parties prenantes

actualités canadiennes Gouvernance Nouvelles diverses parties prenantes

Raison d’être et gouvernance : un couple

Ivan Tchotourian 29 avril 2021 Ivan Tchotourian

Pas de raison d’être sans gouvernance ! clament André Coupet et Marie-France Veilleux (Gestion, 21 avril 2021). Cet articles est intéressant car il fait le lien entre la raison d’être et la gouvernance et montre que la gouvernance doit évoluer si la raison d’être ne veut pas être de façade.

Extrait :

(…) Il existe une troisième implication sous-jacente aux deux premières. Elle implique la gouvernance de l’entreprise. Celle-ci est l’élément central qui fait que l’exercice de se donner une raison d’être devient une réussite. C’est la gouvernance de l’entreprise qui doit déployer la nouvelle stratégie et qui doit piloter la mise en œuvre effective de cette raison d’être et des engagements stratégiques qui en découlent.

Le moteur de la raison d’être

La gouvernance est trop souvent comprise sous l’angle de la conformité aux réglementations et aux institutions. Or, il s’agit plutôt de l’art de diriger et de prendre des décisions, dans le respect des règles ou des statuts de l’organisation, tout en ayant en tête l’horizon des décisions. Les choix à court terme ne doivent pas aller à l’encontre de la pérennité de l’organisation.

Pour construire une raison d’être et s’assurer que celle-ci soit transformative, la gouvernance doit être forte. Elle doit être capable de réorienter l’entreprise et d’assumer les engagements, par exemple en lançant de nouveaux produits et services conformes à la raison d’être, ou en abandonnant, s’il le faut, une partie du chiffre d’affaires jugé trop émetteur de CO².

La gouvernance doit être ouverte :

À la consultation effective des parties prenantes : cette consultation, qui servivra à la définition de la raison d’être de l’organisation, doit retenir aussi bien les critiques à l’égard de l’entreprise que les besoins, les attentes et les suggestions pour bâtir les différentes propositions de valeur.

Au partage de la prise de décision par de nouveaux acteurs : habituellement moins présents autour des tables de décision. Un conseil diversifié à tous niveaux démontre l’acceptation d’une autre façon de penser. Pensons à la nomination d’administrateurs salariés au sein des conseils d’administration (CA). Aujourd’hui, le succès d’une organisation est davantage basé sur le talent que sur le capital. Les actionnaires ne sont donc plus les seuls détenteurs du savoir. Le capitalisme des parties prenantes, perspective évoquée notamment au dernier forum de Davos2, ne sera une réalité que lorsque les CA, lieux de pouvoir par excellence, s’ouvriront aux parties prenantes, soit directement, soit, à minima, en tenant compte des avis d’un comité des parties prenantes

À l’ajustement des valeurs de l’organisation : le respect, la solidarité ou la générosité sont des guides indispensables qui permettent à l’entreprise de s’adresser à des problématiques de pauvreté, d’éducation, d’isolement, etc.

Une boussole entre les mains du CA

Si la raison d’être de l’entreprise est comprise comme étant non seulement le but de l’organisation, mais aussi la boussole de l’entreprise qui donne quotidiennement la route à suivre, alors il est clair que le gardien de la raison d’être est le CA. Son nouveau rôle vient conforter le premier, soit celui de gardien de la pérennité de l’organisation.

Axé sur le long terme, le CA doit s’impliquer totalement, tant dans l’exercice de la définition de la raison d’être que dans celui du plan stratégique. Il doit choisir et décider. L’équipe de direction doit opérationnaliser les choix, ce qui est tout un défi d’agilité et de résilience.

Cette vision d’un CA compétent et impliqué, centrée sur la raison d’être et la stratégie, débouche logiquement sur une séparation des pouvoirs entre la présidence du conseil et la direction générale. Cela semble d’ailleurs devenir la règle. En effet, près de 60% des entreprises américaines inscrites et cotées à l’indice Standard and Poor’s appliquent cette séparation des pouvoirs.

Les deux instances se complètent en termes d’horizon. Le CA n’a clairement pas à s’immiscer dans la gestion quotidienne. Son rôle «n’est pas de gérer, mais bien de formuler une vision de l’avenir», selon Michel Nadeau, cofondateur de l’Institut sur la gouvernance d’organisations publiques et privées.

