La prestigieuse Revue des sociétés (Dalloz) publie deux numéros spéciaux (septembre et octobre) sur les liens entre droit des sociétés et critères ESG. De beaux articles à découvrir !

Nouvelle qui intéressera nos lectrices et lecteurs du blogue : « Cyprus passes Social Enterprise Law » (par Alexandra Fougala-Metaxa, Pioneer Post, 30 mars 2021).

Extrait :

Social enterprises in Cyprus now have their own legal framework. In December 2020, the House of Representatives of Cyprus passed, for the first time, a Social Enterprise Law. The bill was initially introduced in 2013 and it has taken seven years for it to be approved, reportedly due to many modifications, debates and delays.

Prior to this, Cyprus had no legal framework for social enterprises. According to a social enterprise mapping report for Cyprus, carried out by the European Commission, there were only seven organisations that could be described as ‘social enterprises’ in Cyprus in 2014. A recent survey by CyprusInno of entrepreneurs in the Greek Cypriot and Turkish Cypriot communities found that 11% of the 359 entrepreneurs surveyed said they ran social enterprises.

Maria Nomikou, the youth, skills and inclusive communities sector lead for Europe at the British Council, says: “A law on social enterprises can have a very positive impact as it fosters visibility, growth and the development of this type of business.”

Visibility surrounding social enterprises is key to encouraging the growth of the sector in Cyprus. For years, the lack of a legal definition of the term social enterprise meant that social enterprises in Cyprus operated as either limited liability companies or charities. The problem with this, as identified by Andrea Solomonides, the lead of Cyprus operations at enterprise support organisation Cypriot Enterprise Link, was it created an image problem – many people did not think that working full time for social enterprises was financially sustainable, and thus the sector struggled to attract staff.

A law defining social enterprises as separate, unique entities, distinct from other types of businesses or non-profits, helps increase awareness. The law also means that social enterprises will have access to EU grants available only to the social enterprise sector, and receive various tax benefits, which, Maria Nomikou hopes, will motivate people to set up their own social enterprises.

(…) The definition of social enterprises under the new law is as enterprises with a social cause that reinvest a proportion of their profits back into their work, or enterprises that hire a certain proportion of their staff from vulnerable groups.

L’entreprise sud-coréenne Samsung, spécialisée dans l’électronique, a été contrainte de se défendre, jeudi 11 janvier, après que deux ONG avaient apporté de nouveaux éléments à leurs accusations de violations des droits de l’homme dans les usines chinoises du constructeur (ici). Le Monde nous apprend que les poursuites judiciaires n’auront pas lieu : « Conditions de travail des ouvriers chinois : les poursuites contre Samsung France annulées » (26 avril 2021).

Extrait :

La filiale du leader mondial des smartphones avait en effet été mise en examen en avril 2019 pour « pratiques commerciales trompeuses », du fait de la présence sur son site Internet de son opposition au travail forcé et au travail des enfants.

(…) Selon une source judiciaire, cette plainte a été jugée irrecevable le 30 mars par la chambre de l’instruction de la cour d’appel de Paris, au motif que les ONG ne disposaient pas de l’agrément pour agir en justice contre des « pratiques commerciales trompeuses ».

Cette décision entraîne de fait la nullité de la procédure qu’elles avaient lancée, et a donc pour conséquence d’annuler la mise en examen de Samsung France. La maison mère, Samsung Electronics, a dit « prendre acte » de ces décisions, sans plus de commentaires.

(…)

Afin de justifier une procédure pénale en France, les ONG estimaient suffisant que le message incriminé soit accessible aux consommateurs français pour que les juridictions du pays soient compétentes. S’appuyant sur divers rapports d’ONG qui ont pu se rendre dans les usines du groupe en Chine, en Corée du Sud et au Vietnam, Sherpa et Actionaid dénonçaient l’« emploi d’enfants de moins de seize ans », des « horaires de travail abusifs », des « conditions de travail et d’hébergement incompatibles avec la dignité humaine » et une « mise en danger des travailleurs ».

Une autre association, UFC-Que choisir, a déposé elle aussi en février à Paris une plainte avec constitution de partie civile pour pratiques commerciales trompeuses visant le groupe, et attend désormais que la justice se prononce.

