Business, and the dominant legal form of business, that is, the corporation, must be involved in the transition to sustainability, if we are to succeed in securing a safe and just space for humanity. The corporate board has a crucial role in determining the strategy and the direction of the corporation. However, currently, the function of the corporate board is constrained through the social norm of shareholder primacy, reinforced through the intermediary structures of capital markets. This article argues that an EU law reform is key to integrating sustainability into mainstream corporate governance, into the corporate purpose and the core duties of the corporate board, to change corporations from within. While previous attempts at harmonizing core corporate law at the EU level have failed, there are now several drivers for reform that may facilitate a change, including the EU Commission’s increased emphasis on sustainability. Drawing on this momentum, this article presents a proposal to reform corporate purpose and duties of the board, based on the results of the EU-funded research project, Sustainable Market Actors for Responsible Trade (SMART, 2016–2020).

Billet à découvrir sur le site de Harvard Law School Forum on Corporate Governance pour y lire cet article consacré à la sortie de crise sanitaire et aux apports de la raison d’être et des critères ESG : « ESG and Corporate Purpose in a Disrupted World » (Kristen Sullivan, Amy Silverstein et Leeann Galezio Arthur, 10 août 2020).

Extrait :

Corporate purpose and ESG as tools to reframe pandemic-related disruption

The links between ESG, company strategy, and risk have never been clearer than during the COVID-19 pandemic, when companies have had to quickly pivot and respond to critical risks that previously were not considered likely to occur. The World Economic Forum’s Global Risks Survey 2020, published in January 2020, listed “infectious diseases” as number 10 in terms of potential economic impact, and did not make the top 10 list of risks considered to be “likely.” The impact of the pandemic was further magnified by the disruption it created for the operations of companies and their workforces, which were forced to rethink how and where they did business virtually overnight.

The radical recalibration of risk in the context of a global pandemic further highlights the interrelationships between long-term corporate strategy, the environment, and society. The unlikely scenario of a pandemic causing economic disruption of the magnitude seen today has caused many companies—including companies that have performed well in the pandemic—to reevaluate how they can maintain the long-term sustainability of the enterprise. While the nature and outcomes of that reevaluation will differ based on the unique set of circumstances facing each company, this likely means reframing the company’s role in society and the ways in which it addresses ESG-related challenges, including diversity and inclusion, employee safety, health and well-being, the existence of the physical workplace, supply chain disruptions, and more.

ESG factors are becoming a key determinant of financial strength. Recent research shows that the top 20 percent of ESG-ranked stocks outperformed the US market by over 5 percentage points during a recent period of volatility. Twenty-four out of 26 sustainable index funds outperformed comparable conventional index funds in Q1 2020. In addition, the MSCI ACWI ESG Leaders Index returned 5.24 percent, compared to 4.48 percent for the overall market, since it was established in September 2007 through February 2020. Notably, BlackRock, one of the world’s largest asset managers, recently analyzed the performance of 32 sustainable indices and compared that to their non-sustainable benchmarks as far back as 2015. According to BlackRock the findings indicated that “during market downturns in 2015–16 and 2018, sustainable indices tended to outperform their non-sustainable counterparts.” This trend may be further exacerbated by the effects of the pandemic and the social justice movement.

Financial resilience is certainly not the only benefit. Opportunities for brand differentiation, attraction and retention of top talent, greater innovation, operational efficiency, and an ability to attract capital and increase market valuation are abundant. Companies that have already built ESG strategies, measurements, and high-quality disclosures into their business models are likely to be well-positioned to capitalize on those opportunities and drive long-term value postcrisis.

As businesses begin to reopen and attempt to get back to some sense of normalcy, companies will need to rely on their employees, vendors, and customers to go beyond the respond phase and begin to recover and thrive. In a postpandemic world, this means seeking input from and continuing to build and retain the confidence and trust of those stakeholder groups. Business leaders are recognizing that ESG initiatives, particularly those that prioritize the health and safety of people, will be paramount to recovery.

