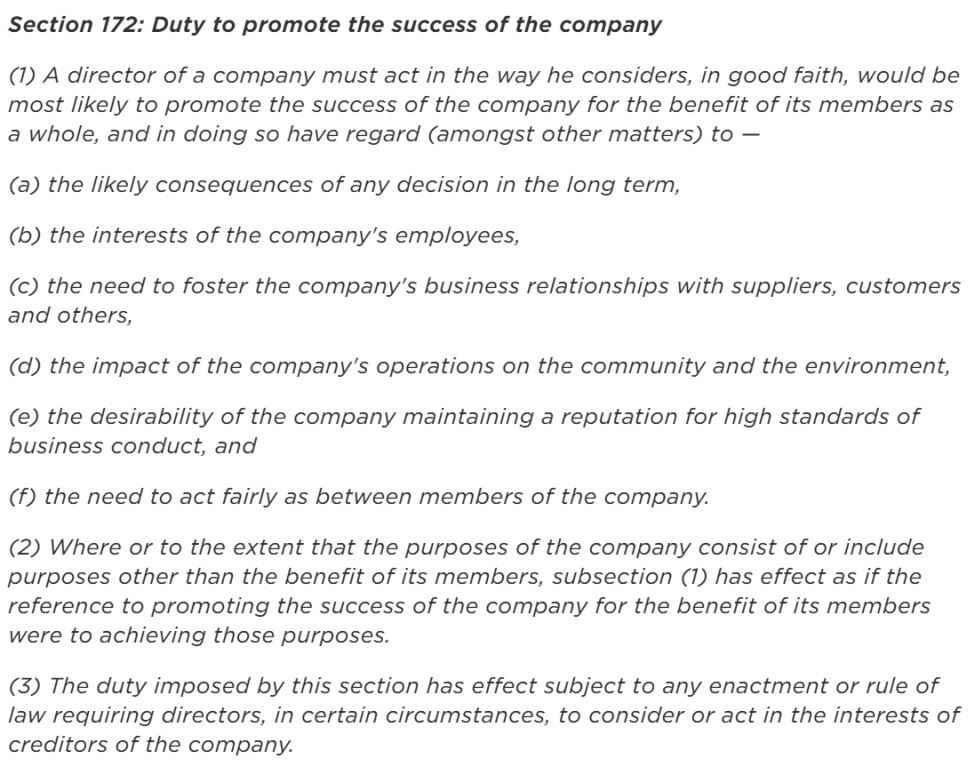

A nuance to director’s duties in the United Kingdom is the expansive statutory delineation of s 172, which endows numerous considerations for directors when acting to promote the success of the company for the benefit of members. Given the unique circumstances of the present-day commercial sphere and the more humanitarian demands being put to businesses, having a statutory foundation upon which to base non-traditional business strategies may assist effective decision-making and financial reporting.

The initial three considerations enshrined within s 172 are (a) the likely long term consequences of any decision, (b) the interests of employees and (c) the need to foster business relationships with suppliers, customers and others. These factors are of particular relevance for firms who sought justification for voluntary shutdown of businesses prior to the wider governmental shutdown.

(…)

Where production changes become quasi-humanitarian in tone and companies internalise cost in the interim, directors may seek justification through s 172(1)(d) and (e), these being the impact on the community and the desirability of maintaining high business standards respectively. Accordingly, directors can seek to frame these quasi-humanitarian efforts in long-term reputational terms, thereby engendering prospective communitarian goodwill.

Furthermore, as political pressure mounts, boards may evaluate reputational factors not simply in terms of market reputation, but also in terms of Governmental co-operation. This is particularly so where companies face increased intervention by public authorities through the Civil Contingencies Act. Comparatively, in a recent memorandum the Trump administration has attempted to exert control over the distribution of ventilators by the multinational conglomerate 3M. Cautious of such intervention occurring within their own enterprises, companies may shift business operations to such an extent to signal their compliance and co-operation with public authorities, thereby disincentivising the wholesale overrule of board discretion.

Within jurisdictions with vaguer duties to act bona fide in the best interests of the company (Delaware, Australia, Ireland), directors may still engage in such quasi-humanitarian efforts. Nevertheless, utilising s 172 to steer directorial judgment may assist effective decision-making, and furthermore guide financial reporting, which mandates s 172 director’s statements. Given that the tenor of 2020 reports will be likely dominated by COVID-19, UK directors will benefit from the homogenising structure of s 172 when making such disclosures in the coming months.

