finance sociale et investissement responsable Gouvernance Nouvelles diverses

Facteurs ESG ou facteurs GSE

Ivan Tchotourian 1 août 2024

Bel article à parcourir sur les priorités des critères ESG… peut-être à inverser (!) : Gouvernance, Social, puis Environnement.

Extrait :

La durabilité, un enjeu de… durabilité et de performance pour les entreprises

La bonne nouvelle est que de plus en plus de dirigeants se rendent compte que la prise en compte des enjeux sociaux et environnementaux devient indispensable afin d’assurer la durabilité de leurs modèles d’affaires et, par là même, la pérennité de leurs entreprises.

De plus en plus d’études témoignent par ailleurs que la prise en compte des enjeux ESG a un impact positif sur les indicateurs financiers de l’entreprise. L’étude d’Eiffel Sustainability & Impact Innovation Center de Mai 2024 sur des PME & Eti européennes, démontre que 83% des objectifs ESG ont eu une répercussion nette positive sur les indicateurs financiers des entreprises étudiées. En prenant conscience que ces enjeux représentent désormais des risques avérés, mais sont aussi des opportunités de création de valeur globale pour leurs entreprises, les dirigeants comprennent qu’ils doivent mieux prendre en considération les impacts positifs ou négatifs que leurs activités génèrent. Ainsi, ils sont de plus en plus nombreux à positionner ces sujets là où ils doivent l’être : au cœur de leur stratégie pour adapter les modèles d’affaires et les propositions de valeur.

Il y a urgence, car il y va de la pérennité même des entreprises à moyen terme. En effet, bien au-delà d’un objectif de réduction de l’empreinte environnementale de leurs activités, les exigences des parties prenantes vis-à-vis de l’entreprise se sont considérablement renforcées en très peu de temps. Cela implique que les entreprises prennent des engagements qui vont très au-delà de la mise en place d’une feuille de route RSE classique. Depuis le Covid, les salariés, au-delà d’un revenu décent et de la perspective d’évolution de carrière alléchante, attendent désormais de leur employeur du sens et un engagement sincère sur les sujets sociaux et environnementaux, pouvant aller jusqu’à quitter leur entreprise ou à refuser un poste ; les donneurs d’ordre accordent une importance croissante voire centrale aux critères ESG dans la sélection de leurs fournisseurs ; le monde de la finance est de plus en plus actif, avec, d’un côté, les fonds d’investissement qui font de l’ESG un critère de sélection et de valorisation objective de leurs participations et, de l’autre, les banques, qui proposent des prêts à taux bonifiés indexés sur l’amélioration d’indicateurs de performance extra-financiers.

On le voit bien, le risque pour une entreprise à ne pas s’engager est réel et dépasse très largement le cadre de la conformité réglementaire. Car si elle ne peut plus attirer ou retenir les talents, si elle vend de plus en plus difficilement et si elle a de plus en plus de mal à se financer, elle est inexorablement amenée à disparaître à plus ou moins brève échéance…

Un enjeu global, systémique et existentiel

La durabilité devient ainsi le nouveau grand sujet de transformation de l’entreprise car une condition essentielle à sa pérennité. Il est global car il les concerne toutes, systémique car il touche à toutes ses fonctions, et essentiel car il interroge sur sa finalité même. Il est plus profond que le digital qui reste, malgré les considérables changements qu’il a occasionnés, un moyen, alors qu’il a bouleversé de façon brutale le paysage concurrentiel de la plupart des secteurs d’activité.

(…)

Si on attend d’elle qu’elle ait un impact sur la société et sur son environnement, elle doit évidemment avoir la capacité d’investir et de se projeter sur le long terme et donc avoir un modèle économique qui fonctionne. Mais la nécessaire transformation d’une entreprise pour la rendre résiliente face aux nouveaux enjeux de durabilité impose de dépasser l’urgence du court terme pour mener une réflexion et s’engager sur un temps long, qui va au-delà de son horizon classique de réflexion.