A notable driver in the movement towards stronger oversight has been allegations of abuses committed in the extractive sector. Indeed, The Business & Human Rights Resource Centre’s latest Transition Minerals Tracker (May 2020) features Glencore as a top 5 company in respect of 4 out of 6 transitional commodities (cobalt, copper, nickel and zinc) and records allegations of human rights abuses in three of these categories: cobalt (10 allegations[2]); copper (32) and zinc (14). While the copper and zinc allegations against Glencore are roughly double in number to those of its nearest competitor, it ties with the DRC state mining company, Gécamines, in respect of cobalt related human rights allegations. In unrelated news, Glencore fought unsuccessfully last week to obtain a gagging injunction pertaining to allegations of child labour made against it by the organization Initiatives multinationales responsableswith reference to its Bolivian mine in Porco.

On November 29, 2020, 50.7% of the national vote went in favour of the RBI; however, it gained a majority vote in only a third of the Swiss cantons. Observers have pointed out that this is the first time in 50 years for a referendum measure to flounder due to regional restrictions despite having attracted a nationwide popular majority.

The outcome of the referendum is thus that the Swiss Responsible Business Initiative will not come into being. However, the fact that it carried the popular vote has been described as, “a clear sign to Switzerland’s multinationals that the days of avoiding scrutiny are well and truly over.”

This is in line with developments elsewhere in the world.

In Vedanta Resources Plc & Anor v Lungowe & Ors the UK Supreme Court held in 2019 in a procedural ruling that pollution charges could proceed in the UK against Vedanta Resources, plc (“Vedenta”) and its Zambian subsidiary, Konkola Copper Mines, plc (“KCM”), notwithstanding the fact that the pollution was alleged to have taken place in Zambia and that the claimants were a Zambian community. The facts relate to the operations of the Nchanga Copper Mine in the Chingola District of Zambia.

This full-bench decision is interesting for multiple reasons. First, it is a significant ruling for multinational UK parent companies with subsidiaries operating in developing countries. Second, both Vedanta and KCM had explicitly submitted to the jurisdiction of the Zambian courts. Third, although most of the proper place indicators pointed to Zambia and despite the fact that the Court found that there would be a real risk of irreconcilable judgments between Zambia and the UK, it still ruled that the UK had jurisdiction to hear the case on the basis that the claimants were likely to suffer a substantial injustice if the matter were to proceed in Zambia. Interestingly, no criticism was levied against either the administration of justice in Zambia or its legal system. Instead, the Court held that by reason of their extreme poverty the claimants would not be able to afford funding the litigation in Zambia and that they would not be able to access a Zambian legal team of sufficient expertise, experience and resources to pursue such litigation in Zambia. In other words, it became an issue where access to justice considerations trumped strict procedure.

All of this is relevant in the Canadian context. In a recent Blog I addressed the settlement of the litigation in Nevsun v Araya. Of great importance remains the fact that in February 2020 the Supreme Court of Canada has in this litigation categorically opened the way for foreign plaintiffs to bring allegations in Canadian courts of human rights abuses perpetrated by foreign subsidiaries of Canadian mining companies. While the Supreme Court made no ruling on the substance of the charges given the preliminary nature of the proceedings, future plaintiffs certainly will get to address the substance of their claim far sooner. As this note has illustrated, Canada is in step with leading business and human rights developments on the international front. That is cause for celebration.

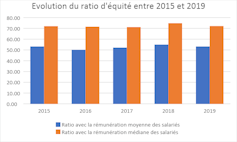

Bel article de Vanessa Serret et Mohamed Khemissi dans The conversation (27 juillet 2020) : « Rémunération des dirigeants : la transparence ne fait pas tout ». Cet article revient sur le ratio d’équité : non seulement son utilité, mais encore son niveau (20 ? 100 ?…)

Le ratio d’équité apprécie l’écart entre la rémunération de chaque dirigeant et le salaire (moyen et médian) des salariés à temps plein de son entreprise. Il est prévu un suivi de l’évolution de ce ratio au cours des cinq derniers exercices et sa mise en perspective avec la performance financière de la société. Ces comparaisons renseignent sur la dynamique du partage de la création de valeur entre le dirigeant et les salariés.

(…)

Un premier état des lieux

Sur la base des rémunérations versées en 2019 par les entreprises composant l’indice boursier du CAC 40, les patrons français ont perçu un salaire moyen de 5 millions d’euros, soit une baisse de 9,1 % par rapport à 2018.

