Intéressant article du professeur étatsunien Stephen Bainbridge sur la fameuse décision américaine Dodge v. Ford Motor Co. : « Why We Should Keep Teaching Dodge v. Ford Motor Co. » (UCLA School of Law, Public Law Research Paper No. 22-05, 5 avril 2022). Le titre ne laissera personne indifférent puisqu’il est exactement à l’opposé de celui de la professeure Lynn Stout publié en 2008 !

The Securities and Exchange Commission (“Commission”) is proposing for public comment amendments to its rules under the Securities Act of 1933 (“Securities Act”) and Securities Exchange Act of 1934 (“Exchange Act”) that would require registrants to provide certain climate-related information in their registration statements and annual reports. The proposed rules would require information about a registrant’s climate-related risks that are reasonably likely to have a material impact on its business, results of operations, or financial condition. The required information about climate-related risks would also include disclosure of a registrant’s greenhouse gas emissions, which have become a commonly used metric to assess a registrant’s exposure to such risks. In addition, under the proposed rules, certain climate-related financial metrics would be required in a registrant’s audited financial statements.

L’IGOPP affirme dans cette prise de position qu’il n’est ni approprié ni opportun d’imposer cette procédure du vote consultatif à l’ensemble des entreprises au pays.

Une gouvernance pleinement assumée par des conseils d’administration responsables et imputables forme la pierre angulaire du fonctionnement des sociétés cotées en Bourse. L’établissement de la rémunération des dirigeants incombe, juridiquement et pratiquement, au conseil d’administration.

L’IGOPP souligne alors que la démarche de vote consultatif (« say-on-pay ») sur la rémunération manifeste une méfiance, méritée ou non, envers les conseils d’administration. Derrière cette démarche se profile un déplacement significatif de responsabilité pour la gouvernance des sociétés du conseil vers les actionnaires. Si on ne peut se fier aux administrateurs d’une entreprise pour prendre de bonnes décisions en ce qui a trait à la rémunération de la haute direction, comment les actionnaires peuvent-ils leur faire confiance pour d’autres décisions tout aussi, sinon plus, importantes?

Dans les cas spécifiques de rémunérations problématiques, les investisseurs devraient être prêts à utiliser leur droit de vote (ou de «s’abstenir») pour contrer l’élection de certains administrateurs, particulièrement les membres du comité de rémunération (ou ressources humaines), dans les quelques cas où le conseil n’aurait pas agi de façon responsable.

Au Canada donc, la tenue d’un vote consultatif était alors une décision de l’entreprise et non pas obligatoire comme c’est le cas aux États-Unis.

Or, en avril 2019, le projet de Loi C-97 amendant la Loi canadienne sur les sociétés par actions (LCSA), stipule notamment que les sociétés inscrites en bourse et constituées selon le régime fédéral des sociétés par actions devront adopter « une approche relative à la rémunération des administrateurs et des employés de la société qui sont des « membres de la haute direction » et présenter aux actionnaires l’approche relative à la rémunération à chaque assemblée annuelle, et les actionnaires devront voter sur l’approche présentée selon un format non contraignant.

Si la loi a été sanctionnée le 21 juin 2019, les modifications apportées aux articles cités ci-dessus ne sont toujours pas en vigueur. Toutefois, au moment où les modifications s’appliqueront, on prévoit qu’environ 500 entreprises additionnelles pourraient être contraintes de tenir un vote consultatif sur la rémunération de leurs dirigeants.

Statistiques sur le vote consultatif sur la rémunération des dirigeants (say-on-pay)

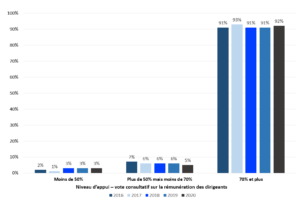

Aux États-Unis, où le vote consultatif sur la rémunération des dirigeants est obligatoire, la grande majorité des entreprises obtiennent annuellement un appui considérable des actionnaires à la politique de rémunération proposée, comme on peut le constater à la Figure 1. En effet, 92% des sociétés américaines du Russell 3000 ont obtenu un vote favorable de 70% et plus des droits de votes exercés, avec un niveau moyen d’appui (pourcentage de votes favorables) de 90% pour l’ensemble des firmes en 2020.