Bonjour à toutes et à tous, mon nouveau billet sur Contact vient d’être publié. Il s’intéresse aux actionnaires dans le contexte de la COVID-19 et est intitulé « COVID-19: actionnaires, engagez-vous! » (10 mai 2020).

Extrait :

(…) Ainsi, les entreprises ont besoin des actionnaires, mais, bien au-delà de leur argent, c’est de leurs valeurs qu’elles ont besoin. La crise de la COVID-19 est une occasion unique pour ces gens d’affaires de redevenir des parties prenantes responsables, plutôt que des «actionnaires-investisseurs » qui depuis trop longtemps, comme des passagers clandestins, se cachent derrière leur irresponsabilité et la seule financiarisation des entreprises.

(…) Or, si l’engagement demeure une attitude souhaitable de la part des actionnaires en temps normal, il devient une nécessité dans le contexte de la pandémie sanitaire actuelle. Dans un moment si chaotique et incertain, la contribution des actionnaires s’avère essentielle au succès du plan de relance du Canada et du Québec. Une fois cette observation faite, encore faut-il répondre à nombre de questions: que devraient faire les actionnaires? Quelle attitude devraient-ils adopter? Comment devraient-ils s’engager?

(…)

Rester calme

Se concentrer sur la COVID-19

Défendre une approche de long terme

S’assurer de sécuriser la position des salariés

Abandonner les sacro-saints dividendes

Se montrer financièrement prudent et souple

Maintenir les relations avec les fournisseurs et les consommateurs

Être vigilant à l’égard de la démocratie actionnariale

(…)

Les actionnaires ont certes des droits, mais il est temps qu’ils assument des obligations, notamment en matière de RSE et de gestion adéquate des parties prenantes d’une entreprise. Autrement dit, ils devraient encourager une gestion financière responsable qui permette aux entreprises de prioriser les employés, les sous-traitants, les fournisseurs et le succès à plus long terme de l’entreprise en mettant de côté les avantages consentis aux dirigeants ainsi que les rachats et les dividendes pour les actionnaires.

Avec la COVID-19, les entreprises peuvent légitimement donner corps à la RSE (voir mon billet de blogue) et dire adieu à la fameuse théorie de la primauté actionnariale. Ce n’est pas parce que le droit est (à notre sens) imparfait et donne la possibilité aux actionnaires d’agir le plus égoïstement possible (voir mon billet de blogue) que ce comportement est celui à adopter. Après tout, la crise peut être vue comme une porte ouverte vers la RSE!

(…)

Cela fait bien longtemps que les juristes ont observé que les actionnaires se désintéressent du sort des entreprises où leurs fonds sont placés. Encore plus quand ce ne sont pas eux, mais des professionnels qui placent leurs fonds en leur nom et pour leur compte. Au fil du temps, les actionnaires se sont transformés en prêteurs qui réclament une rentabilité tout en rejetant l’investissement qu’elle implique. D’ailleurs, le droit leur impose peu d’obligations, si ce n’est de réaliser le paiement en contrepartie du titre qu’ils reçoivent. Toutefois, «[l]es choses n’ont pas été données au départ et ne sont pas pour ainsi dire naturelles».

Alors, actionnaires, retenez une chose de la crise sanitaire mondiale: que cela vous plaise ou non, il va falloir sérieusement vous engager. L’heure est venue d’entendre le clap de fin pour la responsabilité limitée des actionnaires, même si elle demeure ancrée dans le droit des sociétés par actions! C’est à ce prix que les entreprises pourront se redresser.

Dans le cadre du cours DRT-7022 Gouvernance de l’entreprise du Professeur Ivan Tchotourian, nos étudiants ont eu l’opportunité de réfléchir sur un sujet pendant toute une session. Voici le fruit de leur réflexion !

Article 172 du droit des sociétés britanniques, utile ou pas ?

Le Royaume-Uni a vu entre 2006 et 2009 entrer en vigueur le Companies Act 2006 remplaçant le précédent Companies Act de 1985. Cette loi apporte des modifications à presque tous les aspects du droit des sociétés britanniques. Parmi les principales nouveautés, nous pouvons tout d’abord mentionner la consécration du devoir des administrateurs et des dirigeants de promouvoir le succès de l’entreprise, par le renforcement de la voix des parties prenantes. Ce renforcement passe à travers différentes propositions consacrées par l’article 172.

