Alors que tout le monde évoque le changement de paradigme lié à l’émergence d’un « stakeholderism », le Wall Street Journal lance un pavé dans la mare sous la plume notamment du professeur Bebchuk : rien n’a vraiment changé ! « ‘Stakeholder’ Capitalism Seems Mostly for Show » (Wall Street Journal, 6 août 2020)

Extrait :

Notwithstanding statements to the contrary, corporate leaders are generally still focused on shareholder value. They can be expected to protect other stakeholders only to the extent that doing so would not hurt share value.

That conclusion will be greatly disappointing to some and welcome to others. But all should be clear-eyed about what corporate leaders are focused on and what they intend to deliver.

Une société d’intérêt social est une société à but lucratif qui s’engage, au moyen d’une « déclaration d’intérêt social » (benefit statement) et d’une « disposition relative à l’intérêt social » (benefit provision) à exercer ses activités de manière responsable et durable, et à promouvoir un ou plusieurs « intérêts publics » :

déclaration d’intérêt social – L’avis relatif aux statuts de la société comportera la déclaration qui suit : « Cette société est une société d’intérêt social et, par conséquent, elle s’engage à exercer ses activités de manière responsable et durable et à promouvoir un ou plusieurs intérêts publics. » (traduction libre)

disposition relative à l’intérêt social – Les statuts de la société doivent préciser les intérêts publics dont la société d’intérêt social fait la promotion et ils établissent son engagement à :

exercer ses activités de « façon responsable et durable » et

promouvoir les intérêts publics qu’elle a choisis. (traduction libre)

Un « intérêt public » s’entend d’un « effet positif » qui profite à un groupe de personnes (autre que les actionnaires en leur qualité de détenteurs d’actions), à un type de collectivité ou d’organisation, ou à l’environnement.L’« effet positif » éventuel peut notamment en être un de nature artistique, philanthropique, culturelle, écologique, éducative, environnementale, littéraire, médicale, religieuse, scientifique ou technologique.

La Loi prévoit qu’une société d’intérêt public exerce ses activités de « façon responsable et durable » si elle :

tient compte du bien-être des personnes touchées par les activités de la société d’intérêt public;

s’efforce d’utiliser une part équitable et proportionnée des ressources et capacités environnementales, sociales et économiques disponibles.

Pourquoi devenir une société d’intérêt social ?

On se demande de plus en plus si les entreprises, en plus de maximiser leur valeur pour les actionnaires, devraient avoir un objectif social plus important. La tendance croissante à l’adoption d’une législation sur les sociétés d’intérêt social aux États-Unis, et maintenant au Canada, l’illustre bien. Cette réflexion se manifeste également dans la déclaration de l’organisation américaine Business Roundtable d’août 2019 dans laquelle 181 chefs de la direction d’entreprises américaines ont redéfini la raison d’être d’une société pour manifester leur engagement collectif à diriger leur entreprise au profit de toutes les parties prenantes, notamment les clients, les employés, les fournisseurs, les collectivités et les actionnaires. Depuis 1978, la Business Roundtable a publié des principes de gouvernance d’entreprise, qui vont maintenant au-delà de la primauté des actionnaires et englobent désormais la reconnaissance des autres parties prenantes. Les lettres annuelles du président du conseil et chef de la direction de BlackRock, Larry Fink, soulignent par ailleurs le fait qu’une société ne peut réaliser de bénéfices à long terme si elle ne se fixe pas d’objectifs et si elle ne tient pas compte des besoins d’un large éventail de parties prenantes. En 2006, B Lab, un organisme sans but lucratif, a créé le programme de certification « B Corporation » dans le cadre duquel une société devient certifiée et peut se désigner comme étant une « B Corp » une fois que B Lab a évalué l’impact positif global de l’entreprise et déterminé qu’elle a obtenu un pointage vérifié minimum en fonction de son impact sur ses travailleurs, ses clients, la collectivité et l’environnement, et une fois que l’entreprise a modifié ses actes constitutifs pour y inclure certaines dispositions exigées par B Lab. La certification « B Corp » a gagné en popularité, avec une augmentation de 25 % du nombre de sociétés certifiées « B Corp » en 2019. On compte actuellement plus de 2 500 entreprises certifiées « B Corp », dont 1 269 sociétés américaines et 275 sociétés canadiennes. Certaines de ces « B Corp » sont cotées en bourse.