À la prochaine…

Gouvernance Nouvelles diverses parties prenantes Responsabilité sociale des entreprises

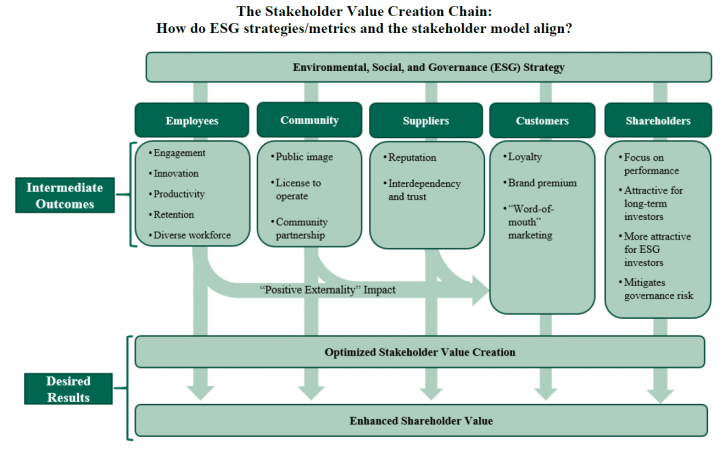

The Stakeholder Model and ESG

Ivan Tchotourian 17 septembre 2020 Ivan Tchotourian

Intéressant article sur l’Harvard Law School Forum on Corporate Governance consacré au modèle partie prenante et à ses liens avec les critères ESG : « The Stakeholder Model and ESG » (Ira Kay, Chris Brindisi et Blaine Martin, 14 septembre 2020).

Extrait :

Is your company ready to set or disclose ESG incentive goals?

ESG incentive metrics are like any other incentive metric: they should support and reinforce strategy rather than lead it. Companies considering ESG incentive metrics should align planning with the company’s social responsibility and environmental strategies, reporting, and goals. Another essential factor in determining readiness is the measurability/quantification of the specific ESG issue.

Companies will generally fall along a spectrum of readiness to consider adopting and disclosing ESG incentive metrics and goals:

- Companies Ready to Set Quantitative ESG Goals: Companies with robust environmental, sustainability, and/or social responsibility strategies including quantifiable metrics and goals (e.g., carbon reduction goals, net zero carbon emissions commitments, Diversity and Inclusion metrics, employee and environmental safety metrics, customer satisfaction, etc.).

- Companies Ready to Set Qualitative Goals: Companies with evolving formalized tracking and reporting but for which ESG matters have been identified as important factors to customers, employees, or other These companies likely already have plans or goals around ESG factors (e.g., LEED [Leadership in Energy and Environmental Design]-certified office space, Diversity and Inclusion initiatives, renewable power and emissions goals, etc.).

- Companies Developing an ESG Strategy: Some companies are at an early stage of developing overall ESG/stakeholder strategies. These companies may be best served to focus on developing a strategy for environmental and social impact before considering linking incentive pay to these priorities.

We note it is critically important that these ESG/stakeholder metrics and goals be chosen and set with rigor in the same manner as financial metrics to ensure that the attainment of the ESG goals will enhance stakeholder value and not serve simply as “window dressing” or “greenwashing.” [9] Implementing ESG metrics is a company-specific design process. For example, some companies may choose to implement qualitative ESG incentive goals even if they have rigorous ESG factor data and reporting.

Will ESG metrics and goals contribute to the company’s value-creation?

The business case for using ESG incentive metrics is to provide line-of-sight for the management team to drive the implementation of initiatives that create significant differentiated value for the company or align with current or emerging stakeholder expectations. Companies must first assess which metrics or initiatives will most benefit the company’s business and for which stakeholders. They must also develop challenging goals for these metrics to increase the likelihood of overall value creation. For example:

- Employees: Are employees and the competitive talent market driving the need for differentiated environmental or social initiatives? Will initiatives related to overall company sustainability (building sustainability, renewable energy use, net zero carbon emissions) contribute to the company being a “best in class” employer? Diversity and inclusion and pay equity initiatives have company and social benefits, such as ensuring fair and equitable opportunities to participate and thrive in the corporate system.

- Customers: Are customer preferences driving the need to differentiate on sustainable supply chains, social justice initiatives, and/or the product/company’s environmental footprint?

- Long-Term Sustainability: Are long-term macro environmental factors (carbon emissions, carbon intensity of product, etc.) critical to the Company’s ability to operate in the long term?

- Brand Image: Does a company want to be viewed by all constituencies, including those with no direct economic linkage, as a positive social and economic contributor to society?