Pour une démarche GSE : Gouvernance, Social, Environnement

La prise de conscience et la construction de convictions fortes du dirigeant et l’alignement avec les instances de gouvernance constituent la première condition pour que l’entreprise se mette en mouvement. Un dirigeant climato sceptique ou qui ne voit dans l’ESG qu’un ensemble de contraintes ne pourra pas créer la dynamique nécessaire pour lancer un chantier de transformation qui affecte toutes les dimensions de l’entreprise. À l’opposé, un dirigeant convaincu mais entouré d’actionnaires qui exigent des résultats à court terme aura du mal à imposer à ses associés des arbitrages visant à renoncer à une performance immédiate au profit d’un investissement dont les retours ne seront visibles qu’au-delà de leur horizon naturel de réflexion. Une entreprise sous LBO, dont les fonds majoritaires exigent un TRI très élevé avec une sortie prévue à deux ou trois ans ou encore une entreprise cotée avec des fonds activistes à son capital n’auront pas la même capacité de projection qu’une entreprise dont le capital est détenu depuis plusieurs générations par une famille et qui s’inscrit dans une tradition de transmission patrimoniale. En considérant la durabilité comme un sujet désormais essentiel, dont les effets se mesurent sur le temps long, la gouvernance va devoir adapter son système de mesure et de reconnaissance de la performance pour y intégrer des critères extra-financiers. La CSRD par le cadre qu’elle pose, invite progressivement les 50 000 plus grandes entreprises européennes à mener cette réflexion dès 2024 et à publier des engagements concrets qui se généraliseront par la suite à l’ensemble de leur chaîne de valeur.

La conviction du dirigeant, l’alignement avec les représentants des actionnaires et le board, de nouveaux indicateurs de performances sont des préalables indispensables pour créer l’impulsion nécessaire. L’étape suivante consiste à embarquer les véritables acteurs de la transformation : les équipes. Là encore, il s’agit de faire les choses dans le bon ordre : des dirigeants qui ont toujours appliqué un modèle de management classique basé sur la recherche de croissance et de profit risquent de susciter scepticisme, voire désengagement s’ils affichent une volonté soudaine de contribuer au bien commun, même s’ils sont sincères.

Le procès en green ou en purpose washing n’est jamais loin. Il faut donc expliquer, donner de la perspective et de la profondeur au sujet pour embarquer les équipes, indispensables pour opérer une transformation qui touche à l’ensemble des métiers et nécessitera donc l’implication de tous. Le besoin de comprendre des équipes est réel, ne serait-ce que pour démontrer qu’il ne s’agit pas d’un effet de mode mais la conséquence d’une évolution en profondeur du modèle capitaliste dont l’entreprise doit se saisir sans tarder.

Mais cela ne suffit évidemment pas. On ne change pas cinquante ans de culture friedmanienne dans les entreprises par la magie de quelques heures de sensibilisation aux grandes évolutions du monde capitaliste. L’ESG est souvent déstabilisant pour des équipes qui se retrouvent face à des injonctions contradictoires et qui vont devoir renoncer à prendre des décisions qui paraissaient évidentes jusque-là.

Accepter des coûts supérieurs pour acheter local, renoncer à un investissement très rentable à court terme car il générera des nuisances sur le long terme, incompatibles avec le nouveau projet de l’entreprise, modifier la structure de rémunération des équipes commerciales jusque-là basée sur des critères de performance au mois pour le remplacer par un indice de satisfaction clients sur le long terme est déstabilisant. Le dirigeant devra être entouré d’une équipe de comité de direction convaincue qui, à son tour, pourra embarquer le management intermédiaire et l’ensemble des équipes.

Intégrer la durabilité devient une nécessité vitale pour l’entreprise et requiert conviction du dirigeant et alignement de la gouvernance avant la mise en œuvre d’un volet social incontournable pour accompagner la transformation et le changement. C’est à cette condition qu’on pourra embarquer les équipes et les motiver à imaginer et lancer les offres qui permettront d’avoir un impact positif et réellement décisif sur l’environnement. C’est précisément la philosophie à laquelle nous invite le reporting de durabilité CSRD qui permet aux entreprises d’encadrer leur démarche.

Il faut donc bouleverser l’ordre des choses : l’impact environnemental est une conséquence et non pas la finalité d’un programme ESG.

D’ailleurs, ne devrions-nous pas désormais parler de programme GSE ?

À la prochaine…

Gouvernance Nouvelles diverses

Research Handbook on Environmental, Social and Corporate Governance

Ivan Tchotourian 21 juin 2024

Voilà une nouvelle publication à signaler !

La table des matières donne envie :

Introduction to Research Handbook on Environmental, Social and Corporate Governance 1

Thilo Kuntz

PART I DIRECTORS’ DUTIES AND MANAGERIAL DECISION-MAKING

1 Taking stakeholder interests seriously: A practitioner’s view from Germany on management duties 21

Christoph H. Seibt

2 ESG enhancements to company law: The French ‘PACTE’ law 44

Alain Pietrancosta

3 How ESG is weakening the business judgement rule 64

Thilo Kuntz

4 Human rights, environmental due diligence, and value chain responsibility: A view from France, Germany, and the European Union 91