Les entreprises peuvent tirer parti du statut de société d’intérêt social pour acquérir un capital social et une reconnaissance de marque auprès de ses parties prenantes et en profiter pour se distinguer de ses concurrents. Dans un contexte où les investisseurs se préoccupent de plus en plus des questions environnementales et sociales et cherchent à investir dans des entreprises reconnues comme leaders dans ces domaines, le fait pour une entreprise de devenir une société d’intérêt social peut lui permettre d’accéder à des sources de financement supplémentaires de la part d’investisseurs désireux d’investir dans des entreprises qui ont à la fois un mandat économique et un mandat social.

En quoi les fonctions de l’administrateur et du dirigeant de l’entreprise d’une société d’intérêt social sont-elles différentes ?

Dans toutes les sociétés, y compris les sociétés d’intérêt social, les administrateurs et les dirigeants sont tenus à une obligation fiduciaire au titre de laquelle ils doivent agir avec intégrité et de bonne foi, au mieux des intérêts de la société.

Les administrateurs et dirigeants des sociétés d’intérêt social ont deux responsabilités supplémentaires (les « responsabilités de la société d’intérêt social ») :

agir honnêtement et de bonne foi de sorte que l’entreprise exerce ses activités de manière responsable et durable et fasse la promotion des intérêts publics inscrits aux statuts de la société;

maintenir l’équilibre entre l’obligation susmentionnée et l’obligation fiduciaire.

La Cour suprême du Canada a déclaré que les administrateurs, en exécutant leurs obligations fiduciaires et en déterminant ce qui sert au mieux les intérêts de la société, peuvent examiner les intérêts de diverses parties prenantes, notamment les employés, les fournisseurs, les créanciers, les consommateurs, les gouvernements et l’environnement, mais ils n’y sont pas tenus. Cependant, dans le cas d’une société d’intérêt social, les intérêts de certaines parties prenantes qui ne sont pas des actionnaires et dont le bien-être peut être touché par les intérêts publics stipulés dans les statuts de la société doivent, dans les faits, être examinés et les administrateurs et dirigeants doivent veiller au maintien de l’équilibre entre les intérêts de ces parties prenantes et ceux de la société dans son ensemble.

La Loi accorde une certaine protection aux administrateurs et aux dirigeants dans l’exécution de leurs obligations pour la société d’intérêt social. Ainsi, un administrateur ou un dirigeant qui agit conformément aux obligations de la société d’intérêt social ne peut être en violation de ses obligations fiduciaires d’agir dans l’intérêt supérieur de la société. Certains commentateurs ont laissé entendre que le fait de pouvoir définir l’intérêt public au sens large dans les statuts d’une société pourrait réduire considérablement l’obligation de rendre compte de la direction et du conseil d’administration. Cela ne signifie cependant pas que l’administrateur ou le dirigeant qui agit selon les intérêts publics indiqués dans les statuts de la société peut ignorer ses obligations fiduciaires à l’égard de la société, puisqu’il a l’obligation de maintenir un équilibre entre ces deux responsabilités. Comme la Loi ne fournit pas d’indications sur la façon dont les administrateurs et les dirigeants doivent s’acquitter de leurs responsabilités dans une société d’intérêt social, il appartiendra aux tribunaux de déterminer si un administrateur ou un dirigeant s’est conformé à ses obligations.

La Loi prévoit par ailleurs que les administrateurs et les dirigeants n’ont aucune obligation envers toute personne dont le bien-être peut être touché par l’exercice des activités de la société, ou qui a un intérêt public énoncé dans les statuts de la société, et qu’aucune procédure ne peut être intentée contre eux à cet effet. Des procédures peuvent uniquement être intentées en raison d’une violation des obligations de la société d’intérêt social par « un actionnaire détenant, au total, au moins 2 % des actions émises de la société ou, dans le cas d’une société ouverte, 2 % des actions émises ou des actions émises dont la juste valeur marchande se chiffre à 2 000 000 $ au moins, si ce montant est moins élevé. » (traduction libre). En raison de ces seuils, les intérêts publics énoncés dans les statuts de la société ne pourront pas tous être considérés de la même façon. Il est probable que l’accent soit mis uniquement sur les intérêts publics qui intéressent de temps à autre un grand nombre d’actionnaires.

De surcroît, un tribunal ne peut pas condamner à des dommages pécuniaires à l’égard d’une violation des responsabilités de la société d’intérêt social. Il peut cependant ordonner une mesure de réparation non pécuniaire, y compris une ordonnance de se conformer.

Comment devenir une société d’intérêt social ?

