Responsabilité sociale des entreprises

devoir de vigilance finance sociale et investissement responsable Gouvernance parties prenantes Responsabilité sociale des entreprises

Retour sur la 2e édition de la grande conférence Measuring Beyond

Ivan Tchotourian 12 mars 2025

Merci à l’École des dirigeants d’HEC d’assurer le suivi de sa grande conférence récente sur l’impact social : « Retour sur la 2e édition de la grande conférence Measuring Beyond ».

En voici quelques extraits :

Dans ce contexte, les organisations doivent repenser leur rapport à la performance, notamment en adoptant une vision de capitalisme partenaire, souligne Geneviève Fortier. « En réfléchissant à l’intérêt de l’ensemble des parties prenantes, et non seulement à celui des actionnaires, cela nous force à concilier les notions de profitabilité et de responsabilité sociale. Et au final, les organisations sont non seulement plus responsables, mais plus résilientes en cas de turbulences. »

L’engagement des communautés est crucial, en particulier dans un contexte de collaboration avec les Premières Nations. Pour y arriver, les organisations doivent transformer leurs objectifs stratégiques en buts communs, a expliqué Marya Besharov, professeure à la Saïd Business School de l’Université d’Oxford. « Lorsque nous changeons de perspective pour penser à la fois au « nous » et au « eux », cela nous aide à aborder cet engagement très différemment. » Plus précisément, les entreprises devraient miser sur une relation transformationnelle, où la communauté est pleinement intégrée au processus décisionnel et partage les bénéfices.

La dimension financière est souvent négligée quand il s’agit de projets de nature sociale, note Ludovic Phalippou, professeur à la Saïd Business School de l’Université d’Oxford qui a présenté un exemple concret : celui de la construction de logements sociaux et abordables sur les terrains d’une ancienne prison, à New York.

Avec l’adoption de réglementations comme la Loi sur la lutte contre le travail forcé et le travail des enfants dans les chaînes d’approvisionnement en 2024, les entreprises doivent non seulement surveiller leurs propres activités, mais aussi celles de leurs fournisseurs. (…) C’est aussi un élément transformateur puisque les entreprises peuvent accompagner leurs fournisseurs pour se conformer aux réglementations et, par le fait même, améliorer leur bilan social, estime Hélène V. Gagnon, cheffe de la direction du Capital humain et du développement durable chez CAE. « Du point de vue environnemental, nous avons aidé nos fournisseurs à trouver des opportunités de décarbonation leur permettant de réduire leurs coûts, ce qui nous a permis d’avoir une meilleure vision d’ensemble de ces opérations. » C’est la même chose au point de vue social, fait-elle valoir. Plus qu’une question de conformité, les grandes organisations peuvent influencer toute leur chaîne d’approvisionnement. Un levier complexe, mais puissant.

« Pour atteindre la carboneutralité, il n’est pas nécessaire que toutes les entreprises soient carboneutres, a expliqué la spécialiste. De par leur nature, certaines organisations peuvent nécessairement faire plus que les autres. C’est donc en cumulant tous ces efforts qu’il sera possible d’y arriver. » Un objectif qui aura certes un effet positif sur l’environnement, mais aussi sur les humains qui doivent composer avec feux de forêt, inondations et autres effets des changements climatiques, conclut-elle.

À la prochaine…

Gouvernance parties prenantes Responsabilité sociale des entreprises

Responsabilité Sociale des Entreprises, Développement Durable et Théorie des Parties Prenantes – Une perspective internationale

Ivan Tchotourian 29 juillet 2024

Bravo à mes collègues Odile Uzan et Émilie Hennequin pour la parution de cet ouvrage collectif : « Responsabilité Sociale des Entreprises, Développement Durable et Théorie des Parties Prenantes – Une perspective internationale » (ESKA, 2024).

Résumé :

Dans un 21e siècle toujours aussi turbulent et complexe que le 20e, mais également marqué par une prise de conscience des enjeux écologiques, se repose la question d’un cadre susceptible d’offrir des perspectives pour un écosystème mondial responsable, durable et partenarial (incluant toutes les Parties Prenantes). Cet ouvrage propose une réflexion en croisant quatre angles d’éclairage portant sur : la compréhension du cadre fondateur de la RSE, de son lien indissociable avec le Développement Durable (DD), du rôle indéniable de la Théorie des Parties Prenantes (TPP) pour améliorer sa base partenariale et son opérationnalisation managériale, et de la perspective internationale qui révèle le « mix » entre pressions « cognitives, normatives et coercitives », que construit chaque pays pour s’inscrire et contribuer à cette dynamique mondiale.

