Selon un article de Les Échos.fr (« L’Allemagne s’attaque à l’éthique de ses entreprises à l’étranger », 15 juillet 2020), Berlin prépare pour la rentrée un projet de loi sur le respect des normes environnementales et sociales sur la chaîne d’approvisionnement des entreprises allemandes.

Extrait :

C’est un jeans bleu produit au Bangladesh, taille haute, banal, mais « il coûte 7 euros aux distributeurs allemands avec toutes les certifications nécessaires sur le respect des droits de l’homme par le producteur. Sans ces normes, il arrive sur le marché allemand à 5 euros : la différence est de 2 euros ». Un pantalon ou des sachets de thé à la main, le ministre allemand du Développement, Gerd Müller, s’est voulu très pédagogue en présentant mardi, à Berlin, les résultats d’une enquête sur le respect des normes sociales et environnementales internationales par les entreprises allemandes.

20 % des entreprises respectent les normes

Selon cette enquête, 98 multinationales allemandes, sur les 455 ayant répondu, respectent leurs engagements, et « c’est déjà une surprise », fait valoir Gerd Müller. « Clairement, l’Allemagne ne peut continuer à traiter la question du respect des normes sociales sur une base volontaire », en conclut Hubertus Heil, le ministre du Travail allemand.

Un cadre général devrait être présenté en août et un projet de loi sur les chaînes d’approvisionnement sera mis sur la table à la rentrée parlementaire, a-t-il annoncé. Son ambition : assurer une gestion des risques « proportionnée et raisonnable » par les entreprises et mettre en place des sanctions avec des amendes ou l’exclusion de marchés publiques à la clef. La loi anticiperait des initiatives européennes annoncées par Bruxelles pour 2021.

The quota requirement has been included as an amendment to the bill transposing the EU Shareholder Rights Directive II (SRD II) into Greek law, and is the result of a consultation led by a group of academics specialising in corporate governance.

(…)

Overall, the directive is designed to encourage companies away from short-termism, focusing on areas such as director remuneration. However, the Greek amendment marks the first time it has been used to tackle the EU’s poor record on gender diversity at a board level.

Within this, France was the only EU member state with at least 40% female representation at board-level, while women account for less than a third of board-level positions in Italy, Sweden, Finland and Germany.

According to the same data, women made up less than 10% of board members in Greece.

David Larcker, Bradford Lynch, Brian Tayan et Daniel Taylor publient un texte qui revient sur la transparence des ghrandes entreprises américaines en matière de COVID-19 « The Spread of Covid-19 Disclosure » (29 juin 2020). Un document plein de statistiques et de tendances sur la transparence… vraiment intéressant sachant que l’enjeu de la question n’est pas à négliger.

Extrait :

The COVID-19 pandemic presents an interesting scenario whereby an unexpected shock to the economic system led to a rapid deterioration in the economic landscape, causing sharp changes in performance relative to expectations just a few months prior. For most companies, the pandemic has been detrimental. For a few, it brought unexpected demand. In many cases, supply chains have been strained, causing ripple effects that extend well beyond any one company.

How do companies respond to such a situation? What choices do they make, and how much transparency do they offer? How does disclosure vary in a setting where the potential impact is so widely uncertain? The COVID-19 pandemic provides a unique setting to examine disclosure choices in a situation of extreme uncertainty that extends across all companies in the public market. This devastating outlier event provides a rare glimpse into disclosure behavior by managers and boards.

Why This Matters

The COVID-19 pandemic provides a unique opportunity to examine disclosure practices of companies relative to peers in real time about a somewhat unprecedented shock that impacted practically every publicly listed company in the U.S. We see that decisions varied considerably about whether to make disclosure and, if so, what and how much to say about the pandemic’s impact on operations, finances, and future. What motivates some companies to be forthcoming about what they are experiencing, while others remain silent? Does this reflect different degrees of certitude about how the virus would impact their businesses, or differences in managements’ perception of their “obligations” to be transparent with the public? What does this say about a company’s view of its relation and duty to shareholders?

In one example, we saw a consumer beverage company make zero references to COVID-19 in its SEC filings and website, despite the virus plausibly having at least some impact on its business. In another example, we saw a company claim no material changes to its previously reported risk factors when managers almost certainly had relevant information about the virus and the likely impact on sales and operations. What discussion among the senior managers, board members, external auditor, and general counsel leads to a decision to make no disclosures? What should shareholders glean from this decision, particularly in light of peer disclosure?

The COVID-19 pandemic represents a so-called “black swan” event that inflicted severe and unexpected damage to wide swaths of the economy. What strategic insights will companies learn from this event? Can boards use these insights to prepare for other possible outlier events, such as climate events, terrorism, cyber-attacks, pandemics, and other emergencies? Should these insights be disclosed to shareholders?

“The future of business will be different,” surmised a director on a recent virtual board roundtable hosted by RSR Partners, “in ways we can’t anticipate in this moment. Our board is focused on assessing whether all our directors are truly ready for what’s coming.”

Over the past few months, RSR Partners hosted more than a dozen roundtables for sitting directors, providing a forum for the participants to share what their boards are learning as they navigate the current crisis and pivot into the “new normal.” While tackling topics as diverse as commercial strategy, operations, health and safety, and the future of business, one theme was pervasive throughout the discussions: leadership and stakeholders will be looking to the boardroom for guidance, and board members not only need to have the requisite experience and skills to confidently provide direction, but the leadership characteristics that will allow them to be effective.

