normes de droit

Gouvernance Normes d'encadrement normes de droit normes de marché Responsabilité sociale des entreprises

À signaler : Research Handbook on Environmental, Social and Corporate Governance

Ivan Tchotourian 3 juillet 2024

Edward Elgar vient de publier un ouvrage collectif Research Handbook on Environmental, Social and Corporate Governance dirigé par Thilo Kuntz.

The Research Handbook on Environmental, Social and Corporate Governance presents a comprehensive view of a rapidly evolving area of study. Adopting a comparative approach, it goes beyond issues of sustainability and human rights, covering the whole spectrum of ESG and its regulatory developments.

Voici la table des matières :

Introduction to Research Handbook on Environmental, Social and Corporate Governance 1

Thilo Kuntz

PART I DIRECTORS’ DUTIES AND MANAGERIAL DECISION-MAKING

1 Taking stakeholder interests seriously: A practitioner’s view from Germany on management duties 21

Christoph H. Seibt

2 ESG enhancements to company law: The French ‘PACTE’ law 44

Alain Pietrancosta

3 How ESG is weakening the business judgement rule 64

Thilo Kuntz

4 Human rights, environmental due diligence, and value chain responsibility: A view from France, Germany, and the European Union 91

Katrin Deckert

PART II INVESTOR AND SHAREHOLDER ACTIVISM

5 Stewardship codes, ESG activism and transnational ordering 112

Tim Bowley and Jennifer G. Hill

6 Climate proposals: ESG shareholder activism sidestepping board authority 132

Sofie Cools

7 ESG and workforce engagement: Experiences in the UK 151

Andrew Johnston and Navajyoti Samanta

8 ESG, the Alien Tort Statute, and private regulation’s legitimacy trap 171

Seth Davis

PART III INVESTMENT AND FUND REGULATION

9 EU ‘rule-based’ ESG duties for investment funds and their managers under the European ‘Green Deal’ 194

Sebastiaan Niels Hooghiemstra

10 Green bonds: A legal and economic analysis 217

Sergio Gilotta

11 Green public finance: The role of central banks 239

Jörn Axel Kämmerer

PART IV DISCLOSURE REGULATION AND RATINGS

12 The forces that shape mandatory ESG reporting 258

Thorsten Sellhorn and Victor Wagner

13 A green victory in the midst of potential defeat? Concern and optimism about the impact of the SEC’s climate-related disclosure rule 281

Lisa M. Fairfax

14 ESG ratings—guiding a movement in search for itself 303

Andreas Engert

PART V INTERNATIONAL LAW

15 ESG initiatives in international law 325

Rita Guerreiro Teixeira and Jan Wouters

16 ESG and international criminal liability 344

Cedric Ryngaert and Martine Jaarsma

PART VI REGIONAL DEVELOPMENTS

17 The EU Framework on ESG 362

Erik Lidman

18 The Nordic approach to corporate governance and ESG 381

Jesper Lau Hansen

19 ESG in China: A critical review from a legal perspective 404

Xianchu Zhang

20 ESG in Japan: The case of a mixed legal system 421

Masayuki Tamaruya and Mutsuhiko Yukioka

21 The legal and regulatory impetus towards ESG in India: Developments and challenges 443

Umakanth Varottil

À la prochaine…

Divulgation finance sociale et investissement responsable Gouvernance normes de droit Responsabilité sociale des entreprises Structures juridiques

Normes ESG: 2024 sera une année charnière

Ivan Tchotourian 22 novembre 2023 Ivan Tchotourian

Un beau numéro spécial dans le journal Les affaires.com : « Normes ESG: 2024 sera une année charnière » (novembre 2023).

Vous pouvez lire ci-dessous l’édito de Mme Marine Thomas (pour y accéder, cliquez ici) :

Bien sûr, la notion de bonnes pratiques environnementales, sociales et de gouvernance n’a rien de nouveau, ce sont des facteurs mesurés depuis une quinzaine d’années. La différence, c’est que jusque-là, tout le monde y allait à son gré dans la divulgation extrafinancière, les méthodes de calcul et les cadres de référence variant énormément. Les entreprises faisaient alors soit une évaluation de bonne foi, soit une «comptabilité créative» de leur bilan en matière de responsabilité sociale pour bien paraître.