What are investors and other stakeholders saying?

While current events have forced and will likely continue to force companies to make difficult decisions that may, in the short term, appear to be in conflict with corporate purpose, evidence suggests that as companies emerge from the crisis, they will refresh and recommit to corporate purpose, using it as a compass to focus ESG performance. Specific to the pandemic, the public may expect that companies will continue to play a greater role in helping not only employees, but the nation in general, through such activities as manufacturing personal protective equipment (PPE), equipment needed to treat COVID-19 patients, and retooling factories to produce ventilators, hand sanitizer, masks, and other items needed to address the pandemic. In some cases, decisions may be based upon or consistent with ESG priorities, such as decisions regarding employee health and well-being. From firms extending paid sick leave to all employees, including temporary workers, vendors, and contract workers, to reorienting relief funds to assist vulnerable populations, examples abound of companies demonstrating commitments to people and communities. As companies emerge from crisis mode, many are signaling that they will continue to keep these principles top of mind. This greater role is arguably becoming part of the “corporate social contract” that legitimizes and supports the existence and prosperity of corporations.

In the United States, much of the current focus on corporate purpose and ESG is likely to continue to be driven by investors rather than regulators or legislators in the near term. Thus, it’s important to consider investors’ views, which are still developing in the wake of COVID-19 and other developments.

Investors have indicated that they will assess a company’s response to the pandemic as a measure of stability, resilience ,and adaptability. Many have stated that employee health, well-being, and proactive human capital management are central to business continuity. Investor expectations remain high for companies to lead with purpose, particularly during times of severe economic disruption, and to continue to demonstrate progress against ESG goals.

State Street Global Advisors president and CEO Cyrus Taraporevala, in a March 2020 letter to board members, emphasized that companies should not sacrifice the long-term health and sustainability of the company when responding to the pandemic. According to Taraporevala, State Street continues “to believe that material ESG issues must be part of the bigger picture and clearly articulated as part of your company’s overall business strategy.” According to a recent BlackRock report, “companies with strong profiles on material sustainability issues have potential to outperform those with poor profiles. We believe companies managed with a focus on sustainability may be better positioned versus their less sustainable peers to weather adverse conditions while still benefiting from positive market environments.”

In addition to COVID-19, the recent social justice movement compels companies to think holistically about their purpose and role in society. Recent widespread protests of systemic, societal inequality leading to civil unrest and instability elevate the conversation on the “S” and “G” in ESG. Commitments to the health and well-being of employees, customers, communities, and other stakeholder groups will also require corporate leaders to address how the company articulates its purpose and ESG objectives through actions that proactively address racism and discrimination in the workplace and the communities where they operate. Companies are responding with, among other things, statements of support for diversity and inclusion efforts, reflective conversations with employees and customers, and monetary donations for diversity-focused initiatives. However, investors and others who are pledging to use their influence to hold companies accountable for meaningful progress on systemic inequality will likely look for data on hiring practices, pay equity, and diversity in executive management and on the board as metrics for further engagement on this issue.

What can boards do?

Deloitte US executive chair of the board, Janet Foutty, recently described the board as “the vehicle to hold an organization to its societal purpose.” Directors play a pivotal role in guiding

companies to balance short-term decisions with long-term strategy and thus must weigh the needs of all stakeholders while remaining cognizant of the risks associated with each decision. COVID-19 has underscored the role of ESG principles as central to business risk and strategy, as well as building credibility and trust with investors and the public at large. Boards can advise management on making clear, stakeholder-informed decisions that position the organization to emerge faster and stronger from a crisis.

It has been said before that those companies that do not control their own ESG strategies and narratives risk someone else controlling their ESG story. This is particularly true with regards to how an organization articulates its purpose and stays grounded in that purpose and ESG principles during a crisis. Transparent, high-quality ESG disclosure can be a tool to provide investors with information to efficiently allocate capital for long-term return. Boards have a role in the oversight of both the articulation of the company’s purpose and how those principles are integrated with strategy and risk.

