Archives

objectifs de l'entreprise Structures juridiques Valeur actionnariale vs. sociétale

Des entreprises progressistes… vraiment ?

Ivan Tchotourian 27 juin 2016

« Faire de l’entreprise un bien commun » ? 18% des dirigeants d’entreprise annoncent aujourd’hui cet objectif comme prioritaire, selon le récent sondage réalisé par Opinion Way pour l’association Entreprise et Progrès et Generali * sur le thème « Les entreprises françaises sont-elles progressistes ? ».

L’enquête qui se penche sur l’évolution de l’implication des chefs d’entreprise en matière de RSE met aussi en relief un décalage entre deux perceptions : quand 89% des dirigeants estiment devoir placer l’impact sociétal de leur activité au même plan que la performance économique, les Français interrogés jugent _ quasiment dans les mêmes proportions (81%) _ que l’entreprise… reste uniquement tournée vers la rentabilité.

Pour celles et ceux que le mouvement progressistes intéressent, plusieurs juristes de renom s’y intéressent :

- Claude Champaud, dir, L’entreprise dans la société du 21e siècle, Bruxelles, Larcier, 2013; Claude Champaud, Manifeste pour la doctrine de l’entreprise : Sortir de la crise du financialisme, Bruxelles, Larcier, 2011.

- Isabelle Corbisier, « L’entreprise : Quelles sont ses valeurs fondatrices et ses finalités ? » dans Nicolas Thirion, dir, Crise et droit économique, Bruxelles, Larcier, 2014, 175 et aussi Isabelle Corbisier, La société : contrat ou institution ? Droits étatsuniens, français, belge, néerlandais, allemand et luxembourgeois, Bruxelles, Larcier, 2011.

- Simon Deakin, « The Juridical Nature of the Firm » dans Thomas Clarke et Douglas Branson, dir, The SAGE Handbook of Corporate Governance, Londres, SAGE, 2012, 113.

- Kent Greenfield, « Saving the World With Corporate Law » (2008) 57 Emory LJ 947; Kent Greenfield, « New Principles for Corporate Law » (2005) 1 Hastings Bus LJ 87.

- Andrew R Keay, The Corporate Objective: Corporations, Globalisation and the Law, Cheltenham, Edward Elgar, 2013.

- Catherine Malecki, Responsabilité sociale des entreprises : Perspectives de la gouvernance d’entreprise durable, Paris, LGDJ, 2014.

- David K Millon, « Why Is Corporate Management Obsessed with Quarterly Earnings and What Should be Done About It? » (2002) 70 Geo Wash L Rev. 890; David K Millon, « New Directions in Corporate Law: Communitarians, Contractarians, and Theorisis in Corporate Law » (1993) 50 Wash. & Lee L Rev 1373 ; David K Millon, « Redefining Corporate Law » (1991) 24 Ind L Rev 233; David K Millon, « Theories of the Corporation » (1990) 39 Duke LJ 201.

- Lawrence E Mitchell, Corporate Irresponsibility: America’s Newest Export, New Haven, Yale University Press, 2001 ; Lawrence E Mitchell, dir, Progressive Corporate Law, Boulder, Westview Press, 1995.

- Beate Sjåfjell et Benjamin Richardson, Company Law and Sustainability: Legal Barriers and Opportunities, New York, Cambridge University Press, 2015 et Beate Sjåfjell, Towards A Sustainable EU Company Law: A Normative Analysis of the Objectives of EU Law, with the Takeover Directive as a Test Case, European Company Law Series, Kluwer Law International, 2009.

- Lynn A Stout, The Shareholder Value Myth, San Francisco, Berrett-Koehler, 2012 ; Lynn A Stout, « Why We Should Stop Teaching Dodge v. Ford » (2008) 3:1 Va L & Bus Rev 163 ; Lynn A Stout, « Takeovers in the Ivory Tower: How Academics Are Learning Martin Lipton May be Right » (2005) 60 Bus Lawyer 1435 ; Lynn A Stout, « Share price as a Poor Criterion for Good Corporate Law » (2005) UCLA School of Law Document de travail No 05-7, en ligne: <http://papers.ssrn.com/abstract=660622> ; Lynn A Stout, « Bad and Not-So-Bad Arguments for Shareholder Primacy » (2002) 75:5 S Cal L Rev 1189.

- Alain Supiot, La gouvernance par les nombres, Paris, Éditions Fayard, 2015 ; Alain Supiot, dir, L’entreprise dans un monde sans frontières – Perspectives économiques et juridiques, Collection les sens du droit, Paris, Éditions Dalloz, 2015.