Évolution du ratio d’équité par rapport à la rémunération moyenne (bleu) et médiane (orange) des salariés de 2015 à 2019. auteurs

Ce chiffre représente 53 fois la rémunération moyenne de leurs employés (72 fois la rémunération médiane) : un ratio acceptable, selon l’agence de conseil en vote Proxinvest. En effet, selon cette agence, et afin de garantir la cohésion sociale au sein de l’entreprise, le ratio d’équité ne doit pas dépasser 100 (par rapport à la rémunération moyenne des salariés).

Deux dirigeants s’attribuent néanmoins des rémunérations qui dépassent le maximum socialement tolérable à savoir Bernard Charlès, vice-président du conseil d’administration et directeur général de Dassault Systèmes et Paul Hudson, directeur général de Sanofi avec un ratio d’équité qui s’établit respectivement de 268 et de 107.

Notons également que pour les deux sociétés publiques appartenant à l’indice boursier du CAC 40, le ratio d’équité dépasse le plafond de 20 (35 pour Engie et 38 pour Orange) fixé par le décret n° 2012-915 du 26 juillet 2012, relatif au contrôle de l’État sur les rémunérations des dirigeants d’entreprises publiques.

Le 2 août 2020, Christiaan de Brauw a publié un intéressant billet sur l’Harvard Law School Forum on Corporate Governance sous le titre « The Dutch Stakeholder Experience ».

Extrait :

Lessons learned

The Dutch experience shows that the following lessons are key to make the stakeholder-oriented governance model work in practice.

Embed a clear stakeholder mission in the fiduciary duties of the board

To have a real stakeholder model, the board must have a duty to act in the interests of the business and all the stakeholders, not only the shareholders. In shareholder models there may be some room to consider stakeholder interests. For example, in Delaware and various other US states, the interests of stakeholders other than shareholders may be considered in the context of achieving overall long-term shareholder value creation. In US states with constituency statutes, the board’s discretion is preserved: the interests of stakeholders other than shareholders can be, but do not have to be, taken into account. A meaningful stakeholder model requires the board to act in the interests of the business and all stakeholders. This is a “shall” duty, in the words of Leo Strine and Robert Eccles (see Purpose With Meaning: A Practical Way Forward, Robert G. Eccles, Leo E. Strine and Timothy Youmans, May 16, 2020). Rather than allowing for the possibility that all stakeholders’ interests will be taken into account; it should create a real duty to do so. Since 1971, boards of Dutch companies have had such a “shall” duty to follow a stakeholder mission, similar to that of a benefit corporation in, for example, Delaware.

The stakeholder duty must be clear and realistic for boards in the economic environment in which they operate. To define the contours of such a mission in a clear and practical way is not easy, as the journey of the Dutch stakeholder model shows. Today, the Netherlands has a meaningful and realistically defined fiduciary duty for boards. The primary duty is to promote the sustainable success of the business, focused on long-term value creation, while taking into account the interests of all stakeholders and ESG and similar sustainability perspectives. These principles are broadly similar to the corporate purpose and mission proposed by Martin Lipton and others (see On the Purpose of the Corporation, Martin Lipton, William Savitt and Karessa L. Cain, posted May 27, 2020).

Critics of the stakeholder model sometimes point to the ambiguity and lack of clarity of such a pluralistic model. The developments of the Dutch stakeholder model since its inception show that a pluralistic model can work in practice. By now, Dutch boards’ overriding task is adequately clear and aligned with what is typically expected of a company’s executives: pursuing the strategic direction that will most likely result in long-term and sustainable business success. The Dutch stakeholder model also has a workable roadmap to deal with stakeholders’ interests, particularly if they diverge or cannot all be protected fully at the same time, which necessarily results in trade-offs between stakeholders. A realistic approach to governance acknowledges that a stakeholder model does not mean that boards can or should seek to maximize value for all the stakeholders equally and at the same time. It is simply unrealistic to simultaneously pay (and progressively increase) dividends, increase wages and improve contract terms, while also promoting the success of the business. The Dutch interpretation of the stakeholder model, as developed through practice over decades, boils down to the focus on the sustainable success of the business and long-term value creation. As said above, stakeholders are protected by the board’s duty to prevent disproportionate or unnecessary harm to any class of stakeholders. Boards should avoid or mitigate such harm, for example, by agreeing “non-financial covenants” in a takeover. This makes sense as a way to protect stakeholder interests in a realistic manner, much more so than merely requiring boards—without any further guidance—to create value for all the stakeholders.