As ESG moves to the top of the board agenda, it is important for boards to have the conversation on how they define the governance structure they will put in place to oversee ESG. Based on a recent review, completed by Deloitte’s Center for Board Effectiveness, of 310 company proxies in the S&P 500, filed from September 1, 2019, through May 6, 2020, 57 percent of the 310 companies noted that the nominating or governance committee has primary oversight responsibility, and only 9 percent noted the full board, with the remaining 34 percent spread across other committees. Regardless of the primary owner, the audit committee should be engaged with regard to any ESG disclosures, as well as prepared to oversee assurance associated with ESG metrics.

Conclusion

The board’s role necessitates oversight of corporate purpose and how corporate purpose is executed through ESG. Although companies will face tough decisions, proactive oversight of and transparency around ESG can help companies emerge from recent events with greater resilience and increased credibility. Those that have already embarked on this journey and stay the course will likely be those well-positioned to thrive in the future.

Questions for the board to consider asking:

How are the company’s corporate purpose and ESG objectives integrated with strategy and risk?

Has management provided key information and assumptions about how ESG is addressed during the strategic planning process?

How is the company communicating its purpose and ESG objectives to its stakeholders?

What data does the company collect to assess the impact of ESG performance on economic performance, how does this data inform internal management decision- making, and how is the board made aware of and involved from a governance perspective?

Does the company’s governance structure facilitate effective oversight of the company’s ESG matters?

How is the company remaining true to its purpose and ESG, especially now given COVID-19 pandemic and social justice issues?

What is the board’s diversity profile? Does the board incorporate diversity when searching for new candidates?

Have the board and management discussed executive management succession and how the company can build a diverse pipeline of candidates?

How will the company continue to refresh and recommit to its corporate purpose and ESG objectives as it emerges from the pandemic response and recovery and commit to accelerating diversity and inclusion efforts?

How does the company align its performance incentives for executive leadership with attaining critical ESG goals and outcomes?

Recent events—notably including the pandemic, its disparate impact on various segments of society, and the focus on inequality and injustice arising in the wake of the death of George Floyd—have accelerated the conversation on corporate purpose. The result has been substantial, salutary reflection about the role that corporations play in creating and distributing economic prosperity and the nexus between value and values.

For our part, we have supported stakeholder governance for over 40 years—first, to empower boards of directors to reject opportunistic takeover bids by corporate raiders, and later to combat short-termism and ensure that directors maintain the flexibility to invest for long-term growth and innovation. We continue to advise corporations and their boards that—consistent with Delaware law—they may exercise their business judgment to manage for the benefit of the corporation and all of its stakeholders over the long term.

In looking beyond the disruption caused by the pandemic, boards and corporate leaders have an opportunity to rebuild with the clarity and conviction that come from articulating a corporate purpose, anchored in a holistic understanding of the key drivers of their business, the ways in which those drivers shape and are shaped by values, and the interdependencies of multiple stakeholders that are essential to the long-term success of the business.

This opportunity leads us to reiterate and refine a simple formulation of corporate purpose and objective, as follows:

The purpose of a corporation is to conduct a lawful, ethical, profitable and sustainable business in order to ensure its success and grow its value over the long term. This requires consideration of all the stakeholders that are critical to its success (shareholders, employees, customers, suppliers and communities), as determined by the corporation and its board of directors using their business judgment and with regular engagement with shareholders, who are essential partners in supporting the corporation’s pursuit of its purpose. Fulfilling purpose in such manner is fully consistent with the fiduciary duties of the board of directors and the stewardship obligations of shareholders.