Toute société nouvelle ou déjà établie peut devenir une société d’intérêt social en incorporant la déclaration d’intérêt social dans son avis relatif aux statuts de la société et la disposition relative à l’intérêt social dans ses statuts, auxquels les actionnaires auront consenti au moyen d’une résolution spéciale. De son côté, une société d’intérêt social peut cesser de l’être en retirant la déclaration d’intérêt social dans son avis relatif aux statuts de la société et en retirant la disposition relative à l’intérêt social dans ses statuts, avec le consentement des actionnaires manifesté au moyen d’une résolution spéciale.

Les actionnaires qui s’opposent à l’ajout ou à la suppression de ces dispositions peuvent exercer leur droit à la dissidence dans le cadre de la résolution spéciale et, si cette dernière est adoptée, les actionnaires dissidents pourront faire racheter leurs actions à leur juste valeur.

Quelles sont les responsabilités continues d’une société d’intérêt social ?

Pour conserver son statut de société d’intérêt social, la société doit produire un rapport annuel des avantages qui comporte une évaluation des résultats en matière d’intérêts publics de la société selon une norme établie par une tierce partie. Les normes tierces peuvent notamment comprendre celles de la certification B Corp, de la Global Reporting Initiative et du Sustainability Accounting Standards Board. Les sociétés d’intérêt social doivent conserver leurs rapports des avantages à leur siège social et les publier sur leur site Web (si elles en ont un). Le défaut de publier leur rapport annuel sur les avantages ou de publier un rapport conforme à la Loi et à toute réglementation applicable constitue une infraction en vertu de la Loi, pour laquelle la société s’expose à une amende maximale de 5 000 $. Le gouvernement ne surveille pas l’évaluation des résultats de l’entreprise par rapport à ses intérêts publics.

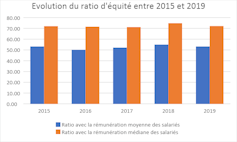

Bel article de Vanessa Serret et Mohamed Khemissi dans The conversation (27 juillet 2020) : « Rémunération des dirigeants : la transparence ne fait pas tout ». Cet article revient sur le ratio d’équité : non seulement son utilité, mais encore son niveau (20 ? 100 ?…)

Le ratio d’équité apprécie l’écart entre la rémunération de chaque dirigeant et le salaire (moyen et médian) des salariés à temps plein de son entreprise. Il est prévu un suivi de l’évolution de ce ratio au cours des cinq derniers exercices et sa mise en perspective avec la performance financière de la société. Ces comparaisons renseignent sur la dynamique du partage de la création de valeur entre le dirigeant et les salariés.

(…)

Un premier état des lieux

Sur la base des rémunérations versées en 2019 par les entreprises composant l’indice boursier du CAC 40, les patrons français ont perçu un salaire moyen de 5 millions d’euros, soit une baisse de 9,1 % par rapport à 2018.

Évolution du ratio d’équité par rapport à la rémunération moyenne (bleu) et médiane (orange) des salariés de 2015 à 2019. auteurs

Ce chiffre représente 53 fois la rémunération moyenne de leurs employés (72 fois la rémunération médiane) : un ratio acceptable, selon l’agence de conseil en vote Proxinvest. En effet, selon cette agence, et afin de garantir la cohésion sociale au sein de l’entreprise, le ratio d’équité ne doit pas dépasser 100 (par rapport à la rémunération moyenne des salariés).

Deux dirigeants s’attribuent néanmoins des rémunérations qui dépassent le maximum socialement tolérable à savoir Bernard Charlès, vice-président du conseil d’administration et directeur général de Dassault Systèmes et Paul Hudson, directeur général de Sanofi avec un ratio d’équité qui s’établit respectivement de 268 et de 107.

Notons également que pour les deux sociétés publiques appartenant à l’indice boursier du CAC 40, le ratio d’équité dépasse le plafond de 20 (35 pour Engie et 38 pour Orange) fixé par le décret n° 2012-915 du 26 juillet 2012, relatif au contrôle de l’État sur les rémunérations des dirigeants d’entreprises publiques.

La gouvernance des banques est souvent dans l’ombre de la gouvernance des entreprises. Pourtant, en cette période post COVID-19, il sa passe des choses intéressantes comme en témoigne cet article : « Ni dividendes, ni rachats d’actions, préconise la BCE » (Thierry Labro, PaperJam).

Extrait :

La Banque centrale européenne (BCE) a étendu, mardi, sa recommandation aux banques sur les distributions de dividendes et les rachats d’actions jusqu’au 1er janvier 2021 et demandé aux banques d’être extrêmement modérées en matière de rémunération variable. Dans un communiqué , elle a également précisé que «cela donnerait suffisamment de temps aux banques pour reconstituer leurs coussins de fonds propres et de liquidités afin de ne pas agir de manière procyclique».