A stakeholder-oriented model should also be modern and flexible enough to address and incorporate important developments. The Dutch model is especially well positioned to embrace ESG and similar sustainability perspectives. For example, the Dutch company DSM has successfully illustrated this, while being profitable and attractive for investors. There is growing appreciation that being a frontrunner in ESG is required for sustainable business success. In addition to the fact that ESG is required for continuity of the business model and can often give a company a competitive edge, stakeholders increasingly require it. Simply “doing the right thing”, as an independent corporate goal, is more and more seen as important by (new millennial) employees, customers, institutional investors and other stakeholders.

There is no standard test to determine whether a business has achieved sustainable success. There will be different ways to achieve and measure success for different companies, depending on the respective circumstances. Therefore, the test will always have to be bespoke, implemented by the board and explained to stakeholders.

The Dutch stakeholder model has proven to work quite well in times of crisis, such as today’s Covid-19 crisis, as it bolsters the board’s focus on the survival and continuity of the business. The board must first assess whether there is a realistic chance of survival and continuity of the business. If not, and if insolvency becomes imminent, the board’s duties transform to focus on creditors’ interests, such as preventing wrongful trading and the winding down or restarting of the business in line with applicable insolvency/restructuring proceedings. Driven by the economic reality and the need to survive, in times of crisis, boards typically have more freedom to do what it takes to survive: from pursuing liquidity enhancing measures, implementing reorganizations, suspending dividends to shareholders and payments to creditors and so on. The success of the business remains the overriding aim, and in some cases harm to one or more classes of stakeholders may need to be accepted. In addition, in a true stakeholder model, in times of crisis there may not be sympathy for corporate raiders or activists (so-called “corona profiteers” in the current case) who want to buy listed companies on the cheap. A just say not now defense in addition to the just say no defense will readily be available for boards who are occupied with dealing with the crisis and revaluating the best strategic direction. This idea that during the Covid-crisis protection against activists and hostile bidders may be needed seems to be understood as well by, for example, ISS and Glass Lewis, evidenced by their willingness to accept new poison pills for a one year duration (see, for example, ISS and Glass Lewis Guidances on Poison Pills during COVID-19 Pandemic, Paul J. Shim, James E. Langston, and Charles W. Allen, posted on April 26, 2020).

Teeth to protect the stakeholder mission and appropriate checks and balances

The Netherlands has adopted a model in which matters of strategy are the prerogative of the executive directors under supervision of the non-executive directors or, in the still widely used two-tier system, of the management board under supervision of the supervisory board. Similar to the discretion afforded to directors under Delaware’s business judgment rule, a Dutch board has a lot of freedom to choose the strategic direction of the company. In a dispute, the amount of care taken by the board in the decision-making process will be scrutinized by courts, but normally objectively reasonable decisions will be respected. In the Dutch model the board is the captain of the ship; it is best equipped to determine the course for the business and take difficult decisions on how to serve the interests of stakeholders. Generally, the board has no obligation to consult with, or get the approval of, the shareholders in advance of a decision.

At the same time, in recognition of the significant power that boards have in the Dutch stakeholder model, there should be checks and balances to ensure the board’s powers are exercised in a careful manner, without conflicts of interest and without entrenchment. Non-executive/supervisory directors will need to exercise critical and hands-on oversight, particularly when there are potential conflicts of interest. Further, shareholders and other stakeholders are entitled to hold boards to account: boards need to be able to explain their strategic decisions. Shareholders can use their shareholder rights to express their opinions and preferences. Shareholders can also pursue the dismissal of failing and entrenched boards. Boards need regular renewed shareholder mandates through reappointments. The courts are the ultimate guardian of the stakeholder model. The Dutch Enterprise Chamber at the Amsterdam Court of Appeals, which operates in a comparable manner to the Delaware Chancery Court, is an efficient and expert referee of last resort.

The stakeholder model should not convert to a shareholder model in takeover scenarios. The board should focus on whether a takeover is the best strategic option and take into account the consequences for all the stakeholders. In most cases, the best strategic direction for the business will create the highest valuation of the business. But, and this is a real difference with shareholder models, it should be acknowledged that the stand-alone (or other best strategic) option can be different from the strategic option favored by a majority of the shareholders and the option that creates the most shareholder value. This principle was confirmed by the Dutch Enterprise Chamber in 2017 in the AkzoNobel case.

