actualités internationales | Page 8

actualités internationales Gouvernance mission et composition du conseil d'administration normes de droit Responsabilité sociale des entreprises

Grèce : 25 % de femmes au CA imposé par la loi

Ivan Tchotourian 9 juillet 2020

Minerva Analytics apporte une belle mise à jour à la problématique de la diversité en m’apprenant que la Grèce vient de renforcer son dispositif juridique en matière de féminisation : « Greek companies will soon be mandated to meet a 25% female quota on their boards following a landmark decision for gender diversity ».

Extrait :

The quota requirement has been included as an amendment to the bill transposing the EU Shareholder Rights Directive II (SRD II) into Greek law, and is the result of a consultation led by a group of academics specialising in corporate governance.

(…)

Overall, the directive is designed to encourage companies away from short-termism, focusing on areas such as director remuneration. However, the Greek amendment marks the first time it has been used to tackle the EU’s poor record on gender diversity at a board level.

According to the European Commission’s 2019 report on equality between men and women, since 2015, progress on corporate gender inclusivity has stalled. As of October 2018, the proportion of women on the boards of the EU’s biggest companies was only 26.7%.

Within this, France was the only EU member state with at least 40% female representation at board-level, while women account for less than a third of board-level positions in Italy, Sweden, Finland and Germany.

According to the same data, women made up less than 10% of board members in Greece.

À la prochaine…

actualités internationales Divulgation Gouvernance normes de droit

Tranparence en matière de COVID-19 : quel bilan des entreprises aux États-Unis ?

Ivan Tchotourian 9 juillet 2020 Ivan Tchotourian

David Larcker, Bradford Lynch, Brian Tayan et Daniel Taylor publient un texte qui revient sur la transparence des ghrandes entreprises américaines en matière de COVID-19 « The Spread of Covid-19 Disclosure » (29 juin 2020). Un document plein de statistiques et de tendances sur la transparence… vraiment intéressant sachant que l’enjeu de la question n’est pas à négliger.

Extrait :

The COVID-19 pandemic presents an interesting scenario whereby an unexpected shock to the economic system led to a rapid deterioration in the economic landscape, causing sharp changes in performance relative to expectations just a few months prior. For most companies, the pandemic has been detrimental. For a few, it brought unexpected demand. In many cases, supply chains have been strained, causing ripple effects that extend well beyond any one company.

How do companies respond to such a situation? What choices do they make, and how much transparency do they offer? How does disclosure vary in a setting where the potential impact is so widely uncertain? The COVID-19 pandemic provides a unique setting to examine disclosure choices in a situation of extreme uncertainty that extends across all companies in the public market. This devastating outlier event provides a rare glimpse into disclosure behavior by managers and boards.

Why This Matters

- The COVID-19 pandemic provides a unique opportunity to examine disclosure practices of companies relative to peers in real time about a somewhat unprecedented shock that impacted practically every publicly listed company in the U.S. We see that decisions varied considerably about whether to make disclosure and, if so, what and how much to say about the pandemic’s impact on operations, finances, and future. What motivates some companies to be forthcoming about what they are experiencing, while others remain silent? Does this reflect different degrees of certitude about how the virus would impact their businesses, or differences in managements’ perception of their “obligations” to be transparent with the public? What does this say about a company’s view of its relation and duty to shareholders?

- In one example, we saw a consumer beverage company make zero references to COVID-19 in its SEC filings and website, despite the virus plausibly having at least some impact on its business. In another example, we saw a company claim no material changes to its previously reported risk factors when managers almost certainly had relevant information about the virus and the likely impact on sales and operations. What discussion among the senior managers, board members, external auditor, and general counsel leads to a decision to make no disclosures? What should shareholders glean from this decision, particularly in light of peer disclosure?

- The COVID-19 pandemic represents a so-called “black swan” event that inflicted severe and unexpected damage to wide swaths of the economy. What strategic insights will companies learn from this event? Can boards use these insights to prepare for other possible outlier events, such as climate events, terrorism, cyber-attacks, pandemics, and other emergencies? Should these insights be disclosed to shareholders?

À la prochaine…

actualités internationales Gouvernance mission et composition du conseil d'administration

What The Director Of The Future Will Need To Succeed

Ivan Tchotourian 8 juillet 2020 Ivan Tchotourian

Board Member vient de publier une étude sur les CA du futur : « What The Director Of The Future Will Need To Succeed ». Intéressant dans le monde post COVID-19.