Fait intéressant, le niveau moyen d’appui atteint 93% (94% en 2019) lorsque l’agence de conseil en vote ISS donne une recommandation favorable, alors que ce niveau d’appui baisse à 64% (aussi 64% en 2019) en moyenne lors d’une recommandation défavorable. Ceci démontre bien l’influence d’ISS dans l’exercice des votes lorsqu’elle émet des recommandations. En 2020, ISS a émis une recommandation défavorable dans 11% des cas.

Statistiques canadiennes

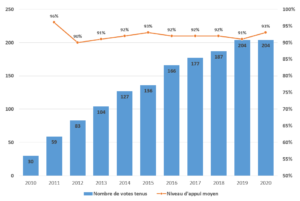

Jusqu’à maintenant en 2020 , 204 votes consultatifs sur la rémunération des dirigeants ont été tenus au Canada, dont 154 par des sociétés constituantes de l’indice S&P/TSX (soit 69,7% d’entre elles). Le nombre d’entreprises qui tiennent un tel vote a été en constante croissance depuis 2010, malgré le caractère volontaire de l’exercice, puis s’est stabilisé depuis 2019. Comme on peut le constater à la Figure 2, le niveau moyen d’appui à la politique de rémunération proposée est semblable à celui observé aux États-Unis, avec des taux au-delà de 90% annuellement.

En 2020, seulement 13 sociétés canadiennes qui ont tenu un vote consultatif sur la rémunération ont obtenu un appui inférieur à 80% (mais néanmoins tous supérieur à 50%). ISS n’a émis aucune recommandation défavorable au cours de la dernière année au Canada.

Mise à jour : Résultats d’études menées au cours des cinq dernières années

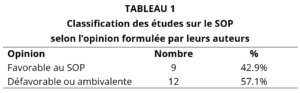

Nous avons analysé les résultats et les conclusions de 21 articles scientifiques ou théoriques publiés entre novembre 2015 et novembre 2020, et portant sur le SOP (pour une description des résultats et des conclusions des différentes études, voir à l’Annexe 1). Le Tableau 1 ci-dessous rend compte de la classification des opinions des auteurs (selon leur propre appréciation).

Ainsi, de façon générale, davantage d’études témoignent d’effets limités, voire indésirables, du SOP. Le constat était analogue lors du dernier exercice similaire mené par l’IGOPP en 2015, alors qu’une forte majorité des études publiées entre 2010 et 2015 (70% des études qui avaient été analysées à l’époque) montraient des effets défavorables du SOP.

Un examen des études dites « favorables » révèle que plus de la moitié d’entre elles portent sur des entreprises qui ont subi un vote défavorable, et ces études ne considèrent donc pas réellement l’effet du SOP sur l’ensemble des autres firmes. Or, comme le soulignait la position de l’IGOPP, les actionnaires ont d’autres mécanismes que le SOP pour faire valoir leur mécontentement, et ces autres mécanismes auraient très bien pu avoir le même effet en bout de piste.

D’ailleurs, même l’agence de conseil en vote Glass Lewis adopte une ligne directrice en ce sens au Canada :

En général, Glass Lewis estime que les actionnaires ne devraient pas être directement impliqués dans la fixation de la rémunération des dirigeants. Ces questions devraient être laissées au comité de rémunération. En l’absence d’un vote consultatif «Say-on-Pay», nous considérons l’élection des membres du comité de rémunération comme un mécanisme approprié permettant aux actionnaires d’exprimer leur désapprobation ou leur soutien à la politique du conseil d’administration sur la rémunération des dirigeants.

Un enjeu important se manifeste: les entreprises seraient-elles tentées d’adopter des formes de rémunération « conformes » aux diktats en cette matière promulgués par les agences de conseil en vote (ISS et autres) afin de réduire le risque d’une recommandation défavorable de ces agences lors du vote SOP. Si cela était, la conséquence serait des politiques de rémunération uniformes, souvent mal adaptées aux contextes particuliers de chacune des entreprises.