Katrin Deckert

PART II INVESTOR AND SHAREHOLDER ACTIVISM

5 Stewardship codes, ESG activism and transnational ordering 112

Tim Bowley and Jennifer G. Hill

6 Climate proposals: ESG shareholder activism sidestepping board authority 132

Sofie Cools

7 ESG and workforce engagement: Experiences in the UK 151

Andrew Johnston and Navajyoti Samanta

8 ESG, the Alien Tort Statute, and private regulation’s legitimacy trap 171

Seth Davis

PART III INVESTMENT AND FUND REGULATION

9 EU ‘rule-based’ ESG duties for investment funds and their managers under the European ‘Green Deal’ 194

Sebastiaan Niels Hooghiemstra

10 Green bonds: A legal and economic analysis 217

Sergio Gilotta

11 Green public finance: The role of central banks 239

Jörn Axel Kämmerer

PART IV DISCLOSURE REGULATION AND RATINGS

12 The forces that shape mandatory ESG reporting 258

Thorsten Sellhorn and Victor Wagner

13 A green victory in the midst of potential defeat? Concern and optimism about the impact of the SEC’s climate-related disclosure rule 281

Lisa M. Fairfax

14 ESG ratings—guiding a movement in search for itself 303

Andreas Engert

PART V INTERNATIONAL LAW

15 ESG initiatives in international law 325

Rita Guerreiro Teixeira and Jan Wouters

16 ESG and international criminal liability 344

Cedric Ryngaert and Martine Jaarsma

PART VI REGIONAL DEVELOPMENTS

17 The EU Framework on ESG 362

Erik Lidman

18 The Nordic approach to corporate governance and ESG 381

Jesper Lau Hansen

19 ESG in China: A critical review from a legal perspective 404

Xianchu Zhang

20 ESG in Japan: The case of a mixed legal system 421

Masayuki Tamaruya and Mutsuhiko Yukioka

21 The legal and regulatory impetus towards ESG in India: Developments and challenges 443

Umakanth Varottil

actualités canadiennes Divulgation divulgation extra-financière Gouvernance Normes d'encadrement