Merci à Louise Champoux-Paillé de l’information !

Extrait :

“The future of business will be different,” surmised a director on a recent virtual board roundtable hosted by RSR Partners, “in ways we can’t anticipate in this moment. Our board is focused on assessing whether all our directors are truly ready for what’s coming.”

Over the past few months, RSR Partners hosted more than a dozen roundtables for sitting directors, providing a forum for the participants to share what their boards are learning as they navigate the current crisis and pivot into the “new normal.” While tackling topics as diverse as commercial strategy, operations, health and safety, and the future of business, one theme was pervasive throughout the discussions: leadership and stakeholders will be looking to the boardroom for guidance, and board members not only need to have the requisite experience and skills to confidently provide direction, but the leadership characteristics that will allow them to be effective.

Fundamentally, the global business disruption and current uncertainty has created a need for a higher level of involvement from board members. “This is a time to have board members who have experienced really tough issues, such as major ecessions, difficult mergers, major cost cutting, insolvency and bankruptcy, and top management departures, along with experience in reinventing companies, including supply chain, product engineering and simplification, digital transformation, offshore manufacturing and procurement, sale of subsidiaries, and comprehensive refinancing,” stated Edward A. Kangas, former Chairman and CEO of Deloitte Touche. “This is not a time for deep thinking. It’s time for people with real experience who know how to oversee and support management in a time of crisis and reinvention.” (Mr. Kangas currently serves on the following boards: Deutsche Bank USA Corp., Intelsat SA, VIVUS, Inc., and Hovnanian Enterprises, Inc.).

Characteristics of Directors Who Succeed in the “New Normal”

From a practical perspective, there is now a higher premium placed on a director’s proven ability to navigate a business through a crisis while mitigating risk and understanding how and when to pull the levers that will impact balance sheets. The demand to optimize results, sustain business, and adapt to changes in a regional and global market has increased alongside the time commitment and attention to detail required of directors to address these issues. Normal requirements for sound governance, audit oversight, compensation strategies, business performance goals, and succession of key leadership have continued to be paramount during the crisis. However, what the current crisis has forced boards to recognize is that a combination of specialized and diversified skillsets and characteristics will produce good corporate governance in and after 2020.

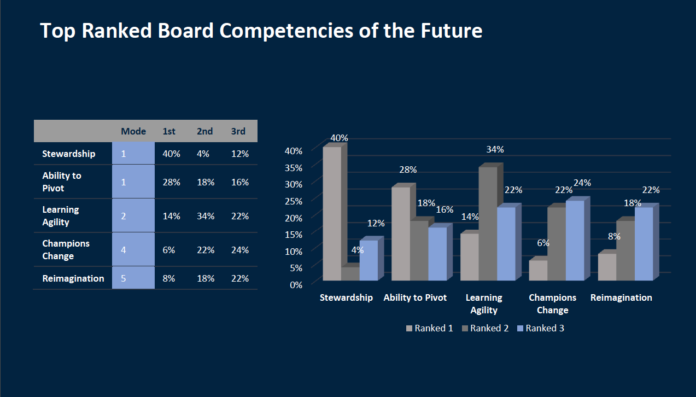

In addition to listening to the characteristics discussed in the recent roundtables, RSR Partners polled more than 250 public company board members of Fortune 50-1000 companies to identify the traits they hope to see emerge in this generation of board members. The results indicated that stewardship, the ability to pivot and learn agility, to be a champion of change, and to be capable of reimagination will be most needed by the directors charged with steering their boards in the “new normal.”

1. Stewardship

2. Ability to Pivot

3. Learning Agility

4. Champions of Change

5. Reimagination

À la prochaine…

actualités internationales Gouvernance Normes d'encadrement

German corporations — and regulation — are in the dock

Ivan Tchotourian 7 juillet 2020 Ivan Tchotourian

Intéressant article du Financial Times du 1er juillet 2020 qui revient sur le modèle allemand « German corporations — and regulation — are in the dock ».

Extrait :

Now the consensual German model of business has suffered multiple mechanical failures. Wirecard, the payments group that bolstered German tech credentials, has imploded in fraud. Bayer is taking up to $11bn in charges mostly triggered by a disastrous US takeover. Once-proud conglomerates Siemens and Thyssenkrupp are shrinking. Volkswagen’s service life shortens each time Tesla’s outlook improves.