C’est donc par la confrontation du triptyque RSE/DD/TPP au mix (pressions cognitives, normatives et coercitives) que cet ouvrage propose aux universitaires et aux praticiens de l’entreprise des cadres d’analyse des dynamiques à l’œuvre et des leviers actionnables afin d’instituer, au niveau international et dans un souci de performance globale, les relations nécessaires entre l’Entreprise et la Société.

À la prochaine…

Base documentaire Gouvernance loi et réglementation parties prenantes Responsabilité sociale des entreprises

Projet de loi sur la protection des retraites

Ivan Tchotourian 10 avril 2022 Ivan Tchotourian

Le 29 mars 2022, le projet de loi C-264 Loi modifiant la Loi sur la faillite et l’insolvabilité et la Loi sur les arrangements avec les créanciers des compagnies (régimes de pension et régimes d’assurance collective) a été déposé à la Chambre des communes par la députée Marilène Gill. Ce projet s’attaque de nouveau à la question de la protection des participants à un régime de retraite.

Rappelons une chose : en l’état actuel, aucune de ces deux lois n’accorde de statut prioritaire aux « paiements spéciaux » requis pour maintenir un régime de retraite en bonne situation financière ou pour honorer les promesses du régime déficitaire en cas de terminaison.

Espérons que ce projet de loi aura plus de succès que les projets C-384 et C-372 déposés en 2017, C-405 et S-253 déposés en 2018 ou encore plus récemment, C-253 déposé en 2020. Pour le gouvernement fédéral et les citoyens canadiens, est-il tolérable que le Canada protège encore si peu les droits de ses retraités en contexte de faillite ou d’insolvabilité ?

- Pour accéder au projet de loi : ici

À la prochaine…

devoir de vigilance Gouvernance Normes d'encadrement Responsabilité sociale des entreprises

Raison d’être et devoir de vigilance

Ivan Tchotourian 4 avril 2022 Ivan Tchotourian

Bel article de réflexion offert par Beate Sjåfjell et Jukka Mähönen (professeurs à Oslo) sur la directive vigilance : « Corporate Purpose and the EU Corporate Sustainability Due Diligence Proposal » (Oxford Business Law Blog, 25 février 2022).

Extrait

Taking sustainability seriously: sustainable value creation within planetary boundaries

The question of how to secure the contribution of our businesses to the fundamental transformation to sustainability is not one that should be responded to in the ideological and emotional way as we have seen in some of the responses when the Sustainable Corporate Governance initiative was launched. Now that the Directive proposal is out, we encourage all who wish to participate in the discussion to lay aside any ideological ‘shareholder vs stakeholders’ viewpoints. That is not what is at stake. While the IPCC report on climate change of 2021 has been referred to as ‘code red for humanity’, planetary boundaries research shows that reality is even more grim – we have a whole set of code reds for humanity and they are increasing in number (as the latest planetary boundaries research shows), and the status for the European Union is not good. Working towards sustainability also entails questions of social justice – just as we cannot silo environmental issues into various categories to be dealt with separately, we cannot separate environmental and social issues. These are all interconnected elements. All of these issues must be dealt with simultaneously. The sustainability challenges of our time are complex and interconnected and attempting to silo sustainability work into dealing piecemeal with isolated elements will not work.

While there seems generally to be an increasing consensus among governments and businesses on the need to integrate sustainability into the governance of our globalized businesses, the attempts to do this so far seem to have been based on three principles: a) as few clear and enforceable rules as possible, b) support voluntary measures although they haven’t worked so far, and c) if we must regulate, be sure to leave company law out of the picture.