This statement of corporate purpose is broad enough to apply to every business entity, but at the same time supplies clear guideposts for action and engagement. The basic objective of sustainable profitability recognizes that the purpose of for-profit corporations includes creation of value for investors. The requirement of lawful and ethical conduct ensures generally recognized standards of corporate social compliance. Going further, the broader mandate to take into account all corporate stakeholders, including communities, is not limited to local communities, but comprises society and the economy at large and directs boards to exercise their business judgment within the scope of this broader responsibility. The requirement of regular shareholder engagement acknowledges accountability to investors, but also the shared responsibility of shareholders for responsible long-term corporate stewardship.

Fulfilling this purpose will require different approaches for each corporation depending on its industry, history, regulatory environment, governance and other factors. We expect that board committees—focusing on stakeholders, ESG issues and the stewardship obligations of shareholders— will be useful or even necessary for some companies. But for all the differences among companies, there is an important unifying commonality: corporate action, taken against the backdrop of this formulation of corporate purpose, will be fully protected by the business judgment rule, so long as decisions are made by non-conflicted directors acting upon careful consideration and deliberation.

Executed in this way, stakeholder governance will be a better driver of long-term value creation and broad-based prosperity than the shareholder primacy model. Directors and managers have the responsibility of exercising their business judgment in acting for the corporate entity that they represent, balancing its rights and obligations and taking into account both risks and opportunities over the long term, in regular consultation with shareholders. Directors will not be forced to narrow their focus and act as if any one interest trumps all others, with potentially destructive consequences, but will instead have latitude to make decisions that reasonably balance the interests of all constituencies in a manner that will promote the sustainable, long-term business success of the corporation as a whole.

Alors que tout le monde évoque le changement de paradigme lié à l’émergence d’un « stakeholderism », le Wall Street Journal lance un pavé dans la mare sous la plume notamment du professeur Bebchuk : rien n’a vraiment changé ! « ‘Stakeholder’ Capitalism Seems Mostly for Show » (Wall Street Journal, 6 août 2020)

Extrait :

Notwithstanding statements to the contrary, corporate leaders are generally still focused on shareholder value. They can be expected to protect other stakeholders only to the extent that doing so would not hurt share value.

That conclusion will be greatly disappointing to some and welcome to others. But all should be clear-eyed about what corporate leaders are focused on and what they intend to deliver.

Une société d’intérêt social est une société à but lucratif qui s’engage, au moyen d’une « déclaration d’intérêt social » (benefit statement) et d’une « disposition relative à l’intérêt social » (benefit provision) à exercer ses activités de manière responsable et durable, et à promouvoir un ou plusieurs « intérêts publics » :

déclaration d’intérêt social – L’avis relatif aux statuts de la société comportera la déclaration qui suit : « Cette société est une société d’intérêt social et, par conséquent, elle s’engage à exercer ses activités de manière responsable et durable et à promouvoir un ou plusieurs intérêts publics. » (traduction libre)

disposition relative à l’intérêt social – Les statuts de la société doivent préciser les intérêts publics dont la société d’intérêt social fait la promotion et ils établissent son engagement à :

exercer ses activités de « façon responsable et durable » et

promouvoir les intérêts publics qu’elle a choisis. (traduction libre)

Un « intérêt public » s’entend d’un « effet positif » qui profite à un groupe de personnes (autre que les actionnaires en leur qualité de détenteurs d’actions), à un type de collectivité ou d’organisation, ou à l’environnement.L’« effet positif » éventuel peut notamment en être un de nature artistique, philanthropique, culturelle, écologique, éducative, environnementale, littéraire, médicale, religieuse, scientifique ou technologique.

La Loi prévoit qu’une société d’intérêt public exerce ses activités de « façon responsable et durable » si elle :

tient compte du bien-être des personnes touchées par les activités de la société d’intérêt public;

s’efforce d’utiliser une part équitable et proportionnée des ressources et capacités environnementales, sociales et économiques disponibles.

Pourquoi devenir une société d’intérêt social ?