Ça, c’était avant. L’harmonisation des normes du Conseil des normes internationales d’information sur la durabilité (ISSB) va mettre tout le monde au pas, du moins sur un pied d’égalité. Il sera désormais pas mal plus difficile de cacher une piètre performance en matière de développement durable.

Si vous pensez que vous avez le temps d’ici à ce que ce changement survienne, détrompez-vous. L’entrée en vigueur est dans deux mois et cela va créer une accélération considérable sur le marché.

Les grandes entreprises qui vont devoir exposer en plein jour les émissions de gaz à effet de serre qu’elles produisent sur l’ensemble de leur chaîne de valeur ne comptent pas porter ce fardeau seules. Elles vont se tourner vers celles qui les approvisionnent, généralement des PME, pour les aider à alléger leur propre bilan. La proportion de grands donneurs d’ordre avec des exigences ESG envers leurs fournisseurs devrait grimper à 92% d’ici 2024, nous révèle le rapport «L’ESG dans votre entreprise: un avantage pour décrocher de gros contrats» publié par la BDC au printemps. Un fait qui est encore largement sous le radar de PME et qui va leur tomber dessus comme un coup de massue le moment venu.

Pour les dirigeants qui pensent encore qu’agir en faveur des changements climatiques ne concerne que les woke, le réveil risque de faire mal. Qu’on se le dise: il ne s’agit plus d’une question de valeurs ou d’appartenance politique. Il s’agit ici d’affaires, tout simplement. Toutes les entreprises seront touchées, ne serait-ce que par leur financement.

Vous trouvez les taux d’intérêt élevés? Imaginez payer davantage, car votre entreprise n’est pas assez verte ou inclusive! En Europe, c’est déjà le cas. Ici, les institutions financières s’y préparent activement. Après tout, l’investissement, c’est avant tout de la gestion de risques, et les risques climatiques pèsent lourdement dans la pérennité de nombreuses entreprises. En outre, les banques auront elles aussi intérêt à montrer «patte verte» en prêtant à des entreprises ayant une plus faible empreinte pour leur propre bilan.

La bonne nouvelle, c’est qu’un nombre toujours plus important de PME prennent conscience des risques liés au climat et passent à l’action en faveur de la transition, comme nous le révèle le Baromètre de la transition des entreprises 2023 de Québec Net Positif, que nous vous offrons en exclusivité.

Pour ces PME, les changements à venir peuvent présenter de sérieux atouts. La recherche d’un approvisionnement durable et d’une réduction des distances de transport va signifier un nouvel intérêt pour des entreprises locales ayant su se positionner. Toute longueur d’avance prise maintenant sera difficile à rattraper par la concurrence qui n’aura pas su se transformer à temps.

Même si tous ces acronymes — ESG, RSE, GES, EDI… — peuvent donner le tournis, vous n’avez plus le choix de les connaître, et surtout d’en tenir compte. Alors que les entreprises commencent les budgets et la planification de 2024, elles ont tout intérêt, si ce n’est pas déjà fait, à mettre la préparation d’un plan en matière de développement durable tout en haut de leur liste de leurs priorités.

Tenez-le-vous pour dit: prêts, pas prêts, les nouvelles normes ESG arrivent et elles vont tout bouleverser!

À la prochaine…

Gouvernance normes de droit Nouvelles diverses Responsabilité sociale des entreprises