Un nouvel examen de la situation sera fait au quatrième trimestre, et, si tout va «bien», les banques dont les fonds propres sont suffisants pourront reprendre le paiement des dividendes, dit-elle.

Elle appelle aussi les dirigeants à revoir la rémunération variable et à préférer les paiements en actions propres, par exemple.

Excellente lecture ce matin de ce billet du Harvard Law School Forum on Corporate Governance : « Legal Liability for ESG Disclosures » (de Connor Kuratek, Joseph A. Hall et Betty M. Huber, 3 août 2020). Dans cette publication, vous trouverez non seulement une belle synthèse des référentiels actuels, mais aussi une réflexion sur les conséquences attachées à la mauvaise divulgation d »information.

Extrait :

3. Legal Liability Considerations

Notwithstanding the SEC’s position that it will not—at this time—mandate additional climate or ESG disclosure, companies must still be mindful of the potential legal risks and litigation costs that may be associated with making these disclosures voluntarily. Although the federal securities laws generally do not require the disclosure of ESG data except in limited instances, potential liability may arise from making ESG-related disclosures that are materially misleading or false. In addition, the anti-fraud provisions of the federal securities laws apply not only to SEC filings, but also extend to less formal communications such as citizenship reports, press releases and websites. Lastly, in addition to potential liability stemming from federal securities laws, potential liability could arise from other statutes and regulations, such as federal and state consumer protection laws.

A. Federal Securities Laws

When they arise, claims relating to a company’s ESG disclosure are generally brought under Section 11 of the Securities Act of 1933, which covers material misstatements and omissions in securities offering documents, and under Section 10(b) of the Securities Exchange Act of 1934 and rule 10b-5, the principal anti-fraud provisions. To date, claims brought under these two provisions have been largely unsuccessful. Cases that have survived the motion to dismiss include statements relating to cybersecurity (which many commentators view as falling under the “S” or “G” of ESG), an oil company’s safety measures, mine safety and internal financial integrity controls found in the company’s sustainability report, website, SEC filings and/or investor presentations.

Interestingly, courts have also found in favor of plaintiffs alleging rule 10b-5 violations for statements made in a company’s code of conduct. Complaints, many of which have been brought in the United States District Court for the Southern District of New York, have included allegations that a company’s code of conduct falsely represented company standards or that public comments made by the company about the code misleadingly publicized the quality of ethical controls. In some circumstances, courts found that statements about or within such codes were more than merely aspirational and did not constitute inactionable puffery, including when viewed in context rather than in isolation. In late March 2020, for example, a company settled a securities class action for $240 million alleging that statements in its code of conduct and code of ethics were false or misleading. The facts of this case were unusual, but it is likely that securities plaintiffs will seek to leverage rulings from the court in that class action to pursue other cases involving code of conducts or ethics. It remains to be seen whether any of these code of conduct case holdings may in the future be extended to apply to cases alleging 10b-5 violations for statements made in a company’s ESG reports.

B. State Consumer Protection Laws

Claims under U.S. state consumer protection laws have been of limited success. Nevertheless, many cases have been appealed which has resulted in additional litigation costs in circumstances where these costs were already significant even when not appealed. Recent claims that were appealed, even if ultimately failed, and which survived the motion to dismiss stage, include claims brought under California’s consumer protection laws alleging that human right commitments on a company website imposed on such company a duty to disclose on its labels that it or its supply chain could be employing child and/or forced labor. Cases have also been dismissed for lack of causal connection between alleged violation and economic injury including a claim under California, Florida and Texas consumer protection statutes alleging that the operator of several theme parks failed to disclose material facts about its treatment of orcas. The case was appealed to the U.S. Court of Appeals for the Ninth Circuit, but was dismissed for failure to show a causal connection between the alleged violation and the plaintiffs’ economic injury.

Overall, successful litigation relating to ESG disclosures is still very much a rare occurrence. However, this does not mean that companies are therefore insulated from litigation risk. Although perhaps not ultimately successful, merely having a claim initiated against a company can have serious reputational damage and may cause a company to incur significant litigation and public relations costs. The next section outlines three key takeaways and related best practices aimed to reduce such risks.

C. Practical Recommendations

Although the above makes clear that ESG litigation to date is often unsuccessful, companies should still be wary of the significant impacts of such litigation. The following outlines some key takeaways and best practices for companies seeking to continue ESG disclosure while simultaneously limiting litigation risk.

