Voilà une belle question abordée dans ce billet du Harvard Law School Forum on Corporate Governance« What Board Members Need to Know about the “E” in ESG » (par Sheila M. Harvey, Reza S. Zarghamee et Jonathan M. Ocker, 9 juillet 2020) !

Extrait concernant les CA :

Board Responsibilities

Traditionally, a company’s board will manage corporate governance risks and executive compensation. The practical need to expand these responsibilities to account for environmental stewardship and risk management is a relatively new phenomenon, and many boards are not yet up to speed.

The first step toward properly addressing environmental matters is for the board to collaborate with management to identify the different ways in which the company’s businesses and operations interface with environmental issues. The aim here is to think expansively. For purposes of ESG, environmental matters extend beyond regulatory compliance and impacts on natural resources to include concepts such as environmental justice, carbon footprints, supply chains and product stewardship.

Consistent with this approach, an equally broad realm of potential environmental risks also should be considered. These may include the potential to cause environmental contamination and natural resource damages, which may trigger not just cleanup liabilities but also disclosure requirements in financial statements. Also relevant is the potential for business operations to be disrupted by environmental factors such as climate change.

Once potential environmental risks are identified, assessments should be made regarding their materiality and the existence of standing corporate policies and procedures to address them. Where such policies are lacking, they should be developed and implemented. Moreover, determinations should be made about how the company will present itself to investors, regulators and society to adequately inform them of potential environmental risks, avoid reputational harm and increase long-term value.

There is no one-size-fits-all solution, and companies have different environmental profiles. Each will have to find its own way, but the board should make sure that management devotes the appropriate resources to addressing environmental matters, understands environmental disclosure requirements and standards and ranking systems, and takes a proactive approach to protecting the company’s reputation from an environmental standpoint.

This is a multifaceted paradigm that requires open lines of communication between management and the board at all times. Moreover, because not every board member can be an ESG expert, we recommend that the appropriate committee be tasked in its charter with spearheading the environmental risk area for the board.

Points à retenir :

Corporate boards should partner with management to ensure appropriate and regular oversight of environmental issues critical to the long-term economic success and reputation of the company.

Either the board or an authorized committee should receive briefings on environmental matters/risks that may jeopardize a company’s reputation and corrective action undertaken to address those risks.

Management should monitor environmental disclosures and rankings of peer firms and consult with the board on how to improve their company’s standing relative to competing firms and in terms of stakeholder expectations.

La revue Banque propose une intéressante analyse par Mmes Weisman et Pruvost de l’entreprise à mission avec un angle financier que je vous livre ci-dessous : « Entreprise à mission : une promesse à confirmer ? » (18 février 2020).

Extrait :

Quel rôle pour la finance ?

L’implication de la sphère financière dans ce mouvement des entreprises à mission est vitale pour que le concept ne reste pas une coquille vide. Les entreprises qui s’engagent publiquement à devenir l’entreprise à mission posent le premier jalon d’un chemin exigeant, long et complexe ; qu’on serait tenté de qualifier de parcours du combattant.

Si la finance semble se mobiliser autour des enjeux climatiques, les acteurs n’ont pas encore pris la mesure de ce que peuvent représenter demain les sociétés à mission. Ces dernières invitent à repenser en profondeur les piliers d’un certain capitalisme et la finance qui la sous-tend. Aussi, les premiers financeurs de cette économie sont des pionniers, emmenés par plus de convictions que de méthodologies ou de pratiques harmonisées. Cependant, des lignes directrices émergent, qui définissent les grands enjeux de la finance « à mission » : des besoins d’expertise et de formation nouveaux ; de nouveaux modèles de passage à l’échelle ; des investissements de temps long ; des indicateurs renouvelés à travers une vision élargie de la valeur.

Des besoins d’expertise et de formation nouveaux

Les sociétés à mission s’engagent sur des innovations importantes. Elles repensent les chaînes d’approvisionnement, mettent en commun des innovations avec le marché, collaborent différemment avec leurs concurrents ou leurs fournisseurs, proposent de nouveaux modèles circulaires et bousculent les fondamentaux de la stratégie économique classique. Pour comprendre, suivre et évaluer les propositions, les financiers doivent se doter de savoirs nouveaux sur le climat, le carbone, les ressources naturelles, mais aussi suivre l’évolution des sciences cognitives et des études sociologiques. La définition même des marchés doit être revisitée. Il y a donc urgence à faire émerger une génération de financeurs plus aguerris sur les grands enjeux physiques et humains de notre société.

De nouveaux modèles de passage à l’échelle

Les propositions des sociétés à mission demandent à être expérimentées, sur des modèles très différents de la R&D industrielle connue. Aussi, la segmentation des champs d’expérimentation (territoriaux, au sein d’une filière, en développement avec les utilisateurs, etc.) et le partage des données nécessaires à celles-ci – à travers des plateformes ouvertes ou publiques – sont des défis clés qui demanderont, demain, des investissements importants.