However, to get real about integrating sustainability, we need to go to company law, which is the regulatory infrastructure for decision-making in business. As all company law scholars who have analysed the sources know, company law gives a broad discretion to corporate boards and by extension senior management in their corporate governance. There is, in other words, space within the current company law and corporate governance systems to steer businesses in more sustainable directions. This has been used by some as an argument for the sanctity of company law – no need for change, move on, nothing to see here! The problem is that this discretionary space is taken up by the social norm of shareholder primacy. We therefore suggest, on the basis of over a decade of multijurisdictional comparative analyses of the drivers for and the barriers to sustainable business, that company law must take back that space and clarify why we have companies (corporate purpose) and give a principle-based instruction to boards on how to do their jobs in this era that is defined by the extreme unsustainabilities resulting from business as usual.

Sustainable value creation is already an emerging concept in corporate governance all over the world. What needs to be done is to position sustainable value creation within the ecological limits of our planet. We therefore propose both ‘sustainable value’ and ‘planetary boundaries’ as general clauses in company law, the content of which gradually can be firmed up as practice develops. This doesn’t mean we don’t think there should be any guidance in the law – quite the opposite, as we see the need to ensure that business does not take these two concepts and turn them into opportunities for greenwashing, bluewashing or ‘sustainability washing’. Integrating these concepts into the duties of the board is therefore also paramount, outlining this in a way that provides legal certainty.

Avoiding the shareholder vs stakeholder trap does not mean that we do not in our proposal encompass a wide variety of interests affected by the company’s business. However, while involving affected communities, trade unions, and civil society is crucial, a mere canvassing of ‘stakeholder interests’ and giving priority to the ones that make themselves heard the most is insufficient, misleading and potentially destructive for the overarching purpose of sustainable value creation. The backdrop must always be the interconnected complexities and the vulnerability of the often-unrepresented groups (whether invisible workers deep in the global value chains, Indigenous communities, or future generations), and the aim of a sustainable future within planetary boundaries.

Under pressure: the proposed Corporate Sustainability Due Diligence Directive

The European Commission’s Corporate Sustainability Due Diligence Directive proposal, presented on 23 February 2022, aims to put into place mandatory and harmonised sustainability due diligence rules in the European Economic Area, in recognition of the insufficiency of voluntary action by business and the regulatory chaos that business faces in its cross-border activities.

The proposed Directive is appropriately named ‘Corporate Sustainability Due Diligence’, resonating in title with the proposed Corporate Sustainability Reporting Directive. It is positive that the Corporate Sustainability Due Diligence Directive proposal clarifies which environmental and human rights issues are intended to be included. However, a broader approach is needed, drawing on a research-based concept of sustainable value creation within planetary boundaries.

The proposal builds on a due diligence duty for the members of the board and the chief executive officer of the company. It reflects the international human rights and environmental international law obligations and concretises the steps of the due diligence process. There is, however, a danger of box ticking instead of principle-based evaluations of risks of unsustainability.

There are proposals for both public and private enforcement, including civil liability for the board members and the chief executive officer, which makes this proposal different from much of what we have otherwise seen in the corporate sustainability area. The scope of the proposal is however extremely narrow, excluding in its direct application all small and medium-sized enterprises, and covering only some 13,000 EU companies and some 4,000 third-country companies.

The proposal takes an important core company law step, which we have advocated in our work, namely to clarify that the duty of the board (strangely formulated as a duty, in Anglo-Saxon speak, for all ‘directors’) is to promote the interests of the company. Wisely, there is no attempt to harmonize this (and especially not by including some kind of stakeholder language), rather leaving the content of the interests of the company to the variety of company law regimes in Europe. What is missing, however, is further situating this duty within an overarching purpose of sustainable value creation within planetary boundaries, which would have given a clearer sustainability-oriented framing for the whole proposal.

The proposal does employ misleading stakeholder language in the consultation duties as part of due diligence, where it would have been better to specify that the consultation should take place with affected communities, groups and people.

The proposed Directive is clearly a product of the tension resulting from, on the one hand, the social norm of shareholder primacy and the drive to keep company law untouched by sustainability issues, and on the other hand, the willingness to make necessary changes to mitigate the extreme unsustainabilities of business as usual. We see this in the way core company law issues are relegated to the end of the proposal. It would have been much more logical to set out clearly in the beginning of the proposed Directive the core duties of the boards to ensure that sustainability due diligence is used as a key tool for integrating sustainability into the entire business of the company.

