice boursier du CAC 40, les patrons français ont perçu un salaire moyen de 5 millions d’euros, soit une baisse de 9,1 % par rapport à 2018.

Évolution du ratio d’équité par rapport à la rémunération moyenne (bleu) et médiane (orange) des salariés de 2015 à 2019. auteurs

Ce chiffre représente 53 fois la rémunération moyenne de leurs employés (72 fois la rémunération médiane) : un ratio acceptable, selon l’agence de conseil en vote Proxinvest. En effet, selon cette agence, et afin de garantir la cohésion sociale au sein de l’entreprise, le ratio d’équité ne doit pas dépasser 100 (par rapport à la rémunération moyenne des salariés).

Deux dirigeants s’attribuent néanmoins des rémunérations qui dépassent le maximum socialement tolérable à savoir Bernard Charlès, vice-président du conseil d’administration et directeur général de Dassault Systèmes et Paul Hudson, directeur général de Sanofi avec un ratio d’équité qui s’établit respectivement de 268 et de 107.

Notons également que pour les deux sociétés publiques appartenant à l’indice boursier du CAC 40, le ratio d’équité dépasse le plafond de 20 (35 pour Engie et 38 pour Orange) fixé par le décret n° 2012-915 du 26 juillet 2012, relatif au contrôle de l’État sur les rémunérations des dirigeants d’entreprises publiques.

La gouvernance des banques est souvent dans l’ombre de la gouvernance des entreprises. Pourtant, en cette période post COVID-19, il sa passe des choses intéressantes comme en témoigne cet article : « Ni dividendes, ni rachats d’actions, préconise la BCE » (Thierry Labro, PaperJam).

Extrait :

La Banque centrale européenne (BCE) a étendu, mardi, sa recommandation aux banques sur les distributions de dividendes et les rachats d’actions jusqu’au 1er janvier 2021 et demandé aux banques d’être extrêmement modérées en matière de rémunération variable. Dans un communiqué , elle a également précisé que «cela donnerait suffisamment de temps aux banques pour reconstituer leurs coussins de fonds propres et de liquidités afin de ne pas agir de manière procyclique».

Un nouvel examen de la situation sera fait au quatrième trimestre, et, si tout va «bien», les banques dont les fonds propres sont suffisants pourront reprendre le paiement des dividendes, dit-elle.

Elle appelle aussi les dirigeants à revoir la rémunération variable et à préférer les paiements en actions propres, par exemple.

Excellente lecture ce matin de ce billet du Harvard Law School Forum on Corporate Governance : « Legal Liability for ESG Disclosures » (de Connor Kuratek, Joseph A. Hall et Betty M. Huber, 3 août 2020). Dans cette publication, vous trouverez non seulement une belle synthèse des référentiels actuels, mais aussi une réflexion sur les conséquences attachées à la mauvaise divulgation d »information.

Extrait :

3. Legal Liability Considerations

Notwithstanding the SEC’s position that it will not—at this time—mandate additional climate or ESG disclosure, companies must still be mindful of the potential legal risks and litigation costs that may be associated with making these disclosures voluntarily. Although the federal securities laws generally do not require the disclosure of ESG data except in limited instances, potential liability may arise from making ESG-related disclosures that are materially misleading or false. In addition, the anti-fraud provisions of the federal securities laws apply not only to SEC filings, but also extend to less formal communications such as citizenship reports, press releases and websites. Lastly, in addition to potential liability stemming from federal securities laws, potential liability could arise from other statutes and regulations, such as federal and state consumer protection laws.

A. Federal Securities Laws

When they arise, claims relating to a company’s ESG disclosure are generally brought under Section 11 of the Securities Act of 1933, which covers material misstatements and omissions in securities offering documents, and under Section 10(b) of the Securities Exchange Act of 1934 and rule 10b-5, the principal anti-fraud provisions. To date, claims brought under these two provisions have been largely unsuccessful. Cases that have survived the motion to dismiss include statements relating to cybersecurity (which many commentators view as falling under the “S” or “G” of ESG), an oil company’s safety measures, mine safety and internal financial integrity controls found in the company’s sustainability report, website, SEC filings and/or investor presentations.

Interestingly, courts have also found in favor of plaintiffs alleging rule 10b-5 violations for statements made in a company’s code of conduct. Complaints, many of which have been brought in the United States District Court for the Southern District of New York, have included allegations that a company’s code of conduct falsely represented company standards or that public comments made by the company about the code misleadingly publicized the quality of ethical controls. In some circumstances, courts found that statements about or within such codes were more than merely aspirational and did not constitute inactionable puffery, including when viewed in context rather than in isolation. In late March 2020, for example, a company settled a securities class action for $240 million alleging that statements in its code of conduct and code of ethics were false or misleading. The facts of this case were unusual, but it is likely that securities plaintiffs will seek to leverage rulings from the court in that class action to pursue other cases involving code of conducts or ethics. It remains to be seen whether any of these code of conduct case holdings may in the future be extended to apply to cases alleging 10b-5 violations for statements made in a company’s ESG reports.

