autres publications normes de marché

Prise en compte des critères ESG : les mythes s’effondrent

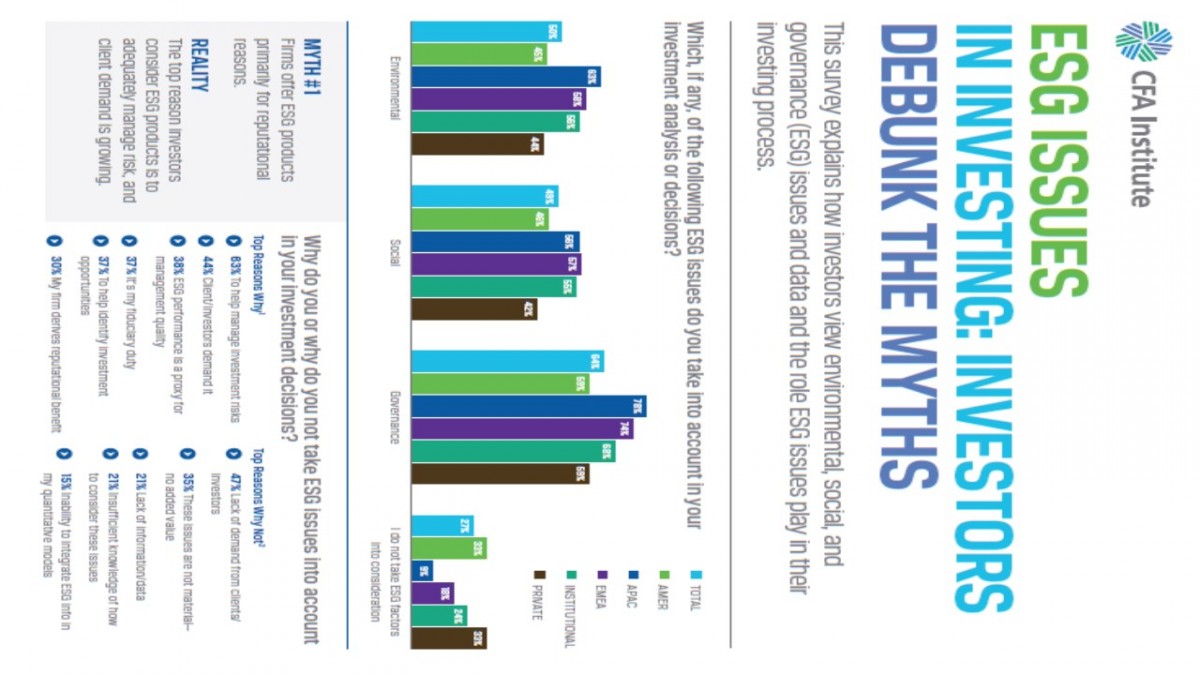

Bonjour à toutes et à tous, intéressante étude publiée à la mi-août par l’IRRC Institute (ESG Issues in Investing: Investors Debunk the Myths) selon laquelle : « Almost Three Quarters of Investment Professionals Use Environmental, Social & Governance Information When Making Investment Décisions. New CFA Institute survey highlights board accountability, human capital and executive compensation as important issues ».

Voici le bilan :

- Risk evaluation: Sixty-three percent of survey respondents said they consider ESG in the investment decision making process to help manage investment risks, 44 percent say that their clients/investors demand it and 38 percent said ESG performance is a proxy for management quality.

- Top three issues in decision-making: Survey respondents ranked board accountability, human capital, and executive compensation as the issues most important to investment analysis and decision-making.

- Regional breakdown: A high proportion of CFA Institute members in the Asia-Pacific region considered ESG issues (78 percent), followed closely by members in the Europe, Middle East, and Africa (EMEA) region (74 percent). Respondents in the Americas region were the least likely to use ESG information in their decision-making process, but, even there, a solid majority (59 percent) do use ESG factors.

- ESG integration in the investment process: Fifty-seven percent of respondents integrate ESG into the whole investment analysis and decision-making process, while 38 percent use best-in-class positive alignment; 36 percent use ESG analysis for exclusionary screening.

- ESG disclosures: Sixty-one percent of survey respondents agreed that public companies should be required to report at least annually on a cohesive set of sustainability indicators in accordance with the most up-to-date reporting framework. In addition, 69 percent of these respondents say ESG disclosures should be subject to independent verification. Furthermore, of these, 44 percent believe that verification at a high level of assurance, similar to an audit, is necessary. Another 46 percent believe limited verification, or a lower level of assurance, is necessary. When this group was asked how much should be spent on independent verification, responses varied from 10 percent to 100 percent of the cost of an audit of financial statements.

À la prochaine…

Ivan Tchotourian