Key Takeaway 1: Disclaimers are Critical

As more and more companies publish reports on ESG performance, like disclaimers on forward-looking statements in SEC filings, companies are beginning to include disclaimers in their ESG reports, which disclaimers may or may not provide protection against potential litigation risks. In many cases, the language found in ESG reports will mirror language in SEC filings, though some companies have begun to tailor them specifically to the content of their ESG reports.

From our limited survey of companies across four industries that receive significant pressure to publish such reports—Banking, Chemicals, Oil & Gas and Utilities & Power—the following preliminary conclusions were drawn:

All companies surveyed across all sectors have some type of “forward-looking statement” disclaimer in their SEC filings; however, these were generic disclaimers that were not tailored to ESG-specific facts and topics or relating to items discussed in their ESG reports.

Most companies had some sort of disclaimer in their Sustainability Report, although some were lacking one altogether. Very few companies had disclaimers that were tailored to the specific facts and topics discussed in their ESG reports:

In the Oil & Gas industry, one company surveyed had a tailored ESG disclaimer in its ESG Report; all others had either the same disclaimer as in SEC filings or a shortened version that was generally very broad.

In the Banking industry, two companies lacked disclaimers altogether, but the rest had either their SEC disclaimer or a shortened version.

In the Utilities & Power industry, one company had no disclaimer, but the rest had general disclaimers.

In the Chemicals industry, three companies had no disclaimer in their reports, but the rest had shortened general disclaimers.

There seems to be a disconnect between the disclaimers being used in SEC filings and those found in ESG In particular, ESG disclaimers are generally shorter and will often reference more detailed disclaimers found in SEC filings.

Best Practices: When drafting ESG disclaimers, companies should:

Draft ESG disclaimers carefully. ESG disclaimers should be drafted in a way that explicitly covers ESG data so as to reduce the risk of litigation.

State that ESG data is non-GAAP. ESG data is usually non-GAAP and non-audited; this should be made clear in any ESG Disclaimer.

Have consistent disclaimers. Although disclaimers in SEC filings appear to be more detailed, disclaimers across all company documents that reference ESG data should specifically address these issues. As more companies start incorporating ESG into their proxies and other SEC filings, it is important that all language follows through.

Key Takeaway 2: ESG Reporting Can Pose Risks to a Company

This article highlighted the clear risks associated with inattentive ESG disclosure: potential litigation; bad publicity; and significant costs, among other things.

Best Practices: Companies should ensure statements in ESG reports are supported by fact or data and should limit overly aspirational statements. Representations made in ESG Reports may become actionable, so companies should disclose only what is accurate and relevant to the company.

Striking the right balance may be difficult; many companies will under-disclose, while others may over-disclose. Companies should therefore only disclose what is accurate and relevant to the company. The US Chamber of Commerce, in their ESG Reporting Best Practices, suggests things in a similar vein: do not include ESG metrics into SEC filings; only disclose what is useful to the intended audience and ensure that ESG reports are subject to a “rigorous internal review process to ensure accuracy and completeness.”

Key Takeaway 3: ESG Reporting Can Also be Beneficial for Companies

The threat of potential litigation should not dissuade companies from disclosing sustainability frameworks and metrics. Not only are companies facing investor pressure to disclose ESG metrics, but such disclosure may also incentivize companies to improve internal risk management policies, internal and external decisional-making capabilities and may increase legal and protection when there is a duty to disclose. Moreover, as ESG investing becomes increasingly popular, it is important for companies to be aware that robust ESG reporting, which in turn may lead to stronger ESG ratings, can be useful in attracting potential investors.

Best Practices: Companies should try to understand key ESG rating and reporting methodologies and how they match their company profile.

The growing interest in ESG metrics has meant that the number of ESG raters has grown exponentially, making it difficult for many companies to understand how each “rater” calculates a company’s ESG score. Resources such as the Better Alignment Project run by the Corporate Reporting Dialogue, strive to better align corporate reporting requirements and can give companies an idea of how frameworks such as CDP, CDSB, GRI and SASB overlap. By understanding the current ESG market raters and methodologies, companies will be able to better align their ESG disclosures with them. The U.S. Chamber of Commerce report noted above also suggests that companies should “engage with their peers and investors to shape ESG disclosure frameworks and standards that are fit for their purpose.”

La puissante Association française des entreprises privées (Afep), qui représente les 113 plus grands groupes français avait demandé à ses membres de se montrer exemplaires s’ils devaient avoir recours au chômage partiel ou aux prêts garantis par l’État. L’effort demandé était à hauteur dune réduction de 20 %.