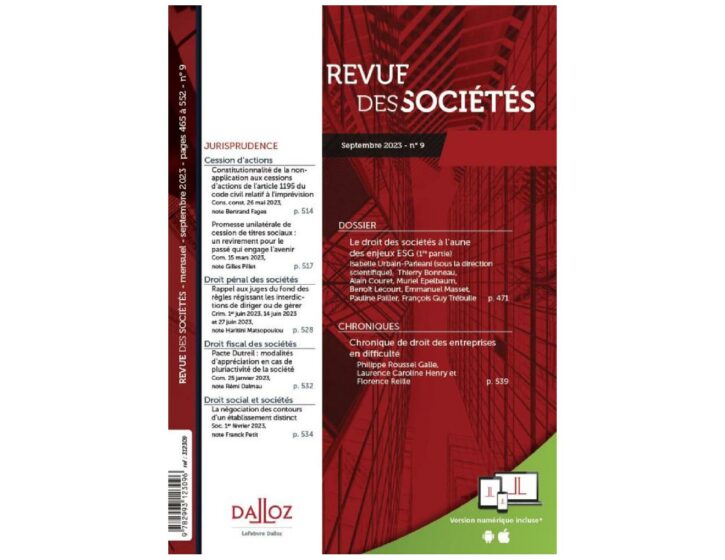

Numéro spécial de la revue Droit des sociétés sur les critères ESG

Ivan Tchotourian 26 octobre 2023 Ivan Tchotourian

La prestigieuse Revue des sociétés (Dalloz) publie deux numéros spéciaux (septembre et octobre) sur les liens entre droit des sociétés et critères ESG. De beaux articles à découvrir !

À la prochaine…

Base documentaire finance sociale et investissement responsable loi et réglementation normes de droit Responsabilité sociale des entreprises

Fonds d’investissement et ESG : cela bouge au Canada

Ivan Tchotourian 4 avril 2022 Ivan Tchotourian

Le 19 janvier 2022, les ACVM ont publié l’Avis 81-334 du personnel des ACVM Information des fonds d’investissement au sujet des facteurs environnementaux, sociaux et de gouvernance.

Au-delà des information contenues dans cet avis sur la prise en compte des critères ESG dans le domaine des fonds d’investissement, les ACVM fournissent de précieuses indications :

Pour donner suite aux constatations des examens de l’information continue axés sur les facteurs ESG, à ses observations sur les changements aux fonds existants en lien avec ces facteurs ainsi qu’aux recommandations de l’OICV, le personnel a décidé de fournir des indications sur l’application des obligations prévues par la réglementation en valeurs mobilières aux fonds d’investissement en ce qui a trait aux facteurs ESG, surtout aux fonds relatifs aux ESG, au regard des aspects suivants : i) les objectifs de placement et les noms des fonds; ii) les types de fonds; iii) l’information sur les stratégies de placement; iv) les politiques et procédures en matière de vote par procuration et d’engagement actionnarial; v) l’information sur les risques; vi) la convenance des placements; vii) l’information continue; viii) les communications publicitaires; ix) les changements aux fonds existants en lien avec les facteurs ESG; et x) la terminologie relative aux facteurs ESG.

À la prochaine…

actualités internationales Divulgation divulgation extra-financière Gouvernance Normes d'encadrement normes de droit normes de marché Responsabilité sociale des entreprises

Approche juridique sur la transparence ESG

Ivan Tchotourian 3 août 2020 Ivan Tchotourian

Excellente lecture ce matin de ce billet du Harvard Law School Forum on Corporate Governance : « Legal Liability for ESG Disclosures » (de Connor Kuratek, Joseph A. Hall et Betty M. Huber, 3 août 2020). Dans cette publication, vous trouverez non seulement une belle synthèse des référentiels actuels, mais aussi une réflexion sur les conséquences attachées à la mauvaise divulgation d »information.

Extrait :

3. Legal Liability Considerations

Notwithstanding the SEC’s position that it will not—at this time—mandate additional climate or ESG disclosure, companies must still be mindful of the potential legal risks and litigation costs that may be associated with making these disclosures voluntarily. Although the federal securities laws generally do not require the disclosure of ESG data except in limited instances, potential liability may arise from making ESG-related disclosures that are materially misleading or false. In addition, the anti-fraud provisions of the federal securities laws apply not only to SEC filings, but also extend to less formal communications such as citizenship reports, press releases and websites. Lastly, in addition to potential liability stemming from federal securities laws, potential liability could arise from other statutes and regulations, such as federal and state consumer protection laws.

A. Federal Securities Laws

When they arise, claims relating to a company’s ESG disclosure are generally brought under Section 11 of the Securities Act of 1933, which covers material misstatements and omissions in securities offering documents, and under Section 10(b) of the Securities Exchange Act of 1934 and rule 10b-5, the principal anti-fraud provisions. To date, claims brought under these two provisions have been largely unsuccessful. Cases that have survived the motion to dismiss include statements relating to cybersecurity (which many commentators view as falling under the “S” or “G” of ESG), an oil company’s safety measures, mine safety and internal financial integrity controls found in the company’s sustainability report, website, SEC filings and/or investor presentations.