Des investissements de temps long

Pour amorcer ces transitions, il est urgent d’amorcer un virage vers un capitalisme plus lent et des financements de plus long terme. Les actionnariats volatils, qui font régner une pression du résultat annuel voire trimestriel sont des freins concrets à l’émergence de ces sociétés à mission.

Des indicateurs renouvelés à travers une vision élargie de la valeur

L’évaluation de la mission est une zone en chantier qui nécessite en partie d’inventer de nouveaux indicateurs. Certaines sociétés à mission s’y essaient déjà, à l’instar de l’indice d’alignement humain d’Alenvi. Cela suppose au préalable de redéfinir les indicateurs d’évaluation de performance à tous les niveaux, à la fois au regard de la mission elle-même et de l’impact réel de l’entreprise sur les territoires, publics ou pratiques visés. Mais pas seulement : les indicateurs doivent être pensés pour pouvoir, eux aussi, être déployés à une échelle plus large de l’économie.

Il s’agit bien de dépasser à terme la fracture entre performance financière et extra-financière, pour les agréger dans une comptabilité qui englobe, en plus du capital financier, les capitaux naturels et humains, à l’image des actuels travaux de recherche sur la comptabilité à triple capital. Ces pistes de réflexion se heurtent encore, pour l’heure, à des freins idéologiques et méthodologiques. Pourtant, leur atterrissage est vital pour révéler la véritable valeur créée par ce nouveau modèle d’entreprises.

David Larcker, Bradford Lynch, Brian Tayan et Daniel Taylor publient un texte qui revient sur la transparence des ghrandes entreprises américaines en matière de COVID-19 « The Spread of Covid-19 Disclosure » (29 juin 2020). Un document plein de statistiques et de tendances sur la transparence… vraiment intéressant sachant que l’enjeu de la question n’est pas à négliger.

Extrait :

The COVID-19 pandemic presents an interesting scenario whereby an unexpected shock to the economic system led to a rapid deterioration in the economic landscape, causing sharp changes in performance relative to expectations just a few months prior. For most companies, the pandemic has been detrimental. For a few, it brought unexpected demand. In many cases, supply chains have been strained, causing ripple effects that extend well beyond any one company.

How do companies respond to such a situation? What choices do they make, and how much transparency do they offer? How does disclosure vary in a setting where the potential impact is so widely uncertain? The COVID-19 pandemic provides a unique setting to examine disclosure choices in a situation of extreme uncertainty that extends across all companies in the public market. This devastating outlier event provides a rare glimpse into disclosure behavior by managers and boards.

Why This Matters

The COVID-19 pandemic provides a unique opportunity to examine disclosure practices of companies relative to peers in real time about a somewhat unprecedented shock that impacted practically every publicly listed company in the U.S. We see that decisions varied considerably about whether to make disclosure and, if so, what and how much to say about the pandemic’s impact on operations, finances, and future. What motivates some companies to be forthcoming about what they are experiencing, while others remain silent? Does this reflect different degrees of certitude about how the virus would impact their businesses, or differences in managements’ perception of their “obligations” to be transparent with the public? What does this say about a company’s view of its relation and duty to shareholders?

In one example, we saw a consumer beverage company make zero references to COVID-19 in its SEC filings and website, despite the virus plausibly having at least some impact on its business. In another example, we saw a company claim no material changes to its previously reported risk factors when managers almost certainly had relevant information about the virus and the likely impact on sales and operations. What discussion among the senior managers, board members, external auditor, and general counsel leads to a decision to make no disclosures? What should shareholders glean from this decision, particularly in light of peer disclosure?

The COVID-19 pandemic represents a so-called “black swan” event that inflicted severe and unexpected damage to wide swaths of the economy. What strategic insights will companies learn from this event? Can boards use these insights to prepare for other possible outlier events, such as climate events, terrorism, cyber-attacks, pandemics, and other emergencies? Should these insights be disclosed to shareholders?

“The future of business will be different,” surmised a director on a recent virtual board roundtable hosted by RSR Partners, “in ways we can’t anticipate in this moment. Our board is focused on assessing whether all our directors are truly ready for what’s coming.”

Over the past few months, RSR Partners hosted more than a dozen roundtables for sitting directors, providing a forum for the participants to share what their boards are learning as they navigate the current crisis and pivot into the “new normal.” While tackling topics as diverse as commercial strategy, operations, health and safety, and the future of business, one theme was pervasive throughout the discussions: leadership and stakeholders will be looking to the boardroom for guidance, and board members not only need to have the requisite experience and skills to confidently provide direction, but the leadership characteristics that will allow them to be effective.

Fundamentally, the global business disruption and current uncertainty has created a need for a higher level of involvement from board members. “This is a time to have board members who have experienced really tough issues, such as major ecessions, difficult mergers, major cost cutting, insolvency and bankruptcy, and top management departures, along with experience in reinventing companies, including supply chain, product engineering and simplification, digital transformation, offshore manufacturing and procurement, sale of subsidiaries, and comprehensive refinancing,” stated Edward A. Kangas, former Chairman and CEO of Deloitte Touche. “This is not a time for deep thinking. It’s time for people with real experience who know how to oversee and support management in a time of crisis and reinvention.” (Mr. Kangas currently serves on the following boards: Deutsche Bank USA Corp., Intelsat SA, VIVUS, Inc., and Hovnanian Enterprises, Inc.).