There is no one-size-fits-all approach to ESG metrics, and companies fall across a spectrum of needs and drivers that affect the type of ESG factors that are relevant to short- and long-term business value depending on scale, industry, and stakeholder drivers. Most companies have addressed, or will need to address, how to implement ESG/stakeholder considerations in their operating strategy.

Conceptual Design Parameters for Structuring Incentive Goals

For those companies moving to implement stakeholder/ESG incentive goals for the first time, the design parameters range widely, which is not different than the design process for implementing any incentive metric. For these companies, considering the following questions can help move the prospect of an ESG incentive metric from an idea to a tangible goal with the potential to create value for the company:

- Quantitative goals versus qualitative milestones. The availability and quality of data from sustainability or social responsibility reports will generally determine whether a company can set a defined quantitative goal. For other companies, lack of available ESG data/goals or the company’s specific pay philosophy may mean ESG initiatives are best measured by setting annual milestones tailored to selected goals.

- Selecting metrics aligned with value creation. Unlike financial metrics, for which robust statistical analyses can help guide the metric selection process (e.g., financial correlation analysis), the link between ESG metrics and company value creation is more nuanced and significantly impacted by industry, operating model, customer and employee perceptions and preferences, etc. Given this, companies should generally apply a principles-based approach to assess the most appropriate metrics for the company as a whole (e.g., assessing significance to the organization, measurability, achievability, etc.) Appendix 1 provides a list of common ESG metrics with illustrative mapping to typical stakeholder impact.

- Determining employee participation. Generally, stakeholder/ESG-focused metrics would be implemented for officer/executive level roles, as this is the employee group that sets company-wide policy impacting the achievement of quantitative ESG goals or qualitative milestones. Alternatively, some companies may choose to implement firm-wide ESG incentive metrics to reinforce the positive employee engagement benefits of the company’s ESG strategy or to drive a whole-team approach to achieving goals.

- Determining the range of metric weightings for stakeholder/ESG goals. Historically, US companies with existing environmental, employee safety, and customer service goals as well as other stakeholder metrics have been concentrated in the extractive, industrial, and utility industries; metric weightings on these goals have ranged from 5% to 20% of annual incentive scorecards. We expect that this weighting range would continue to apply, with the remaining 80%+ of annual incentive weighting focused on financial metrics. Further, we expect that proxy advisors and shareholders may react adversely to non-financial metrics weighted more than 10% to 20% of annual incentive scorecards.

- Considering whether to implement stakeholder/ESG goals in annual versus long-term incentive plans. As noted above, most ESG incentive goals to date have been implemented as weighted metrics in balanced scorecard annual incentive plans for several reasons. However, we have observed increased discussion of whether some goals (particularly greenhouse gas emission goals) may be better suited to long-term incentives. [10] There is no right answer to this question—some milestone and quantitative goals are best set on an annual basis given emerging industry, technology, and company developments; other companies may have a robust long-term plan for which longer-term incentives are a better fit.

- Considering how to operationalize ESG metrics into long-term plans. For companies determining that sustainability or social responsibility goals fit best into the framework of a long-term incentive, those companies will need to consider which vehicles are best to incentivize achievement of strategically important ESG goals. While companies may choose to dedicate a portion of a 3-year performance share unit plan to an ESG metric (e.g., weighting a plan 40% relative total shareholder return [TSR], 40% revenue growth, and 20% greenhouse gas reduction), there may be concerns for shareholders and/or participants in diluting the financial and shareholder-value focus of these incentives. As an alternative, companies could grant performance restricted stock units, vesting at the end of a period of time (e.g., 3 or 4 years) contingent upon achievement of a long-term, rigorous ESG performance milestone. This approach would not “dilute” the percentage of relative TSR and financial-based long-term incentives, which will remain important to shareholders and proxy advisors.

Conclusion

As priorities of stakeholders continue to evolve, and addressing these becomes a strategic imperative, companies may look to include some stakeholder metrics in their compensation programs to emphasize these priorities. As companies and Compensation Committees discuss stakeholder and ESG-focused incentive metrics, each organization must consider its unique industry environment, business model, and cultural context. We interpret the BRT’s updated statement of business purpose as a more nuanced perspective on how to create value for all stakeholders, inclusive of shareholders. While optimizing profits will remain the business purpose of corporations, the BRT’s statement provides support for prioritizing the needs of all stakeholders in driving long-term, sustainable success for the business. For some companies, implementing incentive metrics aligned with this broader context can be an important tool to drive these efforts in both the short and long term. That said, appropriate timing, design, and communication will be critical to ensure effective implementation.