Interestingly, courts have also found in favor of plaintiffs alleging rule 10b-5 violations for statements made in a company’s code of conduct. Complaints, many of which have been brought in the United States District Court for the Southern District of New York, have included allegations that a company’s code of conduct falsely represented company standards or that public comments made by the company about the code misleadingly publicized the quality of ethical controls. In some circumstances, courts found that statements about or within such codes were more than merely aspirational and did not constitute inactionable puffery, including when viewed in context rather than in isolation. In late March 2020, for example, a company settled a securities class action for $240 million alleging that statements in its code of conduct and code of ethics were false or misleading. The facts of this case were unusual, but it is likely that securities plaintiffs will seek to leverage rulings from the court in that class action to pursue other cases involving code of conducts or ethics. It remains to be seen whether any of these code of conduct case holdings may in the future be extended to apply to cases alleging 10b-5 violations for statements made in a company’s ESG reports.

B. State Consumer Protection Laws

Claims under U.S. state consumer protection laws have been of limited success. Nevertheless, many cases have been appealed which has resulted in additional litigation costs in circumstances where these costs were already significant even when not appealed. Recent claims that were appealed, even if ultimately failed, and which survived the motion to dismiss stage, include claims brought under California’s consumer protection laws alleging that human right commitments on a company website imposed on such company a duty to disclose on its labels that it or its supply chain could be employing child and/or forced labor. Cases have also been dismissed for lack of causal connection between alleged violation and economic injury including a claim under California, Florida and Texas consumer protection statutes alleging that the operator of several theme parks failed to disclose material facts about its treatment of orcas. The case was appealed to the U.S. Court of Appeals for the Ninth Circuit, but was dismissed for failure to show a causal connection between the alleged violation and the plaintiffs’ economic injury.

Overall, successful litigation relating to ESG disclosures is still very much a rare occurrence. However, this does not mean that companies are therefore insulated from litigation risk. Although perhaps not ultimately successful, merely having a claim initiated against a company can have serious reputational damage and may cause a company to incur significant litigation and public relations costs. The next section outlines three key takeaways and related best practices aimed to reduce such risks.

C. Practical Recommendations

Although the above makes clear that ESG litigation to date is often unsuccessful, companies should still be wary of the significant impacts of such litigation. The following outlines some key takeaways and best practices for companies seeking to continue ESG disclosure while simultaneously limiting litigation risk.

Key Takeaway 1: Disclaimers are Critical

As more and more companies publish reports on ESG performance, like disclaimers on forward-looking statements in SEC filings, companies are beginning to include disclaimers in their ESG reports, which disclaimers may or may not provide protection against potential litigation risks. In many cases, the language found in ESG reports will mirror language in SEC filings, though some companies have begun to tailor them specifically to the content of their ESG reports.

From our limited survey of companies across four industries that receive significant pressure to publish such reports—Banking, Chemicals, Oil & Gas and Utilities & Power—the following preliminary conclusions were drawn:

- All companies surveyed across all sectors have some type of “forward-looking statement” disclaimer in their SEC filings; however, these were generic disclaimers that were not tailored to ESG-specific facts and topics or relating to items discussed in their ESG reports.

- Most companies had some sort of disclaimer in their Sustainability Report, although some were lacking one altogether. Very few companies had disclaimers that were tailored to the specific facts and topics discussed in their ESG reports:

- In the Oil & Gas industry, one company surveyed had a tailored ESG disclaimer in its ESG Report; all others had either the same disclaimer as in SEC filings or a shortened version that was generally very broad.

- In the Banking industry, two companies lacked disclaimers altogether, but the rest had either their SEC disclaimer or a shortened version.

- In the Utilities & Power industry, one company had no disclaimer, but the rest had general disclaimers.

- In the Chemicals industry, three companies had no disclaimer in their reports, but the rest had shortened general disclaimers.

- There seems to be a disconnect between the disclaimers being used in SEC filings and those found in ESG In particular, ESG disclaimers are generally shorter and will often reference more detailed disclaimers found in SEC filings.