Appelées à renoncer à leurs dividendes et à modérer les rémunérations en contrepartie du recours aux dispositifs d’aide de l’Etat, les entreprises du CAC 40 ont opté pour des stratégies variables. Les trois quarts ont annulé (35 %) ou diminué (40 %) les dividendes prévus en début d’année et 17 % les ont maintenus. Certaines ont décidé de les réduire alors même qu’elles n’avaient pas besoin du soutien de l’Etat.

Le 2 août 2020, Christiaan de Brauw a publié un intéressant billet sur l’Harvard Law School Forum on Corporate Governance sous le titre « The Dutch Stakeholder Experience ».

Extrait :

Lessons learned

The Dutch experience shows that the following lessons are key to make the stakeholder-oriented governance model work in practice.

Embed a clear stakeholder mission in the fiduciary duties of the board

To have a real stakeholder model, the board must have a duty to act in the interests of the business and all the stakeholders, not only the shareholders. In shareholder models there may be some room to consider stakeholder interests. For example, in Delaware and various other US states, the interests of stakeholders other than shareholders may be considered in the context of achieving overall long-term shareholder value creation. In US states with constituency statutes, the board’s discretion is preserved: the interests of stakeholders other than shareholders can be, but do not have to be, taken into account. A meaningful stakeholder model requires the board to act in the interests of the business and all stakeholders. This is a “shall” duty, in the words of Leo Strine and Robert Eccles (see Purpose With Meaning: A Practical Way Forward, Robert G. Eccles, Leo E. Strine and Timothy Youmans, May 16, 2020). Rather than allowing for the possibility that all stakeholders’ interests will be taken into account; it should create a real duty to do so. Since 1971, boards of Dutch companies have had such a “shall” duty to follow a stakeholder mission, similar to that of a benefit corporation in, for example, Delaware.

The stakeholder duty must be clear and realistic for boards in the economic environment in which they operate. To define the contours of such a mission in a clear and practical way is not easy, as the journey of the Dutch stakeholder model shows. Today, the Netherlands has a meaningful and realistically defined fiduciary duty for boards. The primary duty is to promote the sustainable success of the business, focused on long-term value creation, while taking into account the interests of all stakeholders and ESG and similar sustainability perspectives. These principles are broadly similar to the corporate purpose and mission proposed by Martin Lipton and others (see On the Purpose of the Corporation, Martin Lipton, William Savitt and Karessa L. Cain, posted May 27, 2020).

Critics of the stakeholder model sometimes point to the ambiguity and lack of clarity of such a pluralistic model. The developments of the Dutch stakeholder model since its inception show that a pluralistic model can work in practice. By now, Dutch boards’ overriding task is adequately clear and aligned with what is typically expected of a company’s executives: pursuing the strategic direction that will most likely result in long-term and sustainable business success. The Dutch stakeholder model also has a workable roadmap to deal with stakeholders’ interests, particularly if they diverge or cannot all be protected fully at the same time, which necessarily results in trade-offs between stakeholders. A realistic approach to governance acknowledges that a stakeholder model does not mean that boards can or should seek to maximize value for all the stakeholders equally and at the same time. It is simply unrealistic to simultaneously pay (and progressively increase) dividends, increase wages and improve contract terms, while also promoting the success of the business. The Dutch interpretation of the stakeholder model, as developed through practice over decades, boils down to the focus on the sustainable success of the business and long-term value creation. As said above, stakeholders are protected by the board’s duty to prevent disproportionate or unnecessary harm to any class of stakeholders. Boards should avoid or mitigate such harm, for example, by agreeing “non-financial covenants” in a takeover. This makes sense as a way to protect stakeholder interests in a realistic manner, much more so than merely requiring boards—without any further guidance—to create value for all the stakeholders.

A stakeholder-oriented model should also be modern and flexible enough to address and incorporate important developments. The Dutch model is especially well positioned to embrace ESG and similar sustainability perspectives. For example, the Dutch company DSM has successfully illustrated this, while being profitable and attractive for investors. There is growing appreciation that being a frontrunner in ESG is required for sustainable business success. In addition to the fact that ESG is required for continuity of the business model and can often give a company a competitive edge, stakeholders increasingly require it. Simply “doing the right thing”, as an independent corporate goal, is more and more seen as important by (new millennial) employees, customers, institutional investors and other stakeholders.

There is no standard test to determine whether a business has achieved sustainable success. There will be different ways to achieve and measure success for different companies, depending on the respective circumstances. Therefore, the test will always have to be bespoke, implemented by the board and explained to stakeholders.