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial

Une vision positive des actionnaires activistes

Ivan Tchotourian 26 juin 2016

Bonjour à toutes et à tous, Mme Saliha Bardasi propose une réflexion intéressante sur les actionnaires activistes dans un article paru dans La Tribune : « L’actionnaire activiste, capitaliste impatient, mais contre-pouvoir intéressant ». Comme elle l’écrit, « les actionnaires dits activistes sont très souvent contestés. Mais leur rôle peut être utile, dans des sociétés à la gouvernance défaillante ».

Selon une récente étude, la disruption symbolise aujourd’hui les menaces auxquelles les entreprises classiques doivent faire face. Si la disruption numérique est l’exemple immédiat, le champ juridique n’est pas épargné : les actionnaires activistes « nouvelle génération », qui inquiètent déjà les dirigeants et conseils d’administration outre-Atlantique, arrivent en Europe et en France.

L’actionnaire activiste est l’outsider qui agit à rebours des pratiques de gouvernance établies. Bien que propriétaire d’une participation minoritaire, il défend ses intérêts de manière active, en assemblée générale ou directement auprès des dirigeants de l’entreprise, et si nécessaire via des campagnes publiques de communication. Cette vigilance dynamique a nourri une réputation inquiétante. Ces ultras du profit actionnarial seraient prêts à tout pour le maximiser : distribution de dividendes, rachat d’actions, mais surtout dépeçage des entreprises, licenciements massifs…

Pour rappel, je m’étais exprimé sur ce thème dans un billet publié sur Contact au printemps 2015 : « La loi Florange et l’activisme des actionnaires ».

L’activisme des investisseurs institutionnels fait l’actualité au Canada et en Europe, mais aussi –et surtout– aux États-Unis. Plusieurs grandes entreprises cotées en bourse ont en effet subi les attaques d’actionnaires dits activistes. Les Darden, DuPont, PepsiCo pour les États-Unis et Accor ou Péchiney, en France, en sont les exemples les plus éclairants. Au Canada, plusieurs fonds spéculatifs ont fait la manchette pour leur activisme. Qu’il suffise de citer la décision de Pershing Square Capital Management de faire pression sur le Canadien Pacifique afin de faire élire sa liste de candidats au conseil d’administration ou la campagne menée par JANA Partners pour obtenir des modifications dans la composition du conseil de l’entreprise Agrium Inc.. Or, à cette même période, en 2014, la France adoptait une loi innovante dite «loi Florange». Après avoir consacré quelques lignes sur les actionnaires activistes et leurs objectifs parfois critiquables, je reviendrai sur cette réforme française qui vient de fêter sa 1re année d’existence ainsi que sur le signal qu’elle a envoyé.

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial mission et composition du conseil d'administration

Critique sur la pratique du staggered board dans les comités d’audit

Ivan Tchotourian 26 juin 2016

AccountingWeb (par Terri Sheridan, 24 juin 2016) relaie un excellent article : « Staggered Boards Impede Improvements to Audit Committees ». Cet article revient sur la pratique des stagerred board et l’effet négatif qu’elle induit sur les comités d’audit en termes de performance et d’amélioration.

The Efficacy of Shareholder Voting in Staggered and Non-Staggered Boards: The Case of Audit Committee Elections, published in the May/July issue of the American Accounting Association’s Auditing: A Journal of Practice & Theory, indicates that staggered boards can interfere with shareholders’ goals and hinder audit committee improvements. In staggered boards, only a third of the directors are up for re-election annually, with members elected to three-year terms.

“Low shareholder approval rates in firms with nonstaggered boards are associated with improvements to audit committee structure, activity, and financial reporting quality,” the study states.

Pour rappel, en vertu du staggered board, un CA est renouvelable par tranches. Au Canada et au Québec, les dispositions 106(3) L.C.S.A. et 110 L.S.A. mentionnent que les administrateurs sont élus pour un mandat n’excédant pas trois ans, sans imposer cependant que les mandats de ces administrateurs aient à être de la même durée. Cette pratique fait l’objet d’une sérieuse remise en question au Canada même si elle se révèle moins utilisée qu’aux États-Unis (CCGG, « Response to OSC Staff Notice 54-701: Regulatory Developments regarding Shareholder Democracy Issues », 31 mars 2011, à la p. 5).