Best Practices: When drafting ESG disclaimers, companies should:

- Draft ESG disclaimers carefully. ESG disclaimers should be drafted in a way that explicitly covers ESG data so as to reduce the risk of litigation.

- State that ESG data is non-GAAP. ESG data is usually non-GAAP and non-audited; this should be made clear in any ESG Disclaimer.

- Have consistent disclaimers. Although disclaimers in SEC filings appear to be more detailed, disclaimers across all company documents that reference ESG data should specifically address these issues. As more companies start incorporating ESG into their proxies and other SEC filings, it is important that all language follows through.

Key Takeaway 2: ESG Reporting Can Pose Risks to a Company

This article highlighted the clear risks associated with inattentive ESG disclosure: potential litigation; bad publicity; and significant costs, among other things.

Best Practices: Companies should ensure statements in ESG reports are supported by fact or data and should limit overly aspirational statements. Representations made in ESG Reports may become actionable, so companies should disclose only what is accurate and relevant to the company.

Striking the right balance may be difficult; many companies will under-disclose, while others may over-disclose. Companies should therefore only disclose what is accurate and relevant to the company. The US Chamber of Commerce, in their ESG Reporting Best Practices, suggests things in a similar vein: do not include ESG metrics into SEC filings; only disclose what is useful to the intended audience and ensure that ESG reports are subject to a “rigorous internal review process to ensure accuracy and completeness.”

Key Takeaway 3: ESG Reporting Can Also be Beneficial for Companies

The threat of potential litigation should not dissuade companies from disclosing sustainability frameworks and metrics. Not only are companies facing investor pressure to disclose ESG metrics, but such disclosure may also incentivize companies to improve internal risk management policies, internal and external decisional-making capabilities and may increase legal and protection when there is a duty to disclose. Moreover, as ESG investing becomes increasingly popular, it is important for companies to be aware that robust ESG reporting, which in turn may lead to stronger ESG ratings, can be useful in attracting potential investors.

Best Practices: Companies should try to understand key ESG rating and reporting methodologies and how they match their company profile.

The growing interest in ESG metrics has meant that the number of ESG raters has grown exponentially, making it difficult for many companies to understand how each “rater” calculates a company’s ESG score. Resources such as the Better Alignment Project run by the Corporate Reporting Dialogue, strive to better align corporate reporting requirements and can give companies an idea of how frameworks such as CDP, CDSB, GRI and SASB overlap. By understanding the current ESG market raters and methodologies, companies will be able to better align their ESG disclosures with them. The U.S. Chamber of Commerce report noted above also suggests that companies should “engage with their peers and investors to shape ESG disclosure frameworks and standards that are fit for their purpose.”

À la prochaine…

finance sociale et investissement responsable normes de droit

Inquiétant pour l’investissement responsable ?

Ivan Tchotourian 8 juillet 2020 Ivan Tchotourian

Le Ministère du travail américain soumet à commentaire une proposition inquiétante pour l’investissement responsable. Cette proposition est détaillée dans l’Harvard Law School Forum on Corporate Governance : « DOL Proposes New Rules Regulating ESG Investments » (7 juillet 2020).

Extrait :

The Department of Labor (“DOL”) has proposed for public comment rules that would further burden the ability of fiduciaries of private-sector retirement plans to select investments based on ESG factors and would bar 401(k) plans from using a fund with any ESG mandate as the default investment alternative for non-electing participants.

The proposed rules would prohibit a retirement plan fiduciary from making any investment, or choosing an investment fund, based on the consideration of an environmental, societal or governmental factor unless that factor independently represents a material economic investment consideration under generally accepted investment theories or serves as a tiebreaker in what the DOL characterizes as the rare case of economically equivalent investments. In order to select an investment with an ESG component, the plan fiduciaries would be required to compare investments or strategies on “pecuniary” factors such as diversification, liquidity and rate of return. Specific documentation would be required for the tiebreaker justification and for the selection and monitoring of an investment alternative in a 401(k) plan that includes ESG in its mandate or fund name. Most significantly, the proposed rules would prohibit a 401(k) plan from providing a qualified default investment alternative (“QDIA”) with an ESG component, no matter how small, even if that investment alternative satisfies the pecuniary factor requirements.

À la prochaine…