Fundamentally, the global business disruption and current uncertainty has created a need for a higher level of involvement from board members. “This is a time to have board members who have experienced really tough issues, such as major ecessions, difficult mergers, major cost cutting, insolvency and bankruptcy, and top management departures, along with experience in reinventing companies, including supply chain, product engineering and simplification, digital transformation, offshore manufacturing and procurement, sale of subsidiaries, and comprehensive refinancing,” stated Edward A. Kangas, former Chairman and CEO of Deloitte Touche. “This is not a time for deep thinking. It’s time for people with real experience who know how to oversee and support management in a time of crisis and reinvention.” (Mr. Kangas currently serves on the following boards: Deutsche Bank USA Corp., Intelsat SA, VIVUS, Inc., and Hovnanian Enterprises, Inc.).

Characteristics of Directors Who Succeed in the “New Normal”

From a practical perspective, there is now a higher premium placed on a director’s proven ability to navigate a business through a crisis while mitigating risk and understanding how and when to pull the levers that will impact balance sheets. The demand to optimize results, sustain business, and adapt to changes in a regional and global market has increased alongside the time commitment and attention to detail required of directors to address these issues. Normal requirements for sound governance, audit oversight, compensation strategies, business performance goals, and succession of key leadership have continued to be paramount during the crisis. However, what the current crisis has forced boards to recognize is that a combination of specialized and diversified skillsets and characteristics will produce good corporate governance in and after 2020.

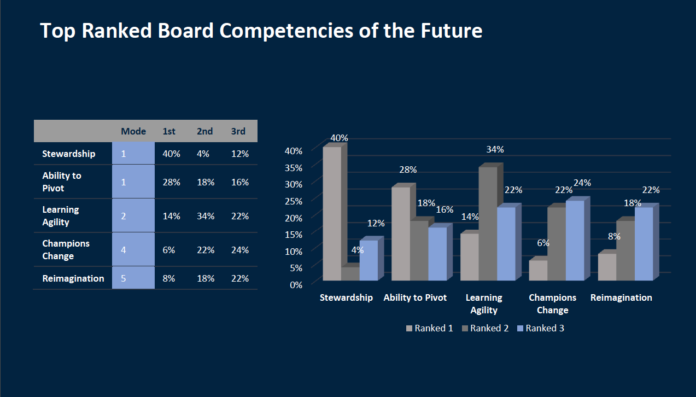

In addition to listening to the characteristics discussed in the recent roundtables, RSR Partners polled more than 250 public company board members of Fortune 50-1000 companies to identify the traits they hope to see emerge in this generation of board members. The results indicated that stewardship, the ability to pivot and learn agility, to be a champion of change, and to be capable of reimagination will be most needed by the directors charged with steering their boards in the “new normal.”

Now the consensual German model of business has suffered multiple mechanical failures. Wirecard, the payments group that bolstered German tech credentials, has imploded in fraud. Bayer is taking up to $11bn in charges mostly triggered by a disastrous US takeover. Once-proud conglomerates Siemens and Thyssenkrupp are shrinking. Volkswagen’s service life shortens each time Tesla’s outlook improves.

(…) Germany, can we talk? “Sure. I’m driving but I’m German so that’s second nature,” jokes an economist via his hands-free, “I don’t think there is any common thread between Wirecard and these other examples.” According to him, the worst accidents occur when German business adopts US ways. Wirecard had a two-tier board structure, like most German businesses. But its supervisory board was seemingly full of corporate yespersons, not vigilant workers as governance rules dictate. And the group was led by a bossy entrepreneur. Kenneth Amaeshi, a professor of business at Edinburgh university, disagrees with such exceptionalism. He believes the Wirecard scandal puts German stakeholder capitalism “in the dock”. It points to a structural weakness of regulation, he says. He is right.

(…) Corporate governance must be overhauled this time.

Supervisory boards must shrink, meet more often and include more independent directors. Regulators must adopt the adversarial approach of US peers. Industrial giants should unbundle further to create a new tier of focused medium-sized businesses. Siemens’ 2018 flotation of Healthineers, a healthcare equipment unit, shows what can be done. Germany’s biggest challenge is spurring investment in disruptive technology. Business has depended on debt finance from risk-averse investors. But there is no lack of equity, as Guntram Wolff of Bruegel, a think-tank, points out. It features as retained corporate earnings rather than footloose investment capital. This is reflected in total equity of some €1.2tn on the balance sheets of Germany’s top 100 quoted companies, according to S&P Global data. Tax breaks are needed to chivvy more of this capital into start-ups and electric vehicle development. It would be a shame to waste two good crises — the meltdown of the German model plus coronavirus. Moreover, support is growing worldwide for stakeholder capitalism, in which social and environmental goals rank alongside profits. Germany just needs to reduce its emphasis on safe jobs for workers and well-networked managers. A little less consensus can make the German model roadworthy again.

Si les marchés et les infrastructures ont bien fonctionné durant la crise sanitaire, les déséquilibres initialement présents se sont accentués et les tensions géopolitiques demeurent. Au-delà des nombreux défis que présente le financement de la relance économique post-Covid 19, une nouvelle vulnérabilité en soi, la cartographie met en avant une montée des risques pour la stabilité financière avec une possible nouvelle correction des marchés et la solvabilité dégradée de nombreuses entreprises.

Vous pouvez accéder au communiqué de presse ici, ainsi qu’au document complet juste ici.

À noter ici que l’information extrafinancière fait figure de risque !

Un besoin croissant de données extra-financières comparables et de qualité, non satisfait pour le moment et qui présente des risques pouvant obérer le développement pérenne de la finance durable […] La définition d’un reporting plus contraignant, faisant l’objet d’une harmonisation maximale, dans le cadre de la prochaine révision de la directive extra-financière, pourrait de ce point de vue également contribuer à des améliorations significatives.