Quoiqu’il en soit, les résultats des études scientifiques portant sur le SOP depuis 2010 appuient majoritairement le scepticisme exprimé par l’IGOPP dans sa prise de position à ce sujet.

Vyacheslav Fos et Clifford Holderness publient un article sur la distribution des droits de vote des actionnaires sur la bourse NYSE : « The Distribution of Voting Rights to Shareholders » (ECGI Finance Series 733/2021).

Résumé

This is the first comprehensive study of the distribution of voting rights to shareholders. Only those owning stock on the record date may vote. Firms, however, reveal that date after the fact 91% of the time. With controversial votes, firms are more likely to do the opposite, and this is associated with a lower passage rate for shareholder-initiated proposals.

The NYSE sells non-public record-date information to select investors. When stocks go ex vote, prices decline and trading volume often surges, suggesting that investors are buying marginal votes. These trends are most pronounced with controversial votes.

Alors que tout le monde évoque le changement de paradigme lié à l’émergence d’un « stakeholderism », le Wall Street Journal lance un pavé dans la mare sous la plume notamment du professeur Bebchuk : rien n’a vraiment changé ! « ‘Stakeholder’ Capitalism Seems Mostly for Show » (Wall Street Journal, 6 août 2020)

Extrait :

Notwithstanding statements to the contrary, corporate leaders are generally still focused on shareholder value. They can be expected to protect other stakeholders only to the extent that doing so would not hurt share value.

That conclusion will be greatly disappointing to some and welcome to others. But all should be clear-eyed about what corporate leaders are focused on and what they intend to deliver.

Excellente lecture ce matin de ce billet du Harvard Law School Forum on Corporate Governance : « Legal Liability for ESG Disclosures » (de Connor Kuratek, Joseph A. Hall et Betty M. Huber, 3 août 2020). Dans cette publication, vous trouverez non seulement une belle synthèse des référentiels actuels, mais aussi une réflexion sur les conséquences attachées à la mauvaise divulgation d »information.

Extrait :

3. Legal Liability Considerations

Notwithstanding the SEC’s position that it will not—at this time—mandate additional climate or ESG disclosure, companies must still be mindful of the potential legal risks and litigation costs that may be associated with making these disclosures voluntarily. Although the federal securities laws generally do not require the disclosure of ESG data except in limited instances, potential liability may arise from making ESG-related disclosures that are materially misleading or false. In addition, the anti-fraud provisions of the federal securities laws apply not only to SEC filings, but also extend to less formal communications such as citizenship reports, press releases and websites. Lastly, in addition to potential liability stemming from federal securities laws, potential liability could arise from other statutes and regulations, such as federal and state consumer protection laws.

A. Federal Securities Laws

When they arise, claims relating to a company’s ESG disclosure are generally brought under Section 11 of the Securities Act of 1933, which covers material misstatements and omissions in securities offering documents, and under Section 10(b) of the Securities Exchange Act of 1934 and rule 10b-5, the principal anti-fraud provisions. To date, claims brought under these two provisions have been largely unsuccessful. Cases that have survived the motion to dismiss include statements relating to cybersecurity (which many commentators view as falling under the “S” or “G” of ESG), an oil company’s safety measures, mine safety and internal financial integrity controls found in the company’s sustainability report, website, SEC filings and/or investor presentations.

Interestingly, courts have also found in favor of plaintiffs alleging rule 10b-5 violations for statements made in a company’s code of conduct. Complaints, many of which have been brought in the United States District Court for the Southern District of New York, have included allegations that a company’s code of conduct falsely represented company standards or that public comments made by the company about the code misleadingly publicized the quality of ethical controls. In some circumstances, courts found that statements about or within such codes were more than merely aspirational and did not constitute inactionable puffery, including when viewed in context rather than in isolation. In late March 2020, for example, a company settled a securities class action for $240 million alleging that statements in its code of conduct and code of ethics were false or misleading. The facts of this case were unusual, but it is likely that securities plaintiffs will seek to leverage rulings from the court in that class action to pursue other cases involving code of conducts or ethics. It remains to be seen whether any of these code of conduct case holdings may in the future be extended to apply to cases alleging 10b-5 violations for statements made in a company’s ESG reports.