(…) Germany, can we talk? “Sure. I’m driving but I’m German so that’s second nature,” jokes an economist via his hands-free, “I don’t think there is any common thread between Wirecard and these other examples.” According to him, the worst accidents occur when German business adopts US ways. Wirecard had a two-tier board structure, like most German businesses. But its supervisory board was seemingly full of corporate yespersons, not vigilant workers as governance rules dictate. And the group was led by a bossy entrepreneur. Kenneth Amaeshi, a professor of business at Edinburgh university, disagrees with such exceptionalism. He believes the Wirecard scandal puts German stakeholder capitalism “in the dock”. It points to a structural weakness of regulation, he says. He is right.

(…) Corporate governance must be overhauled this time.

Supervisory boards must shrink, meet more often and include more independent directors. Regulators must adopt the adversarial approach of US peers. Industrial giants should unbundle further to create a new tier of focused medium-sized businesses. Siemens’ 2018 flotation of Healthineers, a healthcare equipment unit, shows what can be done. Germany’s biggest challenge is spurring investment in disruptive technology. Business has depended on debt finance from risk-averse investors. But there is no lack of equity, as Guntram Wolff of Bruegel, a think-tank, points out. It features as retained corporate earnings rather than footloose investment capital. This is reflected in total equity of some €1.2tn on the balance sheets of Germany’s top 100 quoted companies, according to S&P Global data. Tax breaks are needed to chivvy more of this capital into start-ups and electric vehicle development. It would be a shame to waste two good crises — the meltdown of the German model plus coronavirus. Moreover, support is growing worldwide for stakeholder capitalism, in which social and environmental goals rank alongside profits. Germany just needs to reduce its emphasis on safe jobs for workers and well-networked managers. A little less consensus can make the German model roadworthy again.

À la prochaine…

actualités internationales Gouvernance normes de droit parties prenantes place des salariés Responsabilité sociale des entreprises

Bulletin Joly Travail : deux articles à lire

Ivan Tchotourian 7 juillet 2020 Ivan Tchotourian

Dans le dossier Droit du travail et droit des sociétés : questions d’actualité réalisé sous la coordination scientifique de Jérôme Chacornac et Grégoire Duchange, je signale deux articles intéressants touchant les thématiques du blogue :

À la prochaine…

actualités internationales engagement et activisme actionnarial Gouvernance normes de droit

Activisme actionnarial : l’AMF France prend position

Ivan Tchotourian 4 juillet 2020 Ivan Tchotourian

Le 28 avril 2020, l’Autorité des marchés financiers a proposé des mesures ciblées pour améliorer la transparence vis-à-vis du marché et le dialogue entre les émetteurs et les actionnaires.

Pour en savoir plus : ici.

Extrait :

L’engagement actif des actionnaires dans la vie des sociétés cotées est une condition de leur bon fonctionnement et d’une saine gouvernance. A cet égard, l’AMF considère qu’il doit être encouragé. Pour le régulateur, la problématique n’est donc pas d’empêcher l’activisme mais d’en fixer les limites et de se donner la capacité à en maîtriser les excès.

En l’état de la réglementation, l’AMF considère qu’il n’est pas nécessaire de faire évoluer de manière importante le cadre juridique applicable.

Les propositions de l’AMF visent à :

- améliorer l’information sur la montée au capital et la connaissance de l’actionnariat, en abaissant le premier seuil légal de déclaration et en rendant publiques les déclarations faites à la société sur le franchissement des seuils fixés dans ses statuts ;

- assurer une meilleure information au marché sur l’exposition économique des investisseurs, en complétant les déclarations de positions courtes par une information sur les instruments de dette également détenus (obligations, credit defaults swaps par exemple). L’AMF soutiendra ces propositions au niveau européen ;

- promouvoir un dialogue ouvert et loyal entre les sociétés cotées et leurs actionnaires : l’AMF complètera son guide sur l’information permanente et la gestion de l’information privilégiée afin d’y ajouter des développements sur le dialogue actionnarial. Elle complètera également sa doctrine afin de préciser que les émetteurs peuvent apporter toute information nécessaire au marché en réponse à des déclarations publiques les concernant, même en cours de périodes de silence, sous réserve du respect des règles sur les abus de marché. Elle recommandera, par ailleurs, à tout actionnaire qui initie une campagne publique de communiquer sans délai à l’émetteur concerné les informations importantes qu’il adresserait aux autres actionnaires ;