À la prochaine…

Gouvernance Nouvelles diverses parties prenantes

Hiérarchiser les parties prenantes : comment ?

Ivan Tchotourian 14 juillet 2020 Ivan Tchotourian

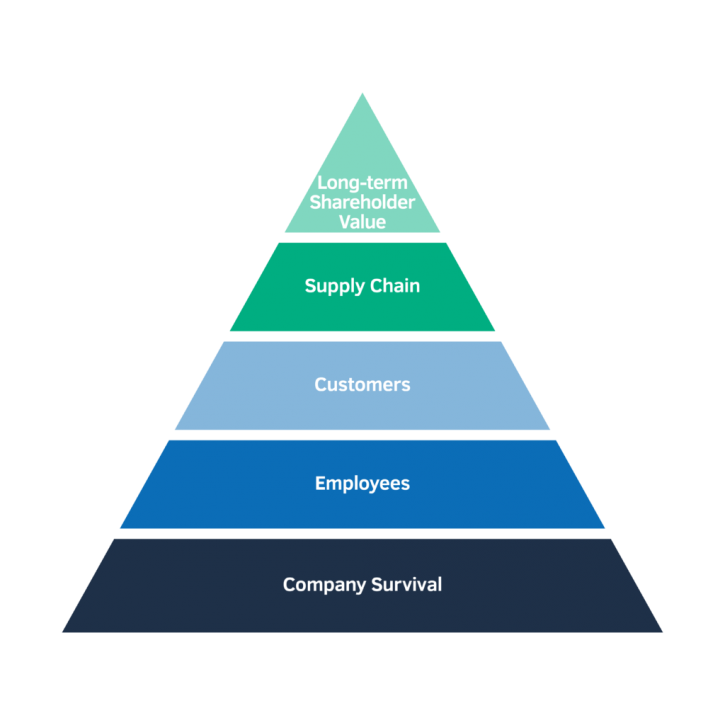

Dans l’Harvard Law School Forum on Corporate Governance, un article intéressant – et court – apporte un bel éclairage sur la gestion des parties prenantes : « A Hierarchy of Stakeholder Needs » (de Sarah Keohane Williamson, FCLTGlobal, 22 juin 2020).

Extrait :

Amid the extraordinary circumstances and economic difficulties brought on by COVID-19, companies in 2020 are faced with decisions on how to best serve the many stakeholders that rely on them—customers, investors, suppliers, employees, and so on. Each group has its own distinct needs and contributions to the company’s overall success, and companies recognize that these groups build on each other to serve their purpose.

(…) Survival for the company itself represents the basic need of the hierarchy. A company’s first priority has to be ensuring it is resilient (and liquid) enough to outlast the crisis. If this need is not met, there are no employees, customers, or other stakeholders to serve. Hard decisions may have to be made to ensure the long-term survival of the enterprise that will affect other tiers of needs—closing stores, furloughing employees, or postponing dividends to investors. Once the basic need is met, however, and the company is a going concern, the company can reorient its focus.

Employees look to their employer for security in more ways than one—financial, to be sure, but also physical. Many companies addressed this area first in its response to COVID-19—89% of respondents to a recent FCLTGlobal survey indicated that employee health and safety was its top priority. (…)

Once the house is in order, customers’ needs can follow. Just as customers depend on a company’s products, the company relies on a consistent, repeatable client base to stay in operation. Like before, this tier is dependent on the one that precedes it—if there were no company, or no employees to keep it running, there would be no customers to serve.

(…) Once customers’ needs are met and business can continue, the supply chain must be maintained. COVID-19 has presented a real challenge in terms of supply for many companies, particularly when sourcing products from countries that are in strict lockdowns.

(…) Then, finally, the company is able to achieve long-term value for its shareholders. Meeting the preceding needs—viability through liquidity, employee wellbeing, extraordinary customer care, and supply chain continuity—may have resulted in near-term shortfalls for shareholders by way of lower earnings or a temporary pause in issuing dividends.

À la prochaine…

engagement et activisme actionnarial Gouvernance Normes d'encadrement Nouvelles diverses objectifs de l'entreprise parties prenantes Responsabilité sociale des entreprises

Les investisseurs institutionnels réclament de la responsabilité !

Ivan Tchotourian 6 avril 2020 Ivan Tchotourian

L’ICCR (Interfaith Center on Corporate Responsibility) américain vient de prendre une position intéressante dans le contexte de la pandémie de Coronavirus : elle exhorte les entreprises à plus de responsabilité et fait connaître ses 5 priorités. Preuve une fois de plus que l’engagement des investisseurs institutionnels en faveur de la RSE est présent !