B. State Consumer Protection Laws

Claims under U.S. state consumer protection laws have been of limited success. Nevertheless, many cases have been appealed which has resulted in additional litigation costs in circumstances where these costs were already significant even when not appealed. Recent claims that were appealed, even if ultimately failed, and which survived the motion to dismiss stage, include claims brought under California’s consumer protection laws alleging that human right commitments on a company website imposed on such company a duty to disclose on its labels that it or its supply chain could be employing child and/or forced labor. Cases have also been dismissed for lack of causal connection between alleged violation and economic injury including a claim under California, Florida and Texas consumer protection statutes alleging that the operator of several theme parks failed to disclose material facts about its treatment of orcas. The case was appealed to the U.S. Court of Appeals for the Ninth Circuit, but was dismissed for failure to show a causal connection between the alleged violation and the plaintiffs’ economic injury.

Overall, successful litigation relating to ESG disclosures is still very much a rare occurrence. However, this does not mean that companies are therefore insulated from litigation risk. Although perhaps not ultimately successful, merely having a claim initiated against a company can have serious reputational damage and may cause a company to incur significant litigation and public relations costs. The next section outlines three key takeaways and related best practices aimed to reduce such risks.

C. Practical Recommendations

Although the above makes clear that ESG litigation to date is often unsuccessful, companies should still be wary of the significant impacts of such litigation. The following outlines some key takeaways and best practices for companies seeking to continue ESG disclosure while simultaneously limiting litigation risk.

Key Takeaway 1: Disclaimers are Critical

As more and more companies publish reports on ESG performance, like disclaimers on forward-looking statements in SEC filings, companies are beginning to include disclaimers in their ESG reports, which disclaimers may or may not provide protection against potential litigation risks. In many cases, the language found in ESG reports will mirror language in SEC filings, though some companies have begun to tailor them specifically to the content of their ESG reports.

From our limited survey of companies across four industries that receive significant pressure to publish such reports—Banking, Chemicals, Oil & Gas and Utilities & Power—the following preliminary conclusions were drawn:

All companies surveyed across all sectors have some type of “forward-looking statement” disclaimer in their SEC filings; however, these were generic disclaimers that were not tailored to ESG-specific facts and topics or relating to items discussed in their ESG reports.

Most companies had some sort of disclaimer in their Sustainability Report, although some were lacking one altogether. Very few companies had disclaimers that were tailored to the specific facts and topics discussed in their ESG reports:

In the Oil & Gas industry, one company surveyed had a tailored ESG disclaimer in its ESG Report; all others had either the same disclaimer as in SEC filings or a shortened version that was generally very broad.

In the Banking industry, two companies lacked disclaimers altogether, but the rest had either their SEC disclaimer or a shortened version.

In the Utilities & Power industry, one company had no disclaimer, but the rest had general disclaimers.

In the Chemicals industry, three companies had no disclaimer in their reports, but the rest had shortened general disclaimers.

There seems to be a disconnect between the disclaimers being used in SEC filings and those found in ESG In particular, ESG disclaimers are generally shorter and will often reference more detailed disclaimers found in SEC filings.

Best Practices: When drafting ESG disclaimers, companies should:

Draft ESG disclaimers carefully. ESG disclaimers should be drafted in a way that explicitly covers ESG data so as to reduce the risk of litigation.

State that ESG data is non-GAAP. ESG data is usually non-GAAP and non-audited; this should be made clear in any ESG Disclaimer.

Have consistent disclaimers. Although disclaimers in SEC filings appear to be more detailed, disclaimers across all company documents that reference ESG data should specifically address these issues. As more companies start incorporating ESG into their proxies and other SEC filings, it is important that all language follows through.

Key Takeaway 2: ESG Reporting Can Pose Risks to a Company

This article highlighted the clear risks associated with inattentive ESG disclosure: potential litigation; bad publicity; and significant costs, among other things.

Best Practices: Companies should ensure statements in ESG reports are supported by fact or data and should limit overly aspirational statements. Representations made in ESG Reports may become actionable, so companies should disclose only what is accurate and relevant to the company.

Striking the right balance may be difficult; many companies will under-disclose, while others may over-disclose. Companies should therefore only disclose what is accurate and relevant to the company. The US Chamber of Commerce, in their ESG Reporting Best Practices, suggests things in a similar vein: do not include ESG metrics into SEC filings; only disclose what is useful to the intended audience and ensure that ESG reports are subject to a “rigorous internal review process to ensure accuracy and completeness.”

Key Takeaway 3: ESG Reporting Can Also be Beneficial for Companies

The threat of potential litigation should not dissuade companies from disclosing sustainability frameworks and metrics. Not only are companies facing investor pressure to disclose ESG metrics, but such disclosure may also incentivize companies to improve internal risk management policies, internal and external decisional-making capabilities and may increase legal and protection when there is a duty to disclose. Moreover, as ESG investing becomes increasingly popular, it is important for companies to be aware that robust ESG reporting, which in turn may lead to stronger ESG ratings, can be useful in attracting potential investors.

Best Practices: Companies should try to understand key ESG rating and reporting methodologies and how they match their company profile.

The growing interest in ESG metrics has meant that the number of ESG raters has grown exponentially, making it difficult for many companies to understand how each “rater” calculates a company’s ESG score. Resources such as the Better Alignment Project run by the Corporate Reporting Dialogue, strive to better align corporate reporting requirements and can give companies an idea of how frameworks such as CDP, CDSB, GRI and SASB overlap. By understanding the current ESG market raters and methodologies, companies will be able to better align their ESG disclosures with them. The U.S. Chamber of Commerce report noted above also suggests that companies should “engage with their peers and investors to shape ESG disclosure frameworks and standards that are fit for their purpose.”