On se demande de plus en plus si les entreprises, en plus de maximiser leur valeur pour les actionnaires, devraient avoir un objectif social plus important. La tendance croissante à l’adoption d’une législation sur les sociétés d’intérêt social aux États-Unis, et maintenant au Canada, l’illustre bien. Cette réflexion se manifeste également dans la déclaration de l’organisation américaine Business Roundtable d’août 2019 dans laquelle 181 chefs de la direction d’entreprises américaines ont redéfini la raison d’être d’une société pour manifester leur engagement collectif à diriger leur entreprise au profit de toutes les parties prenantes, notamment les clients, les employés, les fournisseurs, les collectivités et les actionnaires. Depuis 1978, la Business Roundtable a publié des principes de gouvernance d’entreprise, qui vont maintenant au-delà de la primauté des actionnaires et englobent désormais la reconnaissance des autres parties prenantes. Les lettres annuelles du président du conseil et chef de la direction de BlackRock, Larry Fink, soulignent par ailleurs le fait qu’une société ne peut réaliser de bénéfices à long terme si elle ne se fixe pas d’objectifs et si elle ne tient pas compte des besoins d’un large éventail de parties prenantes. En 2006, B Lab, un organisme sans but lucratif, a créé le programme de certification « B Corporation » dans le cadre duquel une société devient certifiée et peut se désigner comme étant une « B Corp » une fois que B Lab a évalué l’impact positif global de l’entreprise et déterminé qu’elle a obtenu un pointage vérifié minimum en fonction de son impact sur ses travailleurs, ses clients, la collectivité et l’environnement, et une fois que l’entreprise a modifié ses actes constitutifs pour y inclure certaines dispositions exigées par B Lab. La certification « B Corp » a gagné en popularité, avec une augmentation de 25 % du nombre de sociétés certifiées « B Corp » en 2019. On compte actuellement plus de 2 500 entreprises certifiées « B Corp », dont 1 269 sociétés américaines et 275 sociétés canadiennes. Certaines de ces « B Corp » sont cotées en bourse.

Les entreprises peuvent tirer parti du statut de société d’intérêt social pour acquérir un capital social et une reconnaissance de marque auprès de ses parties prenantes et en profiter pour se distinguer de ses concurrents. Dans un contexte où les investisseurs se préoccupent de plus en plus des questions environnementales et sociales et cherchent à investir dans des entreprises reconnues comme leaders dans ces domaines, le fait pour une entreprise de devenir une société d’intérêt social peut lui permettre d’accéder à des sources de financement supplémentaires de la part d’investisseurs désireux d’investir dans des entreprises qui ont à la fois un mandat économique et un mandat social.

En quoi les fonctions de l’administrateur et du dirigeant de l’entreprise d’une société d’intérêt social sont-elles différentes ?

Dans toutes les sociétés, y compris les sociétés d’intérêt social, les administrateurs et les dirigeants sont tenus à une obligation fiduciaire au titre de laquelle ils doivent agir avec intégrité et de bonne foi, au mieux des intérêts de la société.

Les administrateurs et dirigeants des sociétés d’intérêt social ont deux responsabilités supplémentaires (les « responsabilités de la société d’intérêt social ») :

agir honnêtement et de bonne foi de sorte que l’entreprise exerce ses activités de manière responsable et durable et fasse la promotion des intérêts publics inscrits aux statuts de la société;

maintenir l’équilibre entre l’obligation susmentionnée et l’obligation fiduciaire.

La Cour suprême du Canada a déclaré que les administrateurs, en exécutant leurs obligations fiduciaires et en déterminant ce qui sert au mieux les intérêts de la société, peuvent examiner les intérêts de diverses parties prenantes, notamment les employés, les fournisseurs, les créanciers, les consommateurs, les gouvernements et l’environnement, mais ils n’y sont pas tenus. Cependant, dans le cas d’une société d’intérêt social, les intérêts de certaines parties prenantes qui ne sont pas des actionnaires et dont le bien-être peut être touché par les intérêts publics stipulés dans les statuts de la société doivent, dans les faits, être examinés et les administrateurs et dirigeants doivent veiller au maintien de l’équilibre entre les intérêts de ces parties prenantes et ceux de la société dans son ensemble.