Global institutional investors comprising public pensions, asset management firms and faith-based funds issued a Statement on Coronavirus Response calling on the business community to step up as corporate citizens, and recommending measures corporations can take to protect their workforces, their communities, their businesses and our markets as a whole while we all confront the Coronavirus crisis.

Extrait :

1. Provide paid leave: We urge companiesto make emergency paid leave available to all employees, including temporary, part time, and subcontracted workers. Without paid leave, social distancing and self-isolation are not broadly possible.

2. Prioritize health and safety: Protecting worker and public safety is essential for maintaining business reputations, consumer confidence and the social license to operate, as well as staying operational. Workers should avoid or limit exposure to COVID-19 as much as possible. Potential measures include rotating shifts; remote work; enhanced protections, trainings or cleaning; adopting the occupational safety and health guidance, and closing locations, if necessary.

3. Maintain employment: We support companies taking every measure to retain workers as widespread unemployment will only exacerbate the current crisis. Retaining a well-trained and committed workforce will permit companies to resume operations as quickly as possible once the crisis is resolved. Companies considering layoffs should also be mindful of potential discriminatory impact and the risk for subsequent employment discrimination cases.

4. Maintain supplier/customer relationships: As much as possible, maintaining timely or prompt payments to suppliers and working with customers facing financial challenges will help to stabilize the economy, protect our communities and small businesses and ensure a stable supply chain is in place for business operations to resume normally in the future.

5. Financial prudence: During this period of market stress, we expect the highest level of ethical financial management and responsibility. As responsible investors, we recognize this may include companies’ suspending share buybacks and showing support for the predicaments of their constituencies by limiting executive and senior management compensation for the duration of this crisis.

À la prochaine…

actualités internationales Gouvernance Normes d'encadrement Nouvelles diverses parties prenantes Responsabilité sociale des entreprises

Le Forum économique mondial envoie un message

Ivan Tchotourian 4 avril 2020 Ivan Tchotourian

En ce début d’avril 2020, le Forum Économique Mondial vient de publier une déclaration sur les principes parties prenantes qu’il entend promouvoir durant la crise du COVID-19 : « Stakeholder Principles in the COVID Era ».

Extrait :

To this end, we endorse the following Stakeholder Principles in the COVID Era:

− To employees, our principle is to keep you safe: We will continue do everything we can to protect your workplace, and to help you to adapt to the new working conditions

− To our ecosystem of suppliers and customers, our principle is to secure our shared business continuity: We will continue to work to keep supply chains open and integrate you into our business response

− To our end consumers, our principle is to maintain fair prices and commercial terms for essential supplies

− To governments and society, our principle is to offer our full support: We stand ready and will continue to complement public action with our resources, capabilities and know-how

− To our shareholders, our principle remains the long-term viability of the company and its potential to create sustained value

Finally, we also maintain the principle that we must continue our sustainability efforts unabated, to bring our world closer to achieving shared goals, including the Paris climate agreement and the United Nations Sustainable Development Agenda. We will continue to focus on those long-term goals.

À la prochaine…

Gouvernance Nouvelles diverses parties prenantes Responsabilité sociale des entreprises

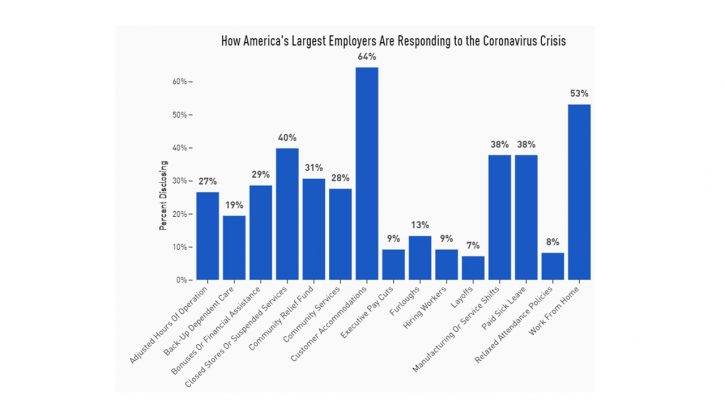

COVID-19 : comment les entreprises américaines traitent leurs parties prenantes ?