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière Normes d'encadrement

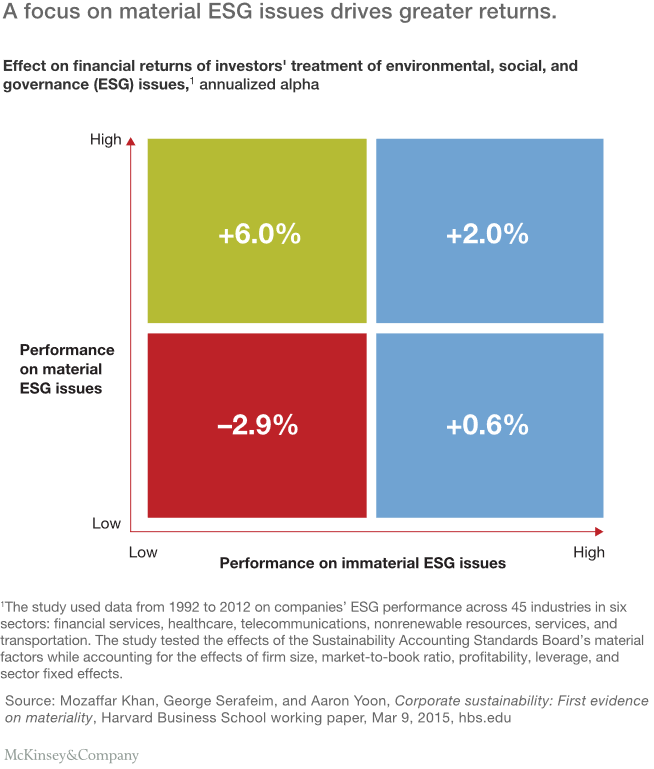

What institutional investors should do next on ESG : un beau rapport !

Ivan Tchotourian 26 juin 2016

C’est sous ce titre que le cabinet McKinsey (sous la plume de Jonathan Bailey, Bryce Klempner et Josh Zoffer) publie un excellent rapport en juin 2016 : « Sustaining sustainability: What institutional investors should do next on ESG ».

Mainstream institutions have made progress integrating environmental, social, and governance factors into their investing, but they still have far to go. Six ideas can take them to the next level.

Voici les 6 étapes énoncées :

- Require uniform corporate ESG-reporting standards based on the principle of materiality

- Build a shared ESG-rating system for external managers

- Work together to engage with corporations

- Stress-test portfolios for ESG risk factors

- Use a long-term ESG outlook to unlock new investment opportunities

- Confront the skepticism and misunderstanding that surround ESG head-on

À la prochaine…

Ivan Tchotourian

Gouvernance normes de droit Structures juridiques

“Enterprise” and Lawyer’s view: By by Irresponsibility and Welcome in a New Area (à télécharger)

Ivan Tchotourian 25 juin 2016

Alors que le colloque du SASE va bientôt avoir lieu à Berkeley aux Etats-Unis, je reviens aujourd’hui sur ce que j’avais présenté au colloque qui s’était tenu en 2014 à Chicago : “Enterprise” and Lawyer’s view: By by Irresponsibility and Welcome in a New Area ».

Accédez au diaporama : PPT SASE 2014 version anglaise

Voici le résumé de cette intervention :