Le 29 août 2017, le gouvernement britannique a publié « Corporate Governance Reform : The Government Response to the Green Paper Consultation », proposant des mesures sur deux enjeux : la prise en compte des parties prenantes dans leur ensemble par le conseil d’administration de l’entreprise, ainsi que sur la rémunération des dirigeants. En somme, le gouvernement suggère d’utiliser le mécanisme de « comply or explain » et l’instrument législatif afin de soumettre de nouvelles propositions à ajouter à cet article.

Le gouvernement s’attaque également à la rémunération des dirigeants, par un encadrement souple se concrétisant à travers différents outils, tels que : le « name and shame », le ratio, ainsi que le comité de rémunération.

The House of commons, chambre basse du parlement du Royaume-Uni, a par son comité « Business, Energy and Industrial Strategy », a publié quelques recommandations suite à une enquête effectuée en 2016. Dans l’objectif d’améliorer l’accessibilité ainsi que l’application de l’article 172 par les sociétés britanniques, il ressort des recommandations du comité notamment la mise en place de rapports au sujet de la politique des entreprises, qui devront être publiés. Mais aussi la création de groupes consultatifs composés des différentes parties prenantes, la rédaction et l’application d’un nouveau code de gouvernance de l’entreprise aux sociétés britanniques cotées et non cotées, et l’attribution de nouvelles missions au Financial Reporting Council.

Mais aussi la création de groupes consultatifs composés des différentes parties prenantes, la rédaction et l’application d’un nouveau code de gouvernance de l’entreprise aux sociétés britanniques cotées et non cotées, et l’attribution de nouvelles missions au Financial Reporting Council.

L’article 172 suite à sa promulgation introduit dans le cadre légal britannique le devoir des administrateurs de « promouvoir le succès de leur société dans l’intérêt de ses membres en prenant en considération l’ensemble des parties prenantes », par la codification de règles issues de la common law. Cet article suppose de la part des administrateurs de non seulement prendre en considération l’ensemble des parties prenantes, mais également d’agir de bonne foi au profit du succès de l’entreprise.

Cependant cet article connaît bon nombre de critiques, en effet, il lui est d’abord reproché l’inexistence de moyens de recours pour les parties prenantes autres que les actionnaires, le rôle normalement protecteur de l’article 172 à l’égard des parties prenantes est limité en dehors de la promotion des intérêts des actionnaires.

Toutefois, malgré les critiques supportées par cet article, grand nombre de pays s’en sont inspirés afin d’améliorer leurs codes de gouvernance d’entreprise.

1. Over the last several years, investors and proxy advisory firms have increasingly focused their attention on environmental, sustainability and governance (ESG) and human capital management (HCM) issues. While there is no one definition of HCM, the term is widely used to cover a very broad range of workforce matters that are of concern to investors and the public as they focus on building long-term value and reducing business and reputational risks. These concerns have resulted in calls for enhanced company disclosures about their HCM practices and processes.

2. Under Delaware and federal law, directors have no duties that are specifically focused on HCM. However, under Delaware law and that of many other states, directors have duties of care, loyalty and oversight that can under certain circumstances apply to HCM matters and can result in director liability.

3. While federal securities laws and rules contain several corporate disclosure requirements that apply to employees and touch on HCM issues, current laws and rules are not as robust or focused as many investors would like and have proposed. In response to rulemaking and other investor requests, the U.S. Securities and Exchange Commission has proposed amendments to its disclosure rules that would expressly require companies to describe their human capital resources to the extent that they are material to an understanding of a company’s business as a whole.

4. Some public companies have already articulated board responsibilities for oversight of HCM matters; some have renamed and expanded the responsibilities of their compensation committees to reflect their expanded focus; and some have disclosed their HCM polices and efforts in their securities law filings and other publications.

5. Separate and apart from the legal requirements that apply to corporate board duties and corporate disclosure requirements, there are important business, governance and reputational reasons for boards and companies to care about and address HCM matters. 6. While there is no one-size-fits-all approach to board oversight of HCM matters, areas for possible board attention are (i) diversity and inclusion, (ii) employee satisfaction and engagement, (iii) succession and talent management, (iv) attrition and retention, and (v) ethics, workforce culture and risk.

Universal threats can unite opposing camps in a common effort. The new coronavirus has hit almost every country and has created a shared understanding that every effort to contribute, however small it may be, is needed to overcome the crisis. Many businesses, typically criticised for giving priority to profits and to the interests of shareholders and managers, are part of the common response to the virus.