The Dutch stakeholder model has proven to work quite well in times of crisis, such as today’s Covid-19 crisis, as it bolsters the board’s focus on the survival and continuity of the business. The board must first assess whether there is a realistic chance of survival and continuity of the business. If not, and if insolvency becomes imminent, the board’s duties transform to focus on creditors’ interests, such as preventing wrongful trading and the winding down or restarting of the business in line with applicable insolvency/restructuring proceedings. Driven by the economic reality and the need to survive, in times of crisis, boards typically have more freedom to do what it takes to survive: from pursuing liquidity enhancing measures, implementing reorganizations, suspending dividends to shareholders and payments to creditors and so on. The success of the business remains the overriding aim, and in some cases harm to one or more classes of stakeholders may need to be accepted. In addition, in a true stakeholder model, in times of crisis there may not be sympathy for corporate raiders or activists (so-called “corona profiteers” in the current case) who want to buy listed companies on the cheap. A just say not now defense in addition to the just say no defense will readily be available for boards who are occupied with dealing with the crisis and revaluating the best strategic direction. This idea that during the Covid-crisis protection against activists and hostile bidders may be needed seems to be understood as well by, for example, ISS and Glass Lewis, evidenced by their willingness to accept new poison pills for a one year duration (see, for example, ISS and Glass Lewis Guidances on Poison Pills during COVID-19 Pandemic, Paul J. Shim, James E. Langston, and Charles W. Allen, posted on April 26, 2020).

Teeth to protect the stakeholder mission and appropriate checks and balances

The Netherlands has adopted a model in which matters of strategy are the prerogative of the executive directors under supervision of the non-executive directors or, in the still widely used two-tier system, of the management board under supervision of the supervisory board. Similar to the discretion afforded to directors under Delaware’s business judgment rule, a Dutch board has a lot of freedom to choose the strategic direction of the company. In a dispute, the amount of care taken by the board in the decision-making process will be scrutinized by courts, but normally objectively reasonable decisions will be respected. In the Dutch model the board is the captain of the ship; it is best equipped to determine the course for the business and take difficult decisions on how to serve the interests of stakeholders. Generally, the board has no obligation to consult with, or get the approval of, the shareholders in advance of a decision.

At the same time, in recognition of the significant power that boards have in the Dutch stakeholder model, there should be checks and balances to ensure the board’s powers are exercised in a careful manner, without conflicts of interest and without entrenchment. Non-executive/supervisory directors will need to exercise critical and hands-on oversight, particularly when there are potential conflicts of interest. Further, shareholders and other stakeholders are entitled to hold boards to account: boards need to be able to explain their strategic decisions. Shareholders can use their shareholder rights to express their opinions and preferences. Shareholders can also pursue the dismissal of failing and entrenched boards. Boards need regular renewed shareholder mandates through reappointments. The courts are the ultimate guardian of the stakeholder model. The Dutch Enterprise Chamber at the Amsterdam Court of Appeals, which operates in a comparable manner to the Delaware Chancery Court, is an efficient and expert referee of last resort.

The stakeholder model should not convert to a shareholder model in takeover scenarios. The board should focus on whether a takeover is the best strategic option and take into account the consequences for all the stakeholders. In most cases, the best strategic direction for the business will create the highest valuation of the business. But, and this is a real difference with shareholder models, it should be acknowledged that the stand-alone (or other best strategic) option can be different from the strategic option favored by a majority of the shareholders and the option that creates the most shareholder value. This principle was confirmed by the Dutch Enterprise Chamber in 2017 in the AkzoNobel case.

A meaningful stakeholder model requires teeth. The right governance structures need to be put in place to create and protect the long-term stakeholder mission in the face of short-term market pressure. The reality—in the Netherlands as well as in the US—is that shareholders are the most powerful constituency in the stakeholder universe, with the authority to replace the board. In Dutch practice, various countervailing measures can be used to protect the stakeholder mission. A commonly used instrument is the independent protection foundation, the Dutch poison pill. The independent foundation can exercise a call option and acquire and vote on preference shares. It can neutralize the newly acquired voting power of hostile bidders or activists and is effective against actions geared at replacing the board, including a proxy fight. Once the threat no longer exists, the preference shares are cancelled. These measures have been effective, for example, against hostile approaches of America Movil for KPN (2013) and Teva for Mylan (2015).