La Loi accorde une certaine protection aux administrateurs et aux dirigeants dans l’exécution de leurs obligations pour la société d’intérêt social. Ainsi, un administrateur ou un dirigeant qui agit conformément aux obligations de la société d’intérêt social ne peut être en violation de ses obligations fiduciaires d’agir dans l’intérêt supérieur de la société. Certains commentateurs ont laissé entendre que le fait de pouvoir définir l’intérêt public au sens large dans les statuts d’une société pourrait réduire considérablement l’obligation de rendre compte de la direction et du conseil d’administration. Cela ne signifie cependant pas que l’administrateur ou le dirigeant qui agit selon les intérêts publics indiqués dans les statuts de la société peut ignorer ses obligations fiduciaires à l’égard de la société, puisqu’il a l’obligation de maintenir un équilibre entre ces deux responsabilités. Comme la Loi ne fournit pas d’indications sur la façon dont les administrateurs et les dirigeants doivent s’acquitter de leurs responsabilités dans une société d’intérêt social, il appartiendra aux tribunaux de déterminer si un administrateur ou un dirigeant s’est conformé à ses obligations.

La Loi prévoit par ailleurs que les administrateurs et les dirigeants n’ont aucune obligation envers toute personne dont le bien-être peut être touché par l’exercice des activités de la société, ou qui a un intérêt public énoncé dans les statuts de la société, et qu’aucune procédure ne peut être intentée contre eux à cet effet. Des procédures peuvent uniquement être intentées en raison d’une violation des obligations de la société d’intérêt social par « un actionnaire détenant, au total, au moins 2 % des actions émises de la société ou, dans le cas d’une société ouverte, 2 % des actions émises ou des actions émises dont la juste valeur marchande se chiffre à 2 000 000 $ au moins, si ce montant est moins élevé. » (traduction libre). En raison de ces seuils, les intérêts publics énoncés dans les statuts de la société ne pourront pas tous être considérés de la même façon. Il est probable que l’accent soit mis uniquement sur les intérêts publics qui intéressent de temps à autre un grand nombre d’actionnaires.

De surcroît, un tribunal ne peut pas condamner à des dommages pécuniaires à l’égard d’une violation des responsabilités de la société d’intérêt social. Il peut cependant ordonner une mesure de réparation non pécuniaire, y compris une ordonnance de se conformer.

Comment devenir une société d’intérêt social ?

Toute société nouvelle ou déjà établie peut devenir une société d’intérêt social en incorporant la déclaration d’intérêt social dans son avis relatif aux statuts de la société et la disposition relative à l’intérêt social dans ses statuts, auxquels les actionnaires auront consenti au moyen d’une résolution spéciale. De son côté, une société d’intérêt social peut cesser de l’être en retirant la déclaration d’intérêt social dans son avis relatif aux statuts de la société et en retirant la disposition relative à l’intérêt social dans ses statuts, avec le consentement des actionnaires manifesté au moyen d’une résolution spéciale.

Les actionnaires qui s’opposent à l’ajout ou à la suppression de ces dispositions peuvent exercer leur droit à la dissidence dans le cadre de la résolution spéciale et, si cette dernière est adoptée, les actionnaires dissidents pourront faire racheter leurs actions à leur juste valeur.

Quelles sont les responsabilités continues d’une société d’intérêt social ?