B. State Consumer Protection Laws

Claims under U.S. state consumer protection laws have been of limited success. Nevertheless, many cases have been appealed which has resulted in additional litigation costs in circumstances where these costs were already significant even when not appealed. Recent claims that were appealed, even if ultimately failed, and which survived the motion to dismiss stage, include claims brought under California’s consumer protection laws alleging that human right commitments on a company website imposed on such company a duty to disclose on its labels that it or its supply chain could be employing child and/or forced labor. Cases have also been dismissed for lack of causal connection between alleged violation and economic injury including a claim under California, Florida and Texas consumer protection statutes alleging that the operator of several theme parks failed to disclose material facts about its treatment of orcas. The case was appealed to the U.S. Court of Appeals for the Ninth Circuit, but was dismissed for failure to show a causal connection between the alleged violation and the plaintiffs’ economic injury.

Overall, successful litigation relating to ESG disclosures is still very much a rare occurrence. However, this does not mean that companies are therefore insulated from litigation risk. Although perhaps not ultimately successful, merely having a claim initiated against a company can have serious reputational damage and may cause a company to incur significant litigation and public relations costs. The next section outlines three key takeaways and related best practices aimed to reduce such risks.

C. Practical Recommendations

Although the above makes clear that ESG litigation to date is often unsuccessful, companies should still be wary of the significant impacts of such litigation. The following outlines some key takeaways and best practices for companies seeking to continue ESG disclosure while simultaneously limiting litigation risk.

Key Takeaway 1: Disclaimers are Critical

As more and more companies publish reports on ESG performance, like disclaimers on forward-looking statements in SEC filings, companies are beginning to include disclaimers in their ESG reports, which disclaimers may or may not provide protection against potential litigation risks. In many cases, the language found in ESG reports will mirror language in SEC filings, though some companies have begun to tailor them specifically to the content of their ESG reports.

From our limited survey of companies across four industries that receive significant pressure to publish such reports—Banking, Chemicals, Oil & Gas and Utilities & Power—the following preliminary conclusions were drawn:

All companies surveyed across all sectors have some type of “forward-looking statement” disclaimer in their SEC filings; however, these were generic disclaimers that were not tailored to ESG-specific facts and topics or relating to items discussed in their ESG reports.

Most companies had some sort of disclaimer in their Sustainability Report, although some were lacking one altogether. Very few companies had disclaimers that were tailored to the specific facts and topics discussed in their ESG reports:

In the Oil & Gas industry, one company surveyed had a tailored ESG disclaimer in its ESG Report; all others had either the same disclaimer as in SEC filings or a shortened version that was generally very broad.

In the Banking industry, two companies lacked disclaimers altogether, but the rest had either their SEC disclaimer or a shortened version.

In the Utilities & Power industry, one company had no disclaimer, but the rest had general disclaimers.

In the Chemicals industry, three companies had no disclaimer in their reports, but the rest had shortened general disclaimers.

There seems to be a disconnect between the disclaimers being used in SEC filings and those found in ESG In particular, ESG disclaimers are generally shorter and will often reference more detailed disclaimers found in SEC filings.

Best Practices: When drafting ESG disclaimers, companies should:

Draft ESG disclaimers carefully. ESG disclaimers should be drafted in a way that explicitly covers ESG data so as to reduce the risk of litigation.

State that ESG data is non-GAAP. ESG data is usually non-GAAP and non-audited; this should be made clear in any ESG Disclaimer.

Have consistent disclaimers. Although disclaimers in SEC filings appear to be more detailed, disclaimers across all company documents that reference ESG data should specifically address these issues. As more companies start incorporating ESG into their proxies and other SEC filings, it is important that all language follows through.