Ivan Tchotourian 31 mars 2020 Ivan Tchotourian

Pour en savoir plus, je vous invite à lire cet article : « The COVID-19 Corporate Response Tracker: How America’s Largest Employers Are Treating Stakeholders Amid the Coronavirus Crisis ». Au travers une méthodologie, Just Capital recense les décisions prises par les grandes entreprises américaines pour identifier leur réponse à la crise…

Je vous invite à regarder l’image ci-dessus qui est plus parlante que des mots !

Résumé :

The coronavirus pandemic and impending recession have created an urgent, unprecedented opportunity for CEOs and corporate leaders to put the promise of purpose-driven leadership and stakeholder capitalism into practice. Companies face extraordinary operational and financial challenges, and with every industry and business tested in unique ways, the course of action may be different for each. Many companies have already stepped up to support their workers, customers, and local communities. We’ve created the following tracker — starting with America’s 100 largest public employers — to help assess what’s happening on the ground, elevate best practices, and share what good looks like in this rapidly shifting landscape.

À la prochaine…

actualités internationales Gouvernance Nouvelles diverses parties prenantes Responsabilité sociale des entreprises Valeur actionnariale vs. sociétale

GM : gouvernance actionnariale v. salariés

Ivan Tchotourian 24 septembre 2019 Ivan Tchotourian

L’auteur américain Robert Reich a pris sa plume pour dénoncer la situation de GM et le fait que les actionnaires sont encore les victimes d’une gouvernance critiquable : « Robert B. Reich: GM is the story of the American worker » (The Baltimore Sun, 23 septembre 2019). Une belle réflexion que je vous fait connaître ici.

Extrait :

When GM went public again in 2010, it boasted to Wall Street that 43 percent of its cars were made outside the United States in places where labor cost less than $15 an hour, while in America it could now pay « lower-tiered » wages and benefits for new employees.

The corporation came roaring back. Over the last three years it’s made $35 billion in North America.

But its workers are still getting measly pay packages, and GM is still outsourcing like mad.

Last year it assigned its new Chevrolet Blazer, a sport utility vehicle that had been made in the United States, to a Mexican plant, while announcing it would lay off 18,000 American workers.

Earlier this year it shut its giant plant in Lordstown, Ohio, which Donald Trump had vowed to save. « Don’t move. Don’t sell your house, » he said at a rally in Youngstown, Ohio, in 2017.

GM is still getting corporate welfare — since Trump took office, some $600 million in federal contracts and $700 million in tax breaks (including Trump’s giant corporate tax cut).

Some of this largesse has gone into the pockets of GM executives. Chairman and CEO Mary Barra raked in almost $22 million in total compensation last year.

Last month, the Business Roundtable — a confab of American CEOs, on whose executive committee Barra sits — pledged to compensate all employees « fairly » and provide them « important benefits. »

Why should anyone believe them? For 40 years these CEOs have fought unions, outsourced jobs abroad, loaded up on labor-replacing technologies without retraining their workers, and abandoned their communities when they could do things more cheaply elsewhere.

Amazon CEO Jeff Bezos signed the same statement. Last week, Amazon-owned Whole Foods announced it would be cutting medical benefits for its entire part-time workforce — at a total savings of about what Bezos makes in two hours.

Corporate profits have reached record levels, but nothing has trickled down to most workers.

Profits now constitute a larger portion of national income, and wages a lower portion, than at any time since World War II. These profits are generating higher share prices (fueled by share buybacks) and higher executive pay, resulting in wider inequality. The richest 1 percent of Americans own about 40 percent of all shares of stock; the richest 10 percent, around 80 percent.

The demise of unions explains much of this. In the mid-1950s, over a third of all workers in the private sector were unionized. This gave them substantial bargaining power to get higher wages and benefits.

Today, just 6.4 percent of private-sector workers are unionized, eliminating most of that bargaining power. Researchers have found that between 1952 and 1988, almost all of the rise in share values came as a result of economic growth, but from 1989 to 2017, economic growth accounted for just 24 percent of the rise. Most of the increase has come from money that otherwise would have gone to workers.

America’s shift from farm to factory was accompanied by decades of bloody labor conflict. The subsequent shift from factory to office and other service jobs created further social upheaval.

The more recent power shift from workers to shareholders — and consequentially, the dramatic widening of inequality — has happened far more quietly, but it has had a more unfortunate and more lasting consequence for the system: stagnant wages, abandoned communities and an angry working class vulnerable to demagogues peddling authoritarianism, racism and xenophobia.

Donald Trump didn’t come from nowhere, but he’s a fake champion of the working class. If he were the real thing, he’d be walking the picket line with GM workers.

À la prochaine…