(…)

It is very unlikely that the virus has suddenly changed the corporate world. Clearly, the motivations of businesses for doing good may differ. While some have a genuine sense about their role in fighting the virus and helping those in need, many others view the crisis as a well-calculated opportunity to amend their battered reputations as partners and employers and gain advantage over competitors once the pandemic is over. But regardless of the motivations, the reaction of the corporate world to the pandemic offers three lessons for the promotion of responsible business practices in normal times.

First, in the absence of legislative action, change in corporate behaviour happens when there is broad consensus in society that collective action in response to a threat is an urgent priority. It is not poor ethics or morals that hold businesses back from working together with other parts of society, but disagreements about the scale and urgency of the problem. The collective response to coronavirus is the result of a broadly shared agreement on what companies are expected to do in the crisis that has emerged in almost every affected nation. Remarkably, companies are behaving differently even in the absence of legal reforms – laws on corporate purpose and directors’ duties are the same today as they were at the outset of the crisis.

Company founders and managers are a diverse group, and so are their preferences. Some may have serious concerns about global challenges facing humanity, such as inequality—whether of income, gender, race, or opportunities—or climate risks. But even these businesses may struggle in behaving responsibly because of concerns about becoming uncompetitive against less enlightened businesses. The classic collective action problem forces would-be responsible businesses to make the rational decision of ignoring inequality and environmental problems.

Where market failures like this are strong, the usual response is government intervention, for example, through the adoption of stricter employment protections or environmental standards. The reaction to the virus shows the power of a decentralized solution to the problem through collective social backlash. By increasing the costs of ignorant behaviour, broad society consensus promotes responsible business practices across markets and nations.

Second, businesses need clear guidelines as to what practical steps they are expected to take to meet the common goal. Governments have been clear about their expectations from businesses during the COVID-19 crisis by recommendations to preserve employment, cut dividends and share buybacks, and lower rents by property owners. Similarly, society in general has been sending clear signals about the expected behaviour by approving some actions taken by companies and showing discontent over undesired conduct in the form of widespread backlash.

For example, when Johnson & Johnson, a medical company, announced plans to invest US $1bn in developing a COVID-19 vaccine, the company’s shares jumped despite the not-for-profit nature of the project. By contrast, the decision by Sports Direct to keep shops open as essential or the decision by Adidas to skip rental payments on its stores led to public outcry and calls to boycott products in tabloid and social media. Similarly, the reluctance by the UK’s largest banks and German carmakers to cut dividends raised many eyebrows. Not only were some of these companies forced to apologize and reverse course, but their reputations were damaged too. Widely shared public reaction can thus send a clear message to all other businesses what to do and how not to behave.

Third, developing consensus over global challenges requires international cooperation. The exceptional scale of the current crisis coupled with the fear that governments responding to the crisis differently to others will face fierce questions explains why, even in the absence of coordination, all nations individually have acted similarly. But countries are likely to be affected differently, at least in the short run, on many other important matters. For example, the degree of underlying inequality varies across countries and some countries experience more acute climate-related risks, like forest fires or rising sea levels, than other nations. This means that atomistic development of consensus through peer pressure, unlike in the case of COVID-19, is highly unlikely. Local action, meanwhile, cannot offer meaningful solutions because markets are still global and responsible governments and businesses will not be able to compete if others do not act similarly.

To sum up, if we want businesses to act responsibly, we need to deliver a clear message by developing consensus over global challenges and communicating it clearly to businesses as one shared global voice. We also need to set out what practical steps businesses need to take to achieve the common goal – whether through government nudges or endorsements in social and news media. Where threats affect nations differently, this can be achieved only through cooperation on a global scale. Given the rise of national sovereign interests and national governments, we are facing a huge task in developing broad consensus on matters that are important. The arrival of responsible capitalism may thus take time. For now, until this consensus is formed, blame us and our elected governments, not businesses, for the failures of capitalism.

It has become fashionable in these troubled times to write about how the coronavirus (or Covid-19) situation shows that the writer’s favourite policies are the best ones. Trite as it may be, I don’t want to miss the opportunity to explain and defend shareholder primacy as a theory / principle followed in corporate law.