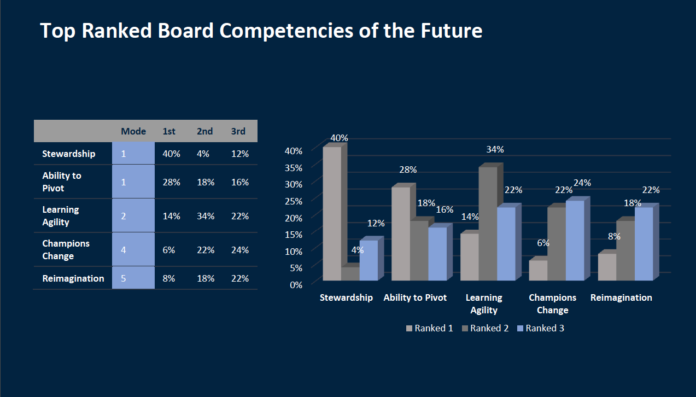

Characteristics of Directors Who Succeed in the “New Normal”

From a practical perspective, there is now a higher premium placed on a director’s proven ability to navigate a business through a crisis while mitigating risk and understanding how and when to pull the levers that will impact balance sheets. The demand to optimize results, sustain business, and adapt to changes in a regional and global market has increased alongside the time commitment and attention to detail required of directors to address these issues. Normal requirements for sound governance, audit oversight, compensation strategies, business performance goals, and succession of key leadership have continued to be paramount during the crisis. However, what the current crisis has forced boards to recognize is that a combination of specialized and diversified skillsets and characteristics will produce good corporate governance in and after 2020.

In addition to listening to the characteristics discussed in the recent roundtables, RSR Partners polled more than 250 public company board members of Fortune 50-1000 companies to identify the traits they hope to see emerge in this generation of board members. The results indicated that stewardship, the ability to pivot and learn agility, to be a champion of change, and to be capable of reimagination will be most needed by the directors charged with steering their boards in the “new normal.”

As businesses start to look beyond the COVID-19 crisis, the EY Global Integrity Report 2020 reveals divisions on the repercussions for company ethics as a result of the pandemic.

The findings are part of a survey of almost 3,000 respondents from 33 countries up to February 2020, analyzing the ethical challenges companies face in turbulent times. An additional 600 employees across all levels of seniority were surveyed at the height of the COVID-19 crisis in April in companies across six countries – China, Germany, Italy, the UK, India and the US.

The majority (90%) of respondents surveyed during the crisis believe that disruption, as a result of COVID-19, poses a risk to ethical business conduct, but there is a concerning disparity between boards, senior management and employees on the implications for compliance. While 43% of board members and 37% of senior managers surveyed believe the pandemic could lead to change and better business ethics, only 21% of junior employees appear to agree.

The survey highlights that signs of an integrity disconnect at different levels within organizations were evident even before the pandemic with more than half of board members (55%) believing management demonstrate professional integrity, but only 37% of junior employees sharing the same sentiment. In addition, over half of board members (55%) believe there are managers in their organization who would sacrifice integrity for short term gain.

La crise de la COVID-19 met en relief l’importance de l’investissement responsable. Deux consultantes expertes dans le domaine invitent les comités de retraite à préparer les bonnes questions à poser à leurs gestionnaires de portefeuille.

Random and arbitrary compliance with various initiatives makes companies’ sustainable practices ‘less’ rather than ‘more’ transparent. Our paper offers a comprehensive view on different reporting frameworks. It shows that there is a need to provide some clarity in this complex landscape. Fundamentally, the current reporting landscape is unlikely to impact positively on efforts towards sustainability. We suggest in our paper hat the scope of the NFRD, as the most promising of the existing initiatives, should be revisited so as to enhance its contribution to furthering corporations’ sustainable practices. Our paper supports reform of the NFRD which has constituted a positive step in the right direction. What is required now is stronger guidance on what to report and how to report it. Steps are being taken in the right direction towards clarifying metrics around sustainability (World Economic Forum 2020). A standardized and streamlined framework is necessary in order to pin companies down to something more concrete, rather than giving them too much choice on which guidelines, frameworks or recommendations they may opt to follow. Stronger, clearer and more concrete definitions of key concepts are required, as well as clarification of the rights of stakeholders in this area of activity. Proposals for reform that have arisen, with a consultation exercise by the European Commission, (European Commission Consultation 2020) are therefore to be welcomed. We suggest an expansion of the NFRD’s scope and that it represent sustainability as a positive instead of reducing the focus only to negative risks. EU member states and companies should have opportunities for effective compliance with the reporting requirements, with the NFRD better defining the concepts it refers to.