- accroître les capacités d’analyse et de réaction de l’AMF afin de lui permettre d’apporter des réponses rapides et adaptées lorsque les circonstances l’exigent : via, par exemple, l’instauration d’un pouvoir d’astreinte en matière d’injonction administrative et d’une faculté d’ordonner à tout investisseur, et non plus seulement à un émetteur, de procéder à des publications rectificatives ou complémentaires en cas d’inexactitude ou d’omission dans ses déclarations publiques.

À la prochaine…

actualités internationales Gouvernance parties prenantes Responsabilité sociale des entreprises

Time to Rethink the S in ESG

Ivan Tchotourian 4 juillet 2020 Ivan Tchotourian

Intéressant billet sur le Harvard Law School Forum on Corporate Governance mettant en avant l’importance prise par le « S » des critères ESG : « Time to Rethink the S in ESG » (Jonathan Neilan, Peter Reilly, et Glenn Fitzpatrick, 28 juin 2020).

Extrait :

In advising companies on protecting and enhancing corporate reputation—through good and bad times—our guiding principle is to ‘do the right thing’. Simple as it sounds, it is reflected in the adage that ‘good PR starts with good behaviour’. This guiding principle also translates to building your ‘S’ credentials. While the various ESG criteria of the reporting frameworks and ratings agencies are a useful guide, our consistent approach in advising companies is for them to take the steps they believe are genuinely in the best interest of the company and its wider stakeholders. Not every decision will meet the expectations of every stakeholder; but it’s a good place to start.

As the wider sustainability agenda also drives more rapid and fundamental change in global markets and technology innovation, properly considering the pressure from public policy and evolving legal requirements, as well as the needs of key stakeholders, is key to understanding what is (and will be seen as) ‘good behaviour’.

As the focus on the ‘S’ grows, companies will need to shift from a reactive to a proactive position. While governance and environmental data is readily available for most companies, the same is not true of the ‘S’. The leeway companies have been afforded on the ‘S’ in the past is unlikely to continue; and, expectations of (and measurement by) rating agencies and investors will continue to increase.

In light of the economic shocks and social upheaval across the globe, demands from stakeholders—most pressingly investors and Governments—will reach a crescendo over the coming six months. As the sole arbiter of much of the information needed to value the ‘S’ in ESG, companies have an opportunity to demonstrate a willingness to shift levels of transparency before they are forced to do so. Companies understandably tend to highlight the efforts they make, often through their corporate social responsibility or communications departments, rather than the higher-cost, higher-risk analysis of the effectiveness of those efforts. Fundamentally, hastened by the emergence of a global pandemic, the world recognises the significance of the risk that failure to address stakeholder interests and expectations represents to business. That shift can be identified as demand for evidence of positive outcomes as opposed to simply efforts or policies.

As we noted in our 2019 Paper, ESG will never replace financial performance as the primary driver of company valuations. Increasingly, however, it is proving to drive the cost of capital down for companies while playing a hugely important role in companies’ risk management frameworks. Most immediately, companies should get a firm handle on how comprehensive their policies, procedures and data are in the five areas listed through a candid audit, as well as other factors material to their businesses’ long-term success. However, this is just a first step and companies must build a narrative and strategy around disclosure for all future annual reports and, where appropriate, market communications. Investors of all sizes are increasingly driving this factor home to Boards and management. In just one week at the end of April, human capital management proposals from As You Sow, a non-for-profit foundation, received 61% and 79% support at two S&P 500 companies, Fastenal and Genuine Parts, respectively. The two companies must now prepare reports on diversity and inclusion, and describe the company’s policies, performance, and improvement targets related to material human capital risks and opportunities as designed by a small shareholder—as opposed to crafting an approach and associated disclosure themselves.

What has become clear over the past three months is that a host of stakeholders, including many investors, will expect a sea-change in their access to information and company practices. While there is no requirement to be the first mover on this, those that are laggards will face avoidable challenges and a rising threat to their ‘licence to operate’.

À la prochaine…