A meaningful stakeholder model requires teeth. The right governance structures need to be put in place to create and protect the long-term stakeholder mission in the face of short-term market pressure. The reality—in the Netherlands as well as in the US—is that shareholders are the most powerful constituency in the stakeholder universe, with the authority to replace the board. In Dutch practice, various countervailing measures can be used to protect the stakeholder mission. A commonly used instrument is the independent protection foundation, the Dutch poison pill. The independent foundation can exercise a call option and acquire and vote on preference shares. It can neutralize the newly acquired voting power of hostile bidders or activists and is effective against actions geared at replacing the board, including a proxy fight. Once the threat no longer exists, the preference shares are cancelled. These measures have been effective, for example, against hostile approaches of America Movil for KPN (2013) and Teva for Mylan (2015).

Foster a stakeholder mindset, governance and environment

Perhaps the most important prerequisite for a well-functioning stakeholder model is the actual mindset of executives and directors. This mindset drives how they will use their stakeholder powers. Fiduciary duties—also in a stakeholder model—are “open norms” and leave a lot of freedom to boards to pursue the strategic direction and to use their authority as they deem fit. The prevailing spirit and opinions about governance are important, as they influence how powers are interpreted and exercised. As an example, the Dutch requirement that boards need to act in the interest of the company and its business dates from 1971, but that did not prevent boards in the 2000s from seeing shareholders as the first among equals. Today, the body of ideas about governance in the developed world is tending to converge towards stakeholder-oriented governance. This seems to indicate a fundamental change in mindset, not merely a fashionable trend or lip service. Board members with a stakeholder conviction should not be afraid to follow their mission, even if it runs counter to past experience or faces shareholder opposition. Of course, the future will hold the ultimate test for the stakeholder model. Can it, in practice, deliver on its promise to create sustainable success and long-term value and provide better protection for stakeholders? If so, this will create a positive feedback loop in which more boards embrace it.

Stakeholder-based governance models remain works in progress. In order to succeed in the long term, models that grant boards the authority to determine the strategy need to stay viable and attractive for shareholders. Going forward, boards following a stakeholder-based model will likely need to focus more on accountability, for example by concretely substantiating their strategic plans and goals and, where possible, providing the relevant metrics to measure their achievements. In reality, stakeholder models are already attractive for foreign investors: about 90% of investors in Dutch listed companies are US or UK investors. In addition, developments in the definition of the corporate purpose will further refine the stakeholder model. In the Netherlands, there has been a call to action by 25 corporate law professors who argue that companies should act as responsible corporate citizens and should articulate a clear corporate purpose.

To make stakeholder governance work, ideally, all stakeholders are committed to the same mission. It is encouraging that key institutional investors are embracing long-term value creation and the consideration of other stakeholders’ interests, for instance by supporting the New Paradigm model of corporate governance and stewardship codes to that effect. However, the “proof of the pudding” is whether boards can continue to walk the stakeholder talk and pursue the long-term view in the face of short-term pressure, either through generally accepted goals and behavior or, if necessary, countervailing governance arrangements. Today, it is still far from certain whether institutional investors will reject pursuing a short-term takeover premium, even where they consider the offer to be undervalued or not supportive of long-term value creation. Annual bonuses of the deciding fund manager may depend on accepting that offer. Until the behavior of investors in such scenarios respects the principle of long-term value creation, appropriate governance protection is important to prevent a legal pathway for shareholders to impose their short-term goals. Therefore, even in jurisdictions where stakeholder-based approaches have been embraced, and are actually pursued by boards, governance arrangements might need to be changed to make the stakeholder mission work in practice. Clear guidance for boards is needed on what the stakeholder mission is and how to deal with stakeholders’ interests, as well as catering for adequate powers and protection for boards.

The Dutch model, which requires a company to be business success-driven, have a “shall duty” to stakeholders that applies even in a sale of the company, and that recognizes that corporations are dependent on stakeholders for success and have a corresponding responsibility to stakeholders, has been demonstrated to be consistent with a high-functioning economy. By highlighting the Dutch system, however, I do not mean to claim that it is unique. For policymakers who are considering the merits of a stakeholder-based governance model, the Dutch system should be seen as one example among many corporate governance systems in successful market economies (such as Germany) that embrace this form of stakeholder-based governance. There is likely no one-size-fits-all approach; each jurisdiction should find the tailor-made model that works best for it, like perhaps the introduction of the corporate purpose in the UK and France. In any event, there is a great benefit in exchanging ideas and learning from experiences in different jurisdictions to find common ground and best practices in order to increase the acceptance and appreciation of stakeholder-oriented governance models.