Divulgation ESG : les entreprises canadiennes font mieux

Ivan Tchotourian 14 septembre 2022 Ivan Tchotourian

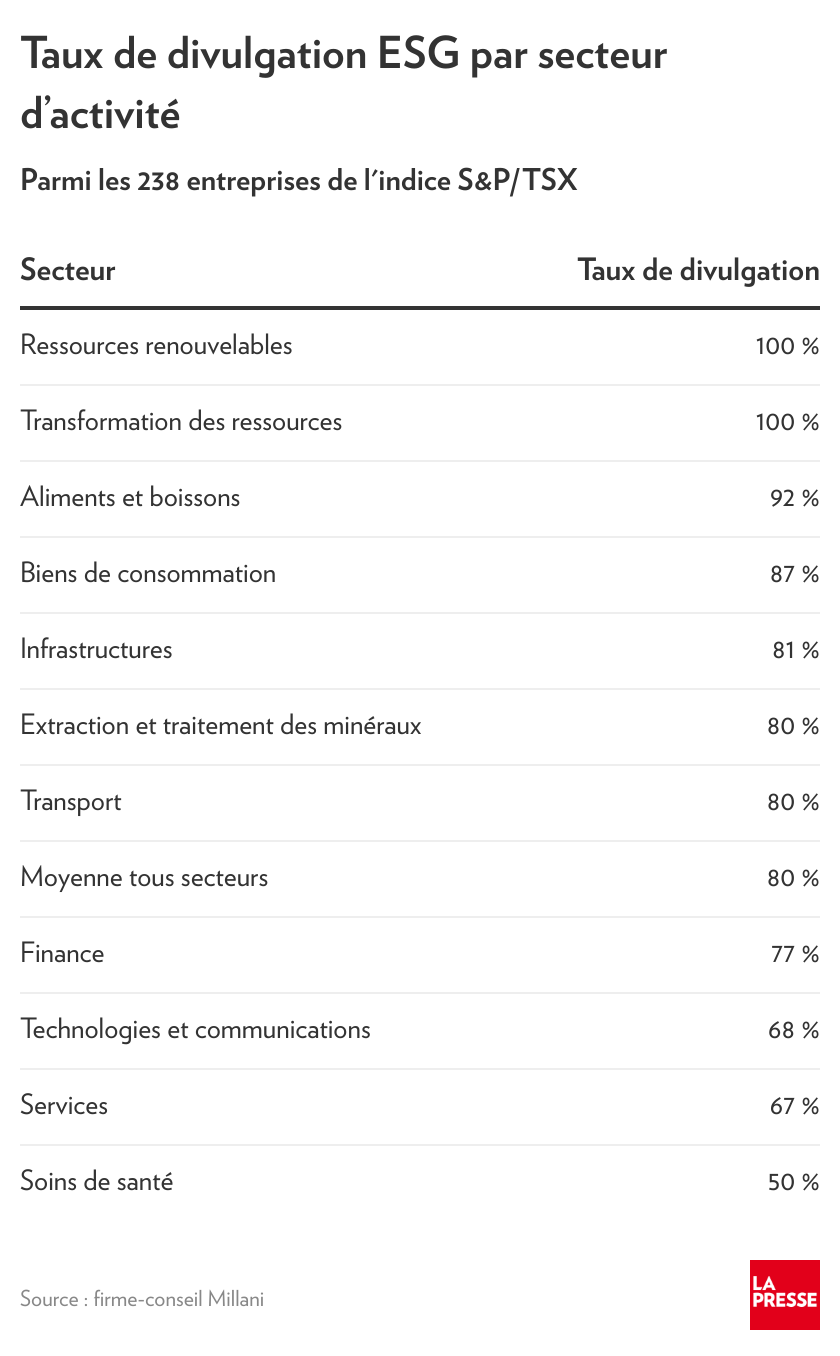

Dans La presse.ca, le journaliste Martin Vallières diffuse les enseignements du dernier rapport Milani montrant que les grandes entreprises canadiennes améliorent leur diffusion des critères ESG. Bonne nouvelle pour la RSE !

Extrait :

« Notre recherche révèle que 80 % des entreprises de l’indice S&P/TSX publient maintenant un rapport ESG, ce qui est mieux que le taux de 71 % mesuré un an plus tôt, mais encore inférieur au 92 % parmi les entreprises de l’indice S&P 500 », lit-on dans le rapport de la firme Millani.

En parallèle, constate Millani, « bien que les rapports ESG soient de plus en plus nombreux, les investisseurs cherchent désormais plus qu’un rapport ».

« Les investisseurs expriment leur désir de comprendre plus profondément les impacts de ces sujets ESG : comment sont-ils gérés, quels sont les indicateurs de performance qui sont suivis et comment évoluent-ils ? Quelle est la capacité d’une entreprise à s’adapter aux risques et à atténuer les impacts négatifs futurs ? »

De plus, signale le rapport de Millani, « les entreprises qui se démarquent dans la valeur stratégique des enjeux en ESG incorporent des mesures de performance en ce sens dans la rémunération du conseil d’administration et de la direction ».

À la prochaine…

actualités canadiennes Divulgation divulgation extra-financière Normes d'encadrement Responsabilité sociale des entreprises

CFA Institute : document de consultation

Ivan Tchotourian 26 octobre 2020 Ivan Tchotourian

CFA Institute a proposé des standards en matière de divulgation des critères ESG dans les produits financiers : « Consulter Paper on the Development of the CFA Institute – ESG Disclosure Standards For Investments Products » (août 2020).

- Pour un article de presse : ici

Petit extrait :

- Disclosure Requirements Many of the Standard’s requirements will be related to disclosures. Disclosure requirements are a key way to provide transparency and comparability for investors. A disclosure requirement is simply a means of ensuring that asset managers communicate certain information to investors. There are different ways that disclosures might be required, both in terms of scope and method. Therefore, it is necessary to establish principles to ensure the disclosure requirements meet the purpose of the Standard. We propose the following design principles:

- Disclosure requirements should focus on relevant, useful information. Disclosures must provide information that will help investors better understand investment products, make comparisons, and choose among alternatives. • Disclosure requirements should focus primarily on ESG-related features. Because the goal of the Standard is to enable greater transparency and comparability of investment products with ESG-related features, the Standard’s disclosure requirements should focus on these features. Focusing the disclosure requirements on ESG-related features also avoids adding unnecessarily to an asset manager’s disclosure burden.

- Disclosure requirements should allow asset managers the flexibility to make the required disclosure in the clearest possible manner given the nature of the product. Disclosure requirements can easily be reformulated as questions. There are two types of questions—open-ended and closed-ended. Open-ended questions ask who, what, why, where, when, or how. Closed-ended questions require answers in a specific form—either yes/no or selected from a predefined list. The open-ended disclosure requirement format provides the flexibility needed for the Standard to be relevant on a global scale and to pertain to all types of investment products with ESG-related features. The open-ended nature of the disclosure requirements, however, must be balanced to a certain degree with a standardization of responses for the sake of comparison by investors. The forthcoming Exposure Draft will include examples of openended and standardized disclosures.

- The disclosure requirements should aim to elicit a moderate level of detail. An investment product’s disclosures should accurately and adequately represent the policies and procedures that govern the design and implementation of the investment product. The Standard’s disclosure requirements can be thought of as a step between a database search and a due diligence conversation. The disclosures will provide more detail than can be standardized and presented in a database but less detail than the information one can obtain through a full due diligence process.