Key Takeaway 2: ESG Reporting Can Pose Risks to a Company

This article highlighted the clear risks associated with inattentive ESG disclosure: potential litigation; bad publicity; and significant costs, among other things.

Best Practices: Companies should ensure statements in ESG reports are supported by fact or data and should limit overly aspirational statements. Representations made in ESG Reports may become actionable, so companies should disclose only what is accurate and relevant to the company.

Striking the right balance may be difficult; many companies will under-disclose, while others may over-disclose. Companies should therefore only disclose what is accurate and relevant to the company. The US Chamber of Commerce, in their ESG Reporting Best Practices, suggests things in a similar vein: do not include ESG metrics into SEC filings; only disclose what is useful to the intended audience and ensure that ESG reports are subject to a “rigorous internal review process to ensure accuracy and completeness.”

Key Takeaway 3: ESG Reporting Can Also be Beneficial for Companies

The threat of potential litigation should not dissuade companies from disclosing sustainability frameworks and metrics. Not only are companies facing investor pressure to disclose ESG metrics, but such disclosure may also incentivize companies to improve internal risk management policies, internal and external decisional-making capabilities and may increase legal and protection when there is a duty to disclose. Moreover, as ESG investing becomes increasingly popular, it is important for companies to be aware that robust ESG reporting, which in turn may lead to stronger ESG ratings, can be useful in attracting potential investors.

Best Practices: Companies should try to understand key ESG rating and reporting methodologies and how they match their company profile.

The growing interest in ESG metrics has meant that the number of ESG raters has grown exponentially, making it difficult for many companies to understand how each “rater” calculates a company’s ESG score. Resources such as the Better Alignment Project run by the Corporate Reporting Dialogue, strive to better align corporate reporting requirements and can give companies an idea of how frameworks such as CDP, CDSB, GRI and SASB overlap. By understanding the current ESG market raters and methodologies, companies will be able to better align their ESG disclosures with them. The U.S. Chamber of Commerce report noted above also suggests that companies should “engage with their peers and investors to shape ESG disclosure frameworks and standards that are fit for their purpose.”

L’Harvard Law School Forum on Corporate Governance publie un bel article sur les conséquences de la COVID-19 sur la rémunération des hauts dirigeants des entreprises américaines : « COVID-19 and Executive Pay: Initial Reactions and Responses« (de Stephen Charlebois, Phillip Pennell, and Rachel Ki).

Extrait :

Though businesses have managed executive pay programs through tough economic conditions before, they now must do so under an unprecedented confluence of external expectations and scrutiny, from the advent of Say on Pay to increased shareholder engagement to the beginning of an era of stakeholder primacy.

While results vary across industries, findings indicate that a majority of U.S. corporations have not yet formulated a response to COVID-19 on executive pay but anticipate taking some form of action later in 2020.

What should you take away from the results of this survey?

There is no universal response. Findings indicate a variety of approaches influenced by company outlook, industry dynamics and broader context

That said, most companies are delaying action until there is greater clarity. Companies that already made pay decisions are generally waiting until payout determinations to see if adjustments are necessary, and those that have not yet made decisions in 2020 are delaying until the impact of COVID-19 is better understood

Companies acting now are doing so out of necessity and are primarily in the hardest-hit industries where immediate cash preservation is a key priority

What are key considerations going forward?

Timely, effective communication is key. Shareholders, employees and customers are all closely monitoring the actions companies are taking in response to the crisis; if decisions are made, transparent and honest communication can build positive alignment and strengthen relationships with key stakeholders

Align executive pay with the stakeholder experience. Company actions are being closely monitored and the expectation is that shareholder experience should be reflected in compensation decisions (i.e., significant shareholder value losses or headcount reductions are accompanied by lower pay outcomes for executives)

Establish objective principles for using discretion. While quantitative metrics may be difficult to rely on at this time, establishing a list of factors for Committees to consider if they decide to apply discretion at the end of the year will allow companies to demonstrate that decisions were made in ways that demonstrably tie back to business context.