The Directive proposal needs to be strengthened on a number of points, and it is now to be discussed further by the European Parliament and the Council, before it can be adopted with possible revisions. We strongly recommend that subsequent work with the Directive proposal be based on a research-based concept of sustainability and take company law and corporate governance seriously, rather than allowing the misleading shareholder vs stakeholder dichotomy to set the parameters for continued siloing of core company law as the regulatory infrastructure for corporate decision-making.

À la prochaine…

Gouvernance Normes d'encadrement objectifs de l'entreprise parties prenantes Responsabilité sociale des entreprises Valeur actionnariale vs. sociétale

Actionnaires et parties prenantes : quelle gouvernance à venir ? : un beau texte de l’IGOPP

Ivan Tchotourian 11 mars 2021 Ivan Tchotourian

À l’été 2020, Yvan Allaire et François Dauphin ont publié une belle tribune dans Le Devoir intitulé : « Actionnaires et parties prenantes : quelle gouvernance à venir ? ». Ils démontrent tout leur scepticisme en mettant en lumière les zones d’ombre du modèle des parties prenantes.

En raison surtout d’une véritable révolution des modes et quanta de rémunération des hauts dirigeants, les sociétés cotées en bourse en sont venues graduellement depuis les années ’80s à œuvrer presqu’exclusivement pour maximiser la création de valeur pour leurs actionnaires.

Tout au cours de ces 40 ans, ce modèle de société fut critiqué, décrié, tenu responsable pour les inégalités de revenus et de richesse et pour les dommages environnementaux. Toutefois, tant que cette critique provenait d’organisations de gauche, de groupuscules sans appui populaire, les sociétés pouvaient faire fi de ces critiques, les contrant par des campagnes de relations publiques et des ajustements mineurs à leur comportement.

Soudainement, pour des raisons multiples, un peu mystérieuses, cette critique des entreprises et du « capitalisme » a surgi du cœur même du système, soit, de grands actionnaires institutionnels récemment convertis à l’écologie. Selon cette nouvelle perspective, les sociétés cotées en bourse devraient désormais non seulement être responsables de leurs performances financières, mais tout autant de l’atteinte d’objectifs précis en matière d’environnement (E), d’enjeux sociaux (S) et de gouvernance (G). Pour les grandes entreprises tout particulièrement, le triplé ESG, de facto le modèle des parties prenantes, est devenu une caractéristique essentielle de leur gouvernance.

Puis, signe des temps, quelque 181 PDG des grandes sociétés américaines ont pris l’engagement, il y a un an à peine, de donner à leurs entreprises une nouvelle «raison d’être » (Purpose en anglais) comportant un « engagement fondamental » envers clients, employés, fournisseurs, communautés et leur environnement et, ultimement, les actionnaires.

De toute évidence, le vent tourne. Les questions environnementales et sociales ainsi que les attentes des parties prenantes autres que les actionnaires sont devenues des enjeux incontournables inscrits aux agendas politiques de presque tous les pays.

Les fonds d’investissement de toute nature bifurquèrent vers l’exigence de plans d’action spécifiques, de cibles mesurables en matière d’ESG ainsi qu’un arrimage entre la rémunération des dirigeants et ces cibles.

Bien que louable à bien des égards, le modèle de « parties prenantes » soulève des difficultés pratiques non négligeables.

1. Depuis un bon moment la Cour suprême du Canada a interprété la loi canadienne de façon favorable à une conception « parties prenantes » de la société. Ainsi, un conseil d’administration doit agir exclusivement dans l’intérêt de la société dont ils sont les administrateurs et n’accorder de traitement préférentiel ni aux actionnaires ni à toute autre partie prenante. Toutefois la Cour suprême n’offre pas de guide sur des sujets épineux conséquents à leur conception de la société : lorsque les intérêts des différentes parties prenantes sont contradictoires, comment doit-on interpréter l’intérêt de la société? Comment le conseil d’administration devrait-il arbitrer entre les intérêts divergents des diverses parties prenantes? Quelles d’entre elles devraient être prises en compte?

2. Comment les entreprises peuvent-elles composer avec des demandes onéreuses en matière d’ESG lorsque des concurrents, domestiques ou internationaux, ne sont pas soumis à ces mêmes pressions?