Foster a stakeholder mindset, governance and environment

Perhaps the most important prerequisite for a well-functioning stakeholder model is the actual mindset of executives and directors. This mindset drives how they will use their stakeholder powers. Fiduciary duties—also in a stakeholder model—are “open norms” and leave a lot of freedom to boards to pursue the strategic direction and to use their authority as they deem fit. The prevailing spirit and opinions about governance are important, as they influence how powers are interpreted and exercised. As an example, the Dutch requirement that boards need to act in the interest of the company and its business dates from 1971, but that did not prevent boards in the 2000s from seeing shareholders as the first among equals. Today, the body of ideas about governance in the developed world is tending to converge towards stakeholder-oriented governance. This seems to indicate a fundamental change in mindset, not merely a fashionable trend or lip service. Board members with a stakeholder conviction should not be afraid to follow their mission, even if it runs counter to past experience or faces shareholder opposition. Of course, the future will hold the ultimate test for the stakeholder model. Can it, in practice, deliver on its promise to create sustainable success and long-term value and provide better protection for stakeholders? If so, this will create a positive feedback loop in which more boards embrace it.

Stakeholder-based governance models remain works in progress. In order to succeed in the long term, models that grant boards the authority to determine the strategy need to stay viable and attractive for shareholders. Going forward, boards following a stakeholder-based model will likely need to focus more on accountability, for example by concretely substantiating their strategic plans and goals and, where possible, providing the relevant metrics to measure their achievements. In reality, stakeholder models are already attractive for foreign investors: about 90% of investors in Dutch listed companies are US or UK investors. In addition, developments in the definition of the corporate purpose will further refine the stakeholder model. In the Netherlands, there has been a call to action by 25 corporate law professors who argue that companies should act as responsible corporate citizens and should articulate a clear corporate purpose.

To make stakeholder governance work, ideally, all stakeholders are committed to the same mission. It is encouraging that key institutional investors are embracing long-term value creation and the consideration of other stakeholders’ interests, for instance by supporting the New Paradigm model of corporate governance and stewardship codes to that effect. However, the “proof of the pudding” is whether boards can continue to walk the stakeholder talk and pursue the long-term view in the face of short-term pressure, either through generally accepted goals and behavior or, if necessary, countervailing governance arrangements. Today, it is still far from certain whether institutional investors will reject pursuing a short-term takeover premium, even where they consider the offer to be undervalued or not supportive of long-term value creation. Annual bonuses of the deciding fund manager may depend on accepting that offer. Until the behavior of investors in such scenarios respects the principle of long-term value creation, appropriate governance protection is important to prevent a legal pathway for shareholders to impose their short-term goals. Therefore, even in jurisdictions where stakeholder-based approaches have been embraced, and are actually pursued by boards, governance arrangements might need to be changed to make the stakeholder mission work in practice. Clear guidance for boards is needed on what the stakeholder mission is and how to deal with stakeholders’ interests, as well as catering for adequate powers and protection for boards.

The Dutch model, which requires a company to be business success-driven, have a “shall duty” to stakeholders that applies even in a sale of the company, and that recognizes that corporations are dependent on stakeholders for success and have a corresponding responsibility to stakeholders, has been demonstrated to be consistent with a high-functioning economy. By highlighting the Dutch system, however, I do not mean to claim that it is unique. For policymakers who are considering the merits of a stakeholder-based governance model, the Dutch system should be seen as one example among many corporate governance systems in successful market economies (such as Germany) that embrace this form of stakeholder-based governance. There is likely no one-size-fits-all approach; each jurisdiction should find the tailor-made model that works best for it, like perhaps the introduction of the corporate purpose in the UK and France. In any event, there is a great benefit in exchanging ideas and learning from experiences in different jurisdictions to find common ground and best practices in order to increase the acceptance and appreciation of stakeholder-oriented governance models.

US governance practices have been, and are, influential around the world. In the 2000s the pendulum in developed countries, including to some extent in the Netherlands, clearly swung in the direction of shareholder-centric governance as championed in the US. In the current environment, if the US system’s focus on shareholders is not adjusted to protect stakeholder interests, it may over time perhaps become an outlier among many of the world’s leading market economies that in one way or the other have adopted a stakeholder approach. Adjustment towards stakeholder governance seems certainly possible in the US, for example through the emerging model of corporate governance, the Delaware Public Benefit Corporation. The benefit corporation seems to have many if not all of the key attributes of the Dutch system and could provide a promising path forward if American corporate governance is to change in a way that makes the US model truly focused on the long-term value for all stakeholders. The question for US advocates of stakeholder governance is whether they will embrace it, or adopt another effective governance change, and make their commitment to respect stakeholders rea