- The disclosure requirements should prioritize content over format. The disclosure requirements will focus on what information is disclosed rather than how it is disclosed. The Standard will provide a certain degree of flexibility in the format for information presentation. Providing latitude in the format is intended to reduce an asset manager’s disclosure burden and allow for harmonization with disclosures required by regulatory bodies and other standards. The Exposure Draft will offer examples of presentation formats. • Disclosure requirements should be categorized as “general” or “feature-specific”. The Standard will have both general and feature-specific disclosure requirements. General disclosure requirements will apply to all investment products that seek to comply with the Standard. Feature-specific disclosure requirements will apply only to investment products that have a specific ESG-related feature.

- The Standard should include disclosure recommendations in addition to requirements. We anticipate that in addition to the Standard’s required disclosures, the Standard will have recommended disclosures as well. Required disclosures represent the minimum information that must be disclosed in order to comply with the Standard. Recommended disclosures provide additional information that investors may find helpful in their decision making. Recommended disclosures are encouraged but not mandatory.

À la prochaine…

Gouvernance Nouvelles diverses parties prenantes Responsabilité sociale des entreprises

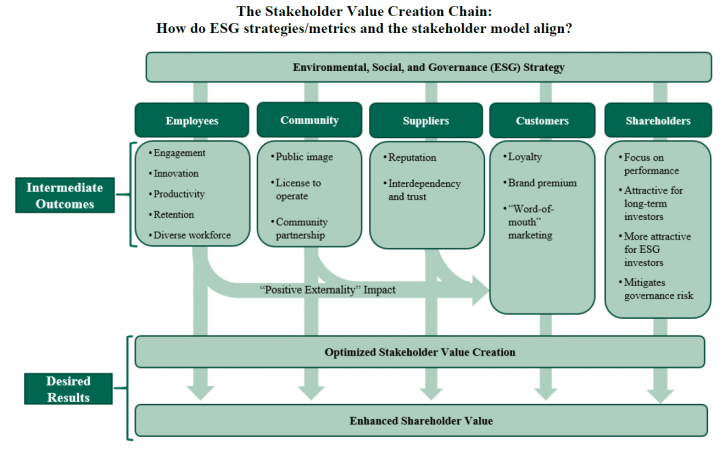

The Stakeholder Model and ESG

Ivan Tchotourian 17 septembre 2020 Ivan Tchotourian

Intéressant article sur l’Harvard Law School Forum on Corporate Governance consacré au modèle partie prenante et à ses liens avec les critères ESG : « The Stakeholder Model and ESG » (Ira Kay, Chris Brindisi et Blaine Martin, 14 septembre 2020).

Extrait :

Is your company ready to set or disclose ESG incentive goals?

ESG incentive metrics are like any other incentive metric: they should support and reinforce strategy rather than lead it. Companies considering ESG incentive metrics should align planning with the company’s social responsibility and environmental strategies, reporting, and goals. Another essential factor in determining readiness is the measurability/quantification of the specific ESG issue.

Companies will generally fall along a spectrum of readiness to consider adopting and disclosing ESG incentive metrics and goals:

- Companies Ready to Set Quantitative ESG Goals: Companies with robust environmental, sustainability, and/or social responsibility strategies including quantifiable metrics and goals (e.g., carbon reduction goals, net zero carbon emissions commitments, Diversity and Inclusion metrics, employee and environmental safety metrics, customer satisfaction, etc.).

- Companies Ready to Set Qualitative Goals: Companies with evolving formalized tracking and reporting but for which ESG matters have been identified as important factors to customers, employees, or other These companies likely already have plans or goals around ESG factors (e.g., LEED [Leadership in Energy and Environmental Design]-certified office space, Diversity and Inclusion initiatives, renewable power and emissions goals, etc.).

- Companies Developing an ESG Strategy: Some companies are at an early stage of developing overall ESG/stakeholder strategies. These companies may be best served to focus on developing a strategy for environmental and social impact before considering linking incentive pay to these priorities.

We note it is critically important that these ESG/stakeholder metrics and goals be chosen and set with rigor in the same manner as financial metrics to ensure that the attainment of the ESG goals will enhance stakeholder value and not serve simply as “window dressing” or “greenwashing.” [9] Implementing ESG metrics is a company-specific design process. For example, some companies may choose to implement qualitative ESG incentive goals even if they have rigorous ESG factor data and reporting.

Will ESG metrics and goals contribute to the company’s value-creation?