3. À un niveau plus fondamental, plus idéologique, les objectifs ESG devraient-ils aller au-delà de ce que la réglementation gouvernementale exige? Dans une société démocratique, n’est-ce pas plutôt le rôle des gouvernements, élus pour protéger le bien commun et incarner la volonté générale des populations, de réglementer les entreprises afin d’atteindre les objectifs sociaux et environnementaux de la société? Mais se peut-il que cette conversion des fonds d’investissement aux normes ESG et la redécouverte d’une « raison d’être » et des parties prenantes par les grandes sociétés ne soient en fait que d’habiles manœuvres visant à composer avec les pressions populaires et atténuer le risque d’interventions « intempestives » des gouvernements?

4. Quoi qu’il en soit, le changement des modes de gestion des entreprises, présumant que cette volonté est authentique, exigera des modifications importantes en matière d’incitatifs financiers pour les gestionnaires. La rémunération des dirigeants dans sa forme actuelle est en grande partie liée à la performance financière de l’entreprise et fluctue fortement selon le cours de l’action. Relier de façon significative la rémunération des dirigeants à certains objectifs ESG suppose des changements complexes qui susciteront de fortes résistances. En 2019, 67,2% des firmes du S&P/TSX 60 ont intégré au moins une mesure ESG dans leur programme de rémunération incitative. Toutefois, seulement 39,7% ont intégré au moins une mesure liée à l’environnement. Quelque 90% des firmes qui utilisent des mesures ESG le font dans le cadre de leur programme annuel de rémunération incitative mais pas dans les programmes de rémunération incitative à long terme. Ce fait est également observé aux États-Unis, alors qu’une étude récente de Willis Towers Watson démontrait que seulement 4% des firmes du S&P 500 utilisaient des mesures ESG dans des programmes à long terme.

5. N’est-il pas pertinent de soulever la question suivante : si l’entreprise doit être gérée selon le modèle des « parties prenantes », pourquoi seuls les actionnaires élisent-ils les membres du conseil d’administration? Cette question lancinante risque de hanter certains des promoteurs de ce modèle, car il ouvre la porte à l’entrée éventuelle d’autres parties prenantes au conseil d’administration, telles que les employés. Ce n’est peut-être pas ce que les fonds institutionnels avaient en tête lors de leur plaidoyer en faveur d’une conversion ESG.

Un vif débat fait rage (du moins dans les cercles académiques) sur les avantages et les inconvénients du modèle des parties prenantes. Dans le milieu des entreprises toutefois, la pression incessante des grands investisseurs a converti la plupart des directions d’entreprises à cette nouvelle religion ESG et parties prenantes même si plusieurs questions difficiles restent en suspens.

À la prochaine…

devoir de vigilance Gouvernance normes de droit parties prenantes Responsabilité sociale des entreprises

UE et devoir de vigilance

Ivan Tchotourian 26 octobre 2020 Ivan Tchotourian

Où s’en va l’UE avec le devoir de vigilance ? M. Farid Baddache propose une synthèse avec des pistes de réflexions : « L’UE veut un devoir de vigilance sur les droits humains obligatoire en 2021 » (Ksapas, 4 juin 2020).

Résumé :

Depuis plus de 10 ans, les entreprises appliquent les Principes Directeurs des Nations Unies sur les Entreprises et les Droits de l’Homme. Faisant écho à de multiples réglementations nationales – notamment en Californie, en France, au Royaume-Uni, aux Pays-Bas ou en Allemagne – la Commission Européenne a annoncé la mise en œuvre d’une directive sur la diligence raisonnable obligatoire en matière de Droits Humains en 2021. Quels sont les retours des entreprises à date ? Une directive européenne peut-elle imposer le respect des Droits Humains sur l’ensemble des chaînes d’approvisionnement, au-delà de ce qui existe déjà ? Quel impact la pandémie Covid-19 pourrait-elle avoir sur son éventuelle application ?