As institutions corporations and enterprises are the basis of capitalism and the subject of great interest for legal studies. Beyond regulation, the inherent nature of corporations raises sensitive legal questions, indeed, since its first appearance in the 18th century. Inspired by economic and financial sciences, legal theories incorporate corporations to contracts (referred to as “aggregate theory”), a private government (referred to as “artificial theory”) and an autonomous entity (“entity theory” or “doctrine de l’entreprise” in Continental Europe). It is indeed argued that incorporating corporations to a simple nexus of contracts has been the subject of great attention since the 1970s, provided that none of the above theories have definitely won unanimity in law, as seen by a comparative reading of the Canadian, American and European jurisprudence. Corporate governance rules clearly demonstrate such incorporation. In its essence, however, the contractual analysis regards the corporation as a means to serving private interests whereby the liability schemes are limited to protecting the supplier of capital. The contractual analysis’s vision is indeed restricted, and it summarizes its goals, to the sought-after maximization of the corporation’s shareholders value. At the heart of the corporation’s issues lies the financial aspect. Within this framework, non-financial concerns appear far away and are dealt with as simple externality that poses management problems. Nonetheless, the corporation’s activities are bearing an economic power that is today seen as ever increasingly significant and its financial and non-financial consequences should be the basis of further thinking. Yet, Canadian law has engaged into this pathway. On the one hand, Canadian corporate law has experienced a profound re-assessment through the Supreme Court of Canada’s decisions in Peoples (2004) and BCE (2008). Far from being a strict contractual reading of the corporation, these decisions have shed light on the importance of different paradigms such as corporate social responsibility and the stakeholders’ theory. Indeed, new incorporated corporate concepts have reshaped the way the corporation is perceived and its relationship with the environment. On the other hand, Canadian competition law attempts at integrating social concerns into its political sphere. In 2013, the Supreme Court of Canada has allowed the commencement of proceedings by indirect purchasers by way of a class action (see cases of Pros-sys, Sun-Rype and Infineon). Case law contemplates limiting the negative impact of anti-competition practices implemented by multinational corporations. The objective is to reinstate an economic balance as between corporations and its clients. The consumer is indeed called upon to play a protective role in the market in addition to the Canadian Competition authority’s competence. As affirmed by the Canadian Competition Tribunal in the decision of Visa/Master Card certain competition disputes between merchants are of common interest. Thus, the public should be made aware of the difficulties met by the businesses in the market. In light of the recent Canadian case law standpoint, it most certainly raises questions about the role that competition policies play within the corporation’s economic activities framework. This paper suggests showing the current legal positions of Canadian corporations and its competition law framework, in addition to putting them into perspective with their US and European counterparts. In addition to demonstrating their convergence in favor of a more social concern, we stand for the proposition that corporations, as has been defined by the jurist, does not only form a contract. Indeed, it is an institution that carries responsibilities as against its own environment.

À la prochaine…

Ivan Tchotourian

rémunération Structures juridiques Valeur actionnariale vs. sociétale

Changer la conception de la société par actions

Ivan Tchotourian 25 juin 2016

Bonjour à toutes et à tous, voici un très bel article de Susan Holmberg et Mark Schmitt accessible en ligne : « The Milton Friedman Doctrine Is Wrong. Here’s How to Rethink the Corporation » (Evonomics, 9 juin 2016).

The compensation of American executives—CEOs and their “C-suite” colleagues—has long been a matter of controversy, especially recently, as the wages of average workers have stagnated and economic inequality has moved to the center of the national debate. Just about every spring, the season of corporate proxy votes, we see the rankings of the highest-paid CEOs, topped by men (they’re all men until number 21) like David Cote of Honeywell, who in 2013 took home $16 million in salary and bonus, and another $9 million in stock options.

(…)

The problem isn’t that the political system doesn’t want to deal with excessive CEO pay. There have been any number of formal efforts to rein in executive pay, involving a host of direct regulation and tax changes. But most of the specific efforts to reduce executive pay—through major policies such as a limit on the tax deductibility of high salaries, as well as more modest accounting and disclosure legislation—have fallen short. That’s because the story of skyrocketing executive pay is a story about our conception of the corporation and its responsibilities. And until we rethink our deepest assumptions about the corporation, we won’t be able to master the challenge of excessive CEO pay, or the inequality it generates. Is the CEO simply the agent of the company’s shareholders? Is the corporation’s only obligation to return short-term gains to shareholders? Or can we begin to think of the corporation in terms of the interests of all those who have a stake in its success—its customers, its community, and all of its employees? If we take the latter view, the challenge of CEO pay will become clearer and more manageable.

À la prochaine…

Ivan Tchotourian

Gouvernance normes de droit

Protégeons les sièges sociaux !

Ivan Tchotourian 25 juin 2016

Le message est clair pour Robert Dutton : « Québec doit protéger ses sièges sociaux » (Journal de Montréal, 20 juin 2016). Pendant son intervention, Robert Dutton a précisé qu’un fonds ad hoc devrait être créée et avoir des objectifs de rendement à remplir. L’homme d’affaires pense aussi que le gouvernement pourrait voter des lois pour protéger les sièges sociaux, par exemple, en accordant plus de droits de vote aux actionnaires de longue date qu’aux spéculateurs ou en octroyant des pouvoirs aux conseils d’administration, qui reçoivent des offres d’achat hostiles.

Robert Dutton réclame la création d’un fonds d’intervention pour protéger les entreprises québé-coises de prises de contrôle étrangères. Selon l’ancien président et chef de la direction de RONA, il ne revient pas à la Caisse de dépôt et placement du Québec d’assumer un tel mandat.

À la prochaine…

Ivan Tchotourian