Pour conserver son statut de société d’intérêt social, la société doit produire un rapport annuel des avantages qui comporte une évaluation des résultats en matière d’intérêts publics de la société selon une norme établie par une tierce partie. Les normes tierces peuvent notamment comprendre celles de la certification B Corp, de la Global Reporting Initiative et du Sustainability Accounting Standards Board. Les sociétés d’intérêt social doivent conserver leurs rapports des avantages à leur siège social et les publier sur leur site Web (si elles en ont un). Le défaut de publier leur rapport annuel sur les avantages ou de publier un rapport conforme à la Loi et à toute réglementation applicable constitue une infraction en vertu de la Loi, pour laquelle la société s’expose à une amende maximale de 5 000 $. Le gouvernement ne surveille pas l’évaluation des résultats de l’entreprise par rapport à ses intérêts publics.

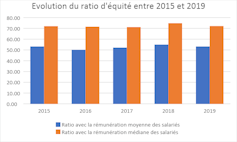

Bel article de Vanessa Serret et Mohamed Khemissi dans The conversation (27 juillet 2020) : « Rémunération des dirigeants : la transparence ne fait pas tout ». Cet article revient sur le ratio d’équité : non seulement son utilité, mais encore son niveau (20 ? 100 ?…)

Le ratio d’équité apprécie l’écart entre la rémunération de chaque dirigeant et le salaire (moyen et médian) des salariés à temps plein de son entreprise. Il est prévu un suivi de l’évolution de ce ratio au cours des cinq derniers exercices et sa mise en perspective avec la performance financière de la société. Ces comparaisons renseignent sur la dynamique du partage de la création de valeur entre le dirigeant et les salariés.

(…)

Un premier état des lieux

Sur la base des rémunérations versées en 2019 par les entreprises composant l’indice boursier du CAC 40, les patrons français ont perçu un salaire moyen de 5 millions d’euros, soit une baisse de 9,1 % par rapport à 2018.

Évolution du ratio d’équité par rapport à la rémunération moyenne (bleu) et médiane (orange) des salariés de 2015 à 2019. auteurs

Ce chiffre représente 53 fois la rémunération moyenne de leurs employés (72 fois la rémunération médiane) : un ratio acceptable, selon l’agence de conseil en vote Proxinvest. En effet, selon cette agence, et afin de garantir la cohésion sociale au sein de l’entreprise, le ratio d’équité ne doit pas dépasser 100 (par rapport à la rémunération moyenne des salariés).

Deux dirigeants s’attribuent néanmoins des rémunérations qui dépassent le maximum socialement tolérable à savoir Bernard Charlès, vice-président du conseil d’administration et directeur général de Dassault Systèmes et Paul Hudson, directeur général de Sanofi avec un ratio d’équité qui s’établit respectivement de 268 et de 107.

Notons également que pour les deux sociétés publiques appartenant à l’indice boursier du CAC 40, le ratio d’équité dépasse le plafond de 20 (35 pour Engie et 38 pour Orange) fixé par le décret n° 2012-915 du 26 juillet 2012, relatif au contrôle de l’État sur les rémunérations des dirigeants d’entreprises publiques.

La gouvernance des banques est souvent dans l’ombre de la gouvernance des entreprises. Pourtant, en cette période post COVID-19, il sa passe des choses intéressantes comme en témoigne cet article : « Ni dividendes, ni rachats d’actions, préconise la BCE » (Thierry Labro, PaperJam).

Extrait :

La Banque centrale européenne (BCE) a étendu, mardi, sa recommandation aux banques sur les distributions de dividendes et les rachats d’actions jusqu’au 1er janvier 2021 et demandé aux banques d’être extrêmement modérées en matière de rémunération variable. Dans un communiqué , elle a également précisé que «cela donnerait suffisamment de temps aux banques pour reconstituer leurs coussins de fonds propres et de liquidités afin de ne pas agir de manière procyclique».

Un nouvel examen de la situation sera fait au quatrième trimestre, et, si tout va «bien», les banques dont les fonds propres sont suffisants pourront reprendre le paiement des dividendes, dit-elle.

Elle appelle aussi les dirigeants à revoir la rémunération variable et à préférer les paiements en actions propres, par exemple.