À la prochaine…

Gouvernance Nouvelles diverses parties prenantes Responsabilité sociale des entreprises

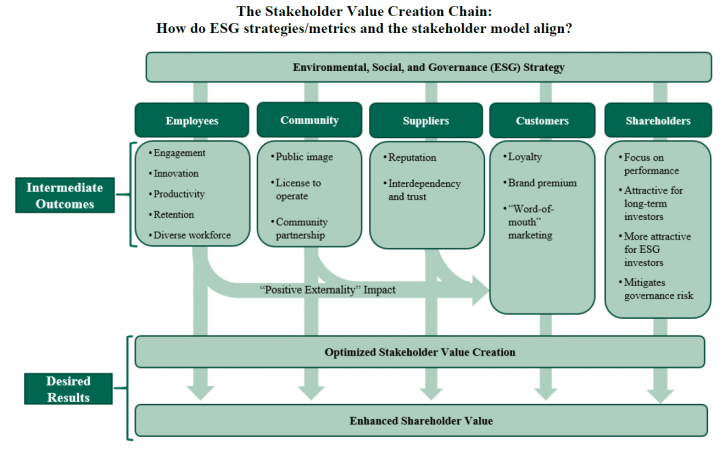

The Stakeholder Model and ESG

Ivan Tchotourian 17 septembre 2020 Ivan Tchotourian

Intéressant article sur l’Harvard Law School Forum on Corporate Governance consacré au modèle partie prenante et à ses liens avec les critères ESG : « The Stakeholder Model and ESG » (Ira Kay, Chris Brindisi et Blaine Martin, 14 septembre 2020).

Extrait :

Is your company ready to set or disclose ESG incentive goals?

ESG incentive metrics are like any other incentive metric: they should support and reinforce strategy rather than lead it. Companies considering ESG incentive metrics should align planning with the company’s social responsibility and environmental strategies, reporting, and goals. Another essential factor in determining readiness is the measurability/quantification of the specific ESG issue.

Companies will generally fall along a spectrum of readiness to consider adopting and disclosing ESG incentive metrics and goals:

- Companies Ready to Set Quantitative ESG Goals: Companies with robust environmental, sustainability, and/or social responsibility strategies including quantifiable metrics and goals (e.g., carbon reduction goals, net zero carbon emissions commitments, Diversity and Inclusion metrics, employee and environmental safety metrics, customer satisfaction, etc.).

- Companies Ready to Set Qualitative Goals: Companies with evolving formalized tracking and reporting but for which ESG matters have been identified as important factors to customers, employees, or other These companies likely already have plans or goals around ESG factors (e.g., LEED [Leadership in Energy and Environmental Design]-certified office space, Diversity and Inclusion initiatives, renewable power and emissions goals, etc.).

- Companies Developing an ESG Strategy: Some companies are at an early stage of developing overall ESG/stakeholder strategies. These companies may be best served to focus on developing a strategy for environmental and social impact before considering linking incentive pay to these priorities.

We note it is critically important that these ESG/stakeholder metrics and goals be chosen and set with rigor in the same manner as financial metrics to ensure that the attainment of the ESG goals will enhance stakeholder value and not serve simply as “window dressing” or “greenwashing.” [9] Implementing ESG metrics is a company-specific design process. For example, some companies may choose to implement qualitative ESG incentive goals even if they have rigorous ESG factor data and reporting.

Will ESG metrics and goals contribute to the company’s value-creation?

The business case for using ESG incentive metrics is to provide line-of-sight for the management team to drive the implementation of initiatives that create significant differentiated value for the company or align with current or emerging stakeholder expectations. Companies must first assess which metrics or initiatives will most benefit the company’s business and for which stakeholders. They must also develop challenging goals for these metrics to increase the likelihood of overall value creation. For example:

- Employees: Are employees and the competitive talent market driving the need for differentiated environmental or social initiatives? Will initiatives related to overall company sustainability (building sustainability, renewable energy use, net zero carbon emissions) contribute to the company being a “best in class” employer? Diversity and inclusion and pay equity initiatives have company and social benefits, such as ensuring fair and equitable opportunities to participate and thrive in the corporate system.

- Customers: Are customer preferences driving the need to differentiate on sustainable supply chains, social justice initiatives, and/or the product/company’s environmental footprint?

- Long-Term Sustainability: Are long-term macro environmental factors (carbon emissions, carbon intensity of product, etc.) critical to the Company’s ability to operate in the long term?

- Brand Image: Does a company want to be viewed by all constituencies, including those with no direct economic linkage, as a positive social and economic contributor to society?

There is no one-size-fits-all approach to ESG metrics, and companies fall across a spectrum of needs and drivers that affect the type of ESG factors that are relevant to short- and long-term business value depending on scale, industry, and stakeholder drivers. Most companies have addressed, or will need to address, how to implement ESG/stakeholder considerations in their operating strategy.