The business case for using ESG incentive metrics is to provide line-of-sight for the management team to drive the implementation of initiatives that create significant differentiated value for the company or align with current or emerging stakeholder expectations. Companies must first assess which metrics or initiatives will most benefit the company’s business and for which stakeholders. They must also develop challenging goals for these metrics to increase the likelihood of overall value creation. For example:

- Employees: Are employees and the competitive talent market driving the need for differentiated environmental or social initiatives? Will initiatives related to overall company sustainability (building sustainability, renewable energy use, net zero carbon emissions) contribute to the company being a “best in class” employer? Diversity and inclusion and pay equity initiatives have company and social benefits, such as ensuring fair and equitable opportunities to participate and thrive in the corporate system.

- Customers: Are customer preferences driving the need to differentiate on sustainable supply chains, social justice initiatives, and/or the product/company’s environmental footprint?

- Long-Term Sustainability: Are long-term macro environmental factors (carbon emissions, carbon intensity of product, etc.) critical to the Company’s ability to operate in the long term?

- Brand Image: Does a company want to be viewed by all constituencies, including those with no direct economic linkage, as a positive social and economic contributor to society?

There is no one-size-fits-all approach to ESG metrics, and companies fall across a spectrum of needs and drivers that affect the type of ESG factors that are relevant to short- and long-term business value depending on scale, industry, and stakeholder drivers. Most companies have addressed, or will need to address, how to implement ESG/stakeholder considerations in their operating strategy.

Conceptual Design Parameters for Structuring Incentive Goals

For those companies moving to implement stakeholder/ESG incentive goals for the first time, the design parameters range widely, which is not different than the design process for implementing any incentive metric. For these companies, considering the following questions can help move the prospect of an ESG incentive metric from an idea to a tangible goal with the potential to create value for the company:

- Quantitative goals versus qualitative milestones. The availability and quality of data from sustainability or social responsibility reports will generally determine whether a company can set a defined quantitative goal. For other companies, lack of available ESG data/goals or the company’s specific pay philosophy may mean ESG initiatives are best measured by setting annual milestones tailored to selected goals.

- Selecting metrics aligned with value creation. Unlike financial metrics, for which robust statistical analyses can help guide the metric selection process (e.g., financial correlation analysis), the link between ESG metrics and company value creation is more nuanced and significantly impacted by industry, operating model, customer and employee perceptions and preferences, etc. Given this, companies should generally apply a principles-based approach to assess the most appropriate metrics for the company as a whole (e.g., assessing significance to the organization, measurability, achievability, etc.) Appendix 1 provides a list of common ESG metrics with illustrative mapping to typical stakeholder impact.

- Determining employee participation. Generally, stakeholder/ESG-focused metrics would be implemented for officer/executive level roles, as this is the employee group that sets company-wide policy impacting the achievement of quantitative ESG goals or qualitative milestones. Alternatively, some companies may choose to implement firm-wide ESG incentive metrics to reinforce the positive employee engagement benefits of the company’s ESG strategy or to drive a whole-team approach to achieving goals.

- Determining the range of metric weightings for stakeholder/ESG goals. Historically, US companies with existing environmental, employee safety, and customer service goals as well as other stakeholder metrics have been concentrated in the extractive, industrial, and utility industries; metric weightings on these goals have ranged from 5% to 20% of annual incentive scorecards. We expect that this weighting range would continue to apply, with the remaining 80%+ of annual incentive weighting focused on financial metrics. Further, we expect that proxy advisors and shareholders may react adversely to non-financial metrics weighted more than 10% to 20% of annual incentive scorecards.

- Considering whether to implement stakeholder/ESG goals in annual versus long-term incentive plans. As noted above, most ESG incentive goals to date have been implemented as weighted metrics in balanced scorecard annual incentive plans for several reasons. However, we have observed increased discussion of whether some goals (particularly greenhouse gas emission goals) may be better suited to long-term incentives. [10] There is no right answer to this question—some milestone and quantitative goals are best set on an annual basis given emerging industry, technology, and company developments; other companies may have a robust long-term plan for which longer-term incentives are a better fit.

- Considering how to operationalize ESG metrics into long-term plans. For companies determining that sustainability or social responsibility goals fit best into the framework of a long-term incentive, those companies will need to consider which vehicles are best to incentivize achievement of strategically important ESG goals. While companies may choose to dedicate a portion of a 3-year performance share unit plan to an ESG metric (e.g., weighting a plan 40% relative total shareholder return [TSR], 40% revenue growth, and 20% greenhouse gas reduction), there may be concerns for shareholders and/or participants in diluting the financial and shareholder-value focus of these incentives. As an alternative, companies could grant performance restricted stock units, vesting at the end of a period of time (e.g., 3 or 4 years) contingent upon achievement of a long-term, rigorous ESG performance milestone. This approach would not “dilute” the percentage of relative TSR and financial-based long-term incentives, which will remain important to shareholders and proxy advisors.