US governance practices have been, and are, influential around the world. In the 2000s the pendulum in developed countries, including to some extent in the Netherlands, clearly swung in the direction of shareholder-centric governance as championed in the US. In the current environment, if the US system’s focus on shareholders is not adjusted to protect stakeholder interests, it may over time perhaps become an outlier among many of the world’s leading market economies that in one way or the other have adopted a stakeholder approach. Adjustment towards stakeholder governance seems certainly possible in the US, for example through the emerging model of corporate governance, the Delaware Public Benefit Corporation. The benefit corporation seems to have many if not all of the key attributes of the Dutch system and could provide a promising path forward if American corporate governance is to change in a way that makes the US model truly focused on the long-term value for all stakeholders. The question for US advocates of stakeholder governance is whether they will embrace it, or adopt another effective governance change, and make their commitment to respect stakeholders rea

Bonjour à toutes et à tous, je signale cette intéressante étude : Zetzsche, Dirk Andreas and Anker-Sørensen, Linn and Consiglio, Roberta and Yeboah-Smith, Miko, « The COVID-19-Crisis and Company Law – Towards Virtual Shareholder Meetings », 15 avril 2020, University of Luxembourg Faculty of Law, Economics & Finance, WPS 2020-007.

Extrait :

Regulators and Parliaments around the world have responded to the COVID-19 epidemic by amending company law. This crisis legislation allows us to examine how, and to what effect, the corporate governance framework can be amended in times of crisis. In fact, almost all leading industrialized nations have already enacted crisis legislation in the field of company law.

In our recent working paper, ‘The COVID-19-Crisis and Company Law – Towards Virtual Shareholder Meetings’, we have sought to (1) document the respective crisis legislation; (2) assist countries looking for solutions to respond rapidly and efficiently to the crisis; (3) exchange experiences of crisis measures; and (4) spur academic discussion on the extent to which the crisis legislation can function as a blueprint for general corporate governance reform.

Countries considered in full or in part include Australia, Austria, Belgium, Canada, China, France, Germany, Hong Kong, Italy, Luxembourg, the Netherlands, Norway, Portugal, Singapore, South Korea, Spain, Switzerland, Thailand, the United Kingdom, and the United States. Readers are encouraged to highlight any inaccuracies in our presentation of the respective laws, and to bring further crisis-related legislation not considered in this working draft to the attention of the authors. Moreover, readers are invited to indicate where there is room for improvement therein, and/or to signal the need for policy reform.

Drawing on the analysis of these more than twenty countries, we note five fields in which legislators have been particularly active. First, the extension of filing periods for annual and quarterly reports to reflect the practical difficulties regarding the collection of numbers and the auditing of financial statements. Second, company law requires shareholders to take decisions in meetings—and these meetings were for the most part in-person gatherings. However, since the gathering of individuals in one location is now at odds with the measures being implemented to contain the virus, legislators have generally allowed for virtual-only meetings, online-only proxy voting and voting-by-mail, and granted relief to various formalities aimed at protecting shareholders (including fixed meeting and notice periods). Third, provisions requiring physical attendance of board members, including provisions on signing corporate documents, have been temporarily lifted for board matters. Fourth, parliaments have enacted changes to allow for more flexible and speedy capital measures, including the disbursement of dividends and the recapitalization of firms, having accepted that the crisis impairs a company’s equity. Fifth and finally, some countries have implemented temporary changes to insolvency law to delay companies’ petitioning for insolvency as a result of the liquidity shock prompted by the imposition of overnight lockdowns.

The legislation passed in response to the COVID-19 crisis provides for an interesting case study through which to examine what can be done to modernize the corporate governance framework with a view to furthering digitalization. Given the difficulties or indeed the impossibility of conducting in-person meetings currently, the overall trajectory of company law reforms has been to allow for digitalization of corporate governance, and ensuring the permissibility of virtual shareholder meetings (VSM), in particular.

In this respect, it is safe to assume that the rules on VSM will have model character. While the details of the modus operandi of VSM will require careful adjustment, to ensure that shareholders will be afforded the same rights and opportunities to participate as they would at an in-person meeting (including Q&A), the experimental phase during the crisis will feed into the policy discussion, with some more successful and some less successful examples providing food for thought. Yet, it is safe to say that the COVID-19 pandemic has unveiled the need for virtual-only shareholder meetings, and that some types of VSM will stay for good long after the current crisis has subsided.