Conceptual Design Parameters for Structuring Incentive Goals

For those companies moving to implement stakeholder/ESG incentive goals for the first time, the design parameters range widely, which is not different than the design process for implementing any incentive metric. For these companies, considering the following questions can help move the prospect of an ESG incentive metric from an idea to a tangible goal with the potential to create value for the company:

- Quantitative goals versus qualitative milestones. The availability and quality of data from sustainability or social responsibility reports will generally determine whether a company can set a defined quantitative goal. For other companies, lack of available ESG data/goals or the company’s specific pay philosophy may mean ESG initiatives are best measured by setting annual milestones tailored to selected goals.

- Selecting metrics aligned with value creation. Unlike financial metrics, for which robust statistical analyses can help guide the metric selection process (e.g., financial correlation analysis), the link between ESG metrics and company value creation is more nuanced and significantly impacted by industry, operating model, customer and employee perceptions and preferences, etc. Given this, companies should generally apply a principles-based approach to assess the most appropriate metrics for the company as a whole (e.g., assessing significance to the organization, measurability, achievability, etc.) Appendix 1 provides a list of common ESG metrics with illustrative mapping to typical stakeholder impact.

- Determining employee participation. Generally, stakeholder/ESG-focused metrics would be implemented for officer/executive level roles, as this is the employee group that sets company-wide policy impacting the achievement of quantitative ESG goals or qualitative milestones. Alternatively, some companies may choose to implement firm-wide ESG incentive metrics to reinforce the positive employee engagement benefits of the company’s ESG strategy or to drive a whole-team approach to achieving goals.

- Determining the range of metric weightings for stakeholder/ESG goals. Historically, US companies with existing environmental, employee safety, and customer service goals as well as other stakeholder metrics have been concentrated in the extractive, industrial, and utility industries; metric weightings on these goals have ranged from 5% to 20% of annual incentive scorecards. We expect that this weighting range would continue to apply, with the remaining 80%+ of annual incentive weighting focused on financial metrics. Further, we expect that proxy advisors and shareholders may react adversely to non-financial metrics weighted more than 10% to 20% of annual incentive scorecards.

- Considering whether to implement stakeholder/ESG goals in annual versus long-term incentive plans. As noted above, most ESG incentive goals to date have been implemented as weighted metrics in balanced scorecard annual incentive plans for several reasons. However, we have observed increased discussion of whether some goals (particularly greenhouse gas emission goals) may be better suited to long-term incentives. [10] There is no right answer to this question—some milestone and quantitative goals are best set on an annual basis given emerging industry, technology, and company developments; other companies may have a robust long-term plan for which longer-term incentives are a better fit.

- Considering how to operationalize ESG metrics into long-term plans. For companies determining that sustainability or social responsibility goals fit best into the framework of a long-term incentive, those companies will need to consider which vehicles are best to incentivize achievement of strategically important ESG goals. While companies may choose to dedicate a portion of a 3-year performance share unit plan to an ESG metric (e.g., weighting a plan 40% relative total shareholder return [TSR], 40% revenue growth, and 20% greenhouse gas reduction), there may be concerns for shareholders and/or participants in diluting the financial and shareholder-value focus of these incentives. As an alternative, companies could grant performance restricted stock units, vesting at the end of a period of time (e.g., 3 or 4 years) contingent upon achievement of a long-term, rigorous ESG performance milestone. This approach would not “dilute” the percentage of relative TSR and financial-based long-term incentives, which will remain important to shareholders and proxy advisors.

Conclusion

As priorities of stakeholders continue to evolve, and addressing these becomes a strategic imperative, companies may look to include some stakeholder metrics in their compensation programs to emphasize these priorities. As companies and Compensation Committees discuss stakeholder and ESG-focused incentive metrics, each organization must consider its unique industry environment, business model, and cultural context. We interpret the BRT’s updated statement of business purpose as a more nuanced perspective on how to create value for all stakeholders, inclusive of shareholders. While optimizing profits will remain the business purpose of corporations, the BRT’s statement provides support for prioritizing the needs of all stakeholders in driving long-term, sustainable success for the business. For some companies, implementing incentive metrics aligned with this broader context can be an important tool to drive these efforts in both the short and long term. That said, appropriate timing, design, and communication will be critical to ensure effective implementation.

À la prochaine…