Conclusion

As priorities of stakeholders continue to evolve, and addressing these becomes a strategic imperative, companies may look to include some stakeholder metrics in their compensation programs to emphasize these priorities. As companies and Compensation Committees discuss stakeholder and ESG-focused incentive metrics, each organization must consider its unique industry environment, business model, and cultural context. We interpret the BRT’s updated statement of business purpose as a more nuanced perspective on how to create value for all stakeholders, inclusive of shareholders. While optimizing profits will remain the business purpose of corporations, the BRT’s statement provides support for prioritizing the needs of all stakeholders in driving long-term, sustainable success for the business. For some companies, implementing incentive metrics aligned with this broader context can be an important tool to drive these efforts in both the short and long term. That said, appropriate timing, design, and communication will be critical to ensure effective implementation.

À la prochaine…

actualités internationales Divulgation divulgation extra-financière Gouvernance Normes d'encadrement normes de droit normes de marché Responsabilité sociale des entreprises

Approche juridique sur la transparence ESG

Ivan Tchotourian 3 août 2020 Ivan Tchotourian

Excellente lecture ce matin de ce billet du Harvard Law School Forum on Corporate Governance : « Legal Liability for ESG Disclosures » (de Connor Kuratek, Joseph A. Hall et Betty M. Huber, 3 août 2020). Dans cette publication, vous trouverez non seulement une belle synthèse des référentiels actuels, mais aussi une réflexion sur les conséquences attachées à la mauvaise divulgation d »information.

Extrait :

3. Legal Liability Considerations

Notwithstanding the SEC’s position that it will not—at this time—mandate additional climate or ESG disclosure, companies must still be mindful of the potential legal risks and litigation costs that may be associated with making these disclosures voluntarily. Although the federal securities laws generally do not require the disclosure of ESG data except in limited instances, potential liability may arise from making ESG-related disclosures that are materially misleading or false. In addition, the anti-fraud provisions of the federal securities laws apply not only to SEC filings, but also extend to less formal communications such as citizenship reports, press releases and websites. Lastly, in addition to potential liability stemming from federal securities laws, potential liability could arise from other statutes and regulations, such as federal and state consumer protection laws.

A. Federal Securities Laws

When they arise, claims relating to a company’s ESG disclosure are generally brought under Section 11 of the Securities Act of 1933, which covers material misstatements and omissions in securities offering documents, and under Section 10(b) of the Securities Exchange Act of 1934 and rule 10b-5, the principal anti-fraud provisions. To date, claims brought under these two provisions have been largely unsuccessful. Cases that have survived the motion to dismiss include statements relating to cybersecurity (which many commentators view as falling under the “S” or “G” of ESG), an oil company’s safety measures, mine safety and internal financial integrity controls found in the company’s sustainability report, website, SEC filings and/or investor presentations.

Interestingly, courts have also found in favor of plaintiffs alleging rule 10b-5 violations for statements made in a company’s code of conduct. Complaints, many of which have been brought in the United States District Court for the Southern District of New York, have included allegations that a company’s code of conduct falsely represented company standards or that public comments made by the company about the code misleadingly publicized the quality of ethical controls. In some circumstances, courts found that statements about or within such codes were more than merely aspirational and did not constitute inactionable puffery, including when viewed in context rather than in isolation. In late March 2020, for example, a company settled a securities class action for $240 million alleging that statements in its code of conduct and code of ethics were false or misleading. The facts of this case were unusual, but it is likely that securities plaintiffs will seek to leverage rulings from the court in that class action to pursue other cases involving code of conducts or ethics. It remains to be seen whether any of these code of conduct case holdings may in the future be extended to apply to cases alleging 10b-5 violations for statements made in a company’s ESG reports.

B. State Consumer Protection Laws

Claims under U.S. state consumer protection laws have been of limited success. Nevertheless, many cases have been appealed which has resulted in additional litigation costs in circumstances where these costs were already significant even when not appealed. Recent claims that were appealed, even if ultimately failed, and which survived the motion to dismiss stage, include claims brought under California’s consumer protection laws alleging that human right commitments on a company website imposed on such company a duty to disclose on its labels that it or its supply chain could be employing child and/or forced labor. Cases have also been dismissed for lack of causal connection between alleged violation and economic injury including a claim under California, Florida and Texas consumer protection statutes alleging that the operator of several theme parks failed to disclose material facts about its treatment of orcas. The case was appealed to the U.S. Court of Appeals for the Ninth Circuit, but was dismissed for failure to show a causal connection between the alleged violation and the plaintiffs’ economic injury.

Overall, successful litigation relating to ESG disclosures is still very much a rare occurrence. However, this does not mean that companies are therefore insulated from litigation risk. Although perhaps not ultimately successful, merely having a claim initiated against a company can have serious reputational damage and may cause a company to incur significant litigation and public relations costs. The next section outlines three key takeaways and related best practices aimed to reduce such risks.