Do companies have an ethical obligation to take care of employees during the coronavirus pandemic? If not, why are companies asking employees to work from home and even paying employees when they are not coming in to work? Even companies in the gig economy like Uber are stepping up and offering unexpected support to their drivers whom they have refused to consider as employees. For instance, Uber announced that it would offer 14 days of financial assistance to drivers affected by Covid-19. Similarly, to accommodate the demand from workplaces and educational institutions to switch to working online, tech companies like Google, Microsoft, and Zoom have begun offering some of their products’ features for free. Why are they going well beyond what current laws require them to do?

Have they begun to embrace stakeholderism (the idea that companies should service all stakeholders equally) and, if so, can we expect such continued benefits being offered to employees in need even after the pandemic has passed? I’d answer both parts of this question in the negative. In my view, these companies are guided by shareholder primacy (the idea that shareholder interests have primacy over that of other stakeholders).

The first and most obvious reason is that shareholders would want directors of the company they have invested in to step up to the occasion when a crisis as big as a pandemic is staring us in the face. While it is normally assumed that shareholder interests translate into profit-making or wealth maximization, intelligent directors would understand that a crisis calls for a different understanding of what shareholders want. The second possible reason for companies to act in the interests of stakeholders at this time is to enhance their reputation. A company making accommodations during a time of crisis might forego some profits in the short-term but will have reputational gains in the long term. The consideration of reputational incentives is not to suggest that companies acting altruistically should be seen as cynical. On the contrary, it is laudable that the directors of these companies have acted in the interests of the company by taking care of relevant stakeholders when it was most needed. The fact that company reputation was one of the variables in the calculus should be noted positively because that shows that shareholder primacy ensures companies act in the interests of other stakeholders when it is most essential. A third reason is that by offering benefits to employees (or independent contractors as in the case of Uber’s drivers) or customers as in the case of the tech companies, the companies have ensured that the relevant stakeholders (customers and employees / independent contractors) would want to work or continue to work with these companies.

If shareholder primacy leads to beneficial outcomes, why is it so reviled? Shareholder primacy is often confused with a myopic focus on short-term profits. To be sure, the company law of most countries requires directors to act in the best interests of the company and, in determining which interests within the company are to be prioritised, to give primacy to that of shareholders. The default assumption is that most shareholders would want to maximise the wealth that they have invested in the company. However, it is left to directors to consider other relevant interests where they are in the best interests of the company. As I have argued above, it was clearly in the interests of the company to prioritise various stakeholders’ interests and act accordingly, and in this instance they have acted accordingly. Not every situation has such an easy answer and so it is left to directors to choose the course of action best suited to the company, with the interests of shareholders being ultimately prioritised.

What happens after the pandemic has passed? While the coronavirus situation is a big crisis and companies have been stepping up, decisions prioritising the interests of one stakeholder over those of others are routine, even in calmer situations, or where a company alone is facing a crisis of some sort. Take for example, employees’ complaints about toxic work culture and harassment, which we now know was the case with Uber in the past. Often the response is to keep the issue under wraps or refuse to address the particular stakeholder’s needs. This unsavoury behaviour cannot however be attributed to either shareholder primacy or stakeholderism. We would expect that shareholders would want companies to clean their house as soon as they know there is trouble so that they are not at the receiving end of the law suit at a later date and, more importantly, because shareholders would want talented employees to be retained within the company. Unfortunately, the unsavoury behaviour is simply an expression of human nature in some cases and better incentives to prevent such behaviour need to be devised. Similarly, for concerns of other stakeholders, the environment for instance, environment protection and climate change laws would constrain directors’ actions rather than relying on principles of either shareholder primacy or stakeholderism to do the job.

All this is to say that there are problems with how companies are run and we need innovative solutions to create better incentives rather than falling back on paying lip service to stakeholderism as the Business Roundtable recently did in its 2019 statement.

Cette discussion aborde les principaux défis auxquels sont confrontés les chefs d’entreprise canadiens à l’approche de la phase de réouverture :

se concentrer sur les véritables enjeux;

veiller à la gestion immédiate des crises et à la préparation du conseil d’administration;

repenser la stratégie et la gestion des risques;

repenser les cadres incitatifs; et

repenser l’objectif de l’entreprise.

Comme en conclut l’article, cette crise redéfinira une grande partie de ce que nous considérons comme étant de la « bonne gouvernance ». Les conseils d’administration, en particulier, doivent élargir leurs missions pour s’assurer que leurs entreprises sont préparées à la nouvelle réalité qui les attend.