C. Practical Recommendations

Although the above makes clear that ESG litigation to date is often unsuccessful, companies should still be wary of the significant impacts of such litigation. The following outlines some key takeaways and best practices for companies seeking to continue ESG disclosure while simultaneously limiting litigation risk.

Key Takeaway 1: Disclaimers are Critical

As more and more companies publish reports on ESG performance, like disclaimers on forward-looking statements in SEC filings, companies are beginning to include disclaimers in their ESG reports, which disclaimers may or may not provide protection against potential litigation risks. In many cases, the language found in ESG reports will mirror language in SEC filings, though some companies have begun to tailor them specifically to the content of their ESG reports.

From our limited survey of companies across four industries that receive significant pressure to publish such reports—Banking, Chemicals, Oil & Gas and Utilities & Power—the following preliminary conclusions were drawn:

- All companies surveyed across all sectors have some type of “forward-looking statement” disclaimer in their SEC filings; however, these were generic disclaimers that were not tailored to ESG-specific facts and topics or relating to items discussed in their ESG reports.

- Most companies had some sort of disclaimer in their Sustainability Report, although some were lacking one altogether. Very few companies had disclaimers that were tailored to the specific facts and topics discussed in their ESG reports:

- In the Oil & Gas industry, one company surveyed had a tailored ESG disclaimer in its ESG Report; all others had either the same disclaimer as in SEC filings or a shortened version that was generally very broad.

- In the Banking industry, two companies lacked disclaimers altogether, but the rest had either their SEC disclaimer or a shortened version.

- In the Utilities & Power industry, one company had no disclaimer, but the rest had general disclaimers.

- In the Chemicals industry, three companies had no disclaimer in their reports, but the rest had shortened general disclaimers.

- There seems to be a disconnect between the disclaimers being used in SEC filings and those found in ESG In particular, ESG disclaimers are generally shorter and will often reference more detailed disclaimers found in SEC filings.

Best Practices: When drafting ESG disclaimers, companies should:

- Draft ESG disclaimers carefully. ESG disclaimers should be drafted in a way that explicitly covers ESG data so as to reduce the risk of litigation.

- State that ESG data is non-GAAP. ESG data is usually non-GAAP and non-audited; this should be made clear in any ESG Disclaimer.

- Have consistent disclaimers. Although disclaimers in SEC filings appear to be more detailed, disclaimers across all company documents that reference ESG data should specifically address these issues. As more companies start incorporating ESG into their proxies and other SEC filings, it is important that all language follows through.

Key Takeaway 2: ESG Reporting Can Pose Risks to a Company

This article highlighted the clear risks associated with inattentive ESG disclosure: potential litigation; bad publicity; and significant costs, among other things.

Best Practices: Companies should ensure statements in ESG reports are supported by fact or data and should limit overly aspirational statements. Representations made in ESG Reports may become actionable, so companies should disclose only what is accurate and relevant to the company.

Striking the right balance may be difficult; many companies will under-disclose, while others may over-disclose. Companies should therefore only disclose what is accurate and relevant to the company. The US Chamber of Commerce, in their ESG Reporting Best Practices, suggests things in a similar vein: do not include ESG metrics into SEC filings; only disclose what is useful to the intended audience and ensure that ESG reports are subject to a “rigorous internal review process to ensure accuracy and completeness.”

Key Takeaway 3: ESG Reporting Can Also be Beneficial for Companies

The threat of potential litigation should not dissuade companies from disclosing sustainability frameworks and metrics. Not only are companies facing investor pressure to disclose ESG metrics, but such disclosure may also incentivize companies to improve internal risk management policies, internal and external decisional-making capabilities and may increase legal and protection when there is a duty to disclose. Moreover, as ESG investing becomes increasingly popular, it is important for companies to be aware that robust ESG reporting, which in turn may lead to stronger ESG ratings, can be useful in attracting potential investors.

Best Practices: Companies should try to understand key ESG rating and reporting methodologies and how they match their company profile.

The growing interest in ESG metrics has meant that the number of ESG raters has grown exponentially, making it difficult for many companies to understand how each “rater” calculates a company’s ESG score. Resources such as the Better Alignment Project run by the Corporate Reporting Dialogue, strive to better align corporate reporting requirements and can give companies an idea of how frameworks such as CDP, CDSB, GRI and SASB overlap. By understanding the current ESG market raters and methodologies, companies will be able to better align their ESG disclosures with them. The U.S. Chamber of Commerce report noted above also suggests that companies should “engage with their peers and investors to shape ESG disclosure frameworks and standards that are fit for their purpose.”

À la prochaine…