divulgation financière | Page 2

autres publications divulgation financière engagement et activisme actionnarial Normes d'encadrement

Investissement éthique : où en est le droit ? Une réflexion

Ivan Tchotourian 16 janvier 2017

Il n’est pas rare que dans le cadre de ce bloque, je vous renvoie à des publications et des billets mis sur LinkedIn. Une fois n’est pas coutume, en voilà un de plus : E. Forget, « Ethical Investment Funds A French and Luxembourg Law Analysis » (11 janvier 2017). Cette auteure qui n’en est pas à son coup d’essai (sa belle thèse portait sur « L’investissement éthique : analyse juridique ») offre une belle réflexion sur l’investissement éthique et les dernières évolutions réglementaires intervenues en France et aux Luxembourg (avec un détour par l’Europe), ainsi que sur les orientations réglementaires choisies : transparence, conformité et responsabilisation des investisseurs. À lire pour celles et ceux qui s’intéressent à la responsabilité sociétale !

Voici le plan de cet article :

There exist a variety of ethical investment funds, as wide as the values on which they are based (I). While all ethical investment funds must be structured and managed in accordance with the rule applicable to all investment funds, some of them are subject to specific regulations (II). Finally, because ethics bring a nuance to this specific form of investment funds, it impacts the set of rules for this type of investment. It establishes the content of the investment policy and requires financial intermediaries to inform investors adequately. It also forces them to ensure ethical compliance of the investment to its ending. Ethical investment, however, is not limited to this, and investors are enjoined to take an active part in the life of the companies of which they hold shares (III).

À la prochaine…

Ivan Tchotourian

divulgation financière Normes d'encadrement Nouvelles diverses

Information extra-financière : quelle place ?

Ivan Tchotourian 28 septembre 2016

I. Mejri Hamdi et A. Mennechet propose un intéressant papier sur Boursorama.com intitulé : « Information extra-financière, quelle place dans l’analyse financière ? » (6 septembre 2016). Les auteurs reviennent sur l’émergence de l’information extra-financière et la manière dont l’offre et la demande ont évolué en ce domaine, tout en soulignant les difficultés existantes.

L’information extra-financière a été au cœur de l’actualité ces derniers mois, notamment avec le cas de Volkswagen. Le constructeur allemand a reconnu en septembre 2015 avoir manipulé les tests d’émission de certains véhicules aux États-Unis grâce à un logiciel espion. Pour les investisseurs, l’action Volkswagen est devenue un pari difficile à maintenir en portefeuille, avec une performance de -41,23 % sur 1 an (au 6 mai 2016). Mais certains gérants habiles n’ont pas eu à subir cette contribution négative, notamment grâce à l’analyse extra-financière en excluant le titre (voire le secteur automobile dans son ensemble) de leur univers d’investissement sur la base de critères ESG (Environnement, social, gouvernance). Certaines sociétés de gestion, tout en prenant en compte ces critères, avaient tout de même choisi de détenir le titre Volkswagen. Il est donc légitime de s’interroger sur la valeur ajoutée de cette information extra-financière et de sa place dans l’analyse financière.

La période récente a été également marquée par le développement de l’offre d’information extra-financière avec le lancement de notations ESG sur les fonds en 2016 (Morningstar-Sustainalytics, MSCI ESG Research), ainsi qu’un cadre réglementaire plus incitatif (art. 173 de la loi de transition énergétique pour le reporting des OPCVM).

Si la prise en compte de l’information extra-financière au sens large dans les décisions d’investissement n’est pas nouvelle, on constate néanmoins un engouement pour cette information et la finance durable ces dernières années. Selon le GSIA (Global Sustainable Investment Alliance), les actifs gérés par toutes les formes de finance durable ont progressé en moyenne de 61 % entre fin 2012 et début 2014, pour atteindre 21 358 Mds $ au niveau mondial, soit 30,2 % des actifs sous gestion (21,5 % en 2012). À cette même date, l’Europe représentait le premier marché de la finance durable (63,7 % des encours globaux) devant l’Amérique du Nord (35,2 %), l’Asie-Pacifique étant encore à ses balbutiements (environ 1 %). Les investisseurs institutionnels en sont les principaux porteurs (86,9 % début 2014).

Dans le contexte d’après 2008 et suite aux multiples scandales de l’industrie financière, ce regain d’intérêt pour la finance durable s’inscrit surtout dans une attente plus large des investisseurs, à la recherche de plus de transparence et d’utilité sociale dans leurs placements.

À la prochaine…

Ivan Tchotourian

divulgation financière Gouvernance Normes d'encadrement

Résultat de la consultation du FRC sur la transparence financière en matière de changement climatique

Ivan Tchotourian 20 août 2016

Un groupe de travail du Financial Reporting Council (FRC) a publié fin avril 2016 un bilan de la 1e phase de son travail : « Phase 1 Report of the Task Force on Climate-Related Financial Disclosures (TCFD) ». Qu’en retenir ?

Objectifs

We support the objectives of the TCFD and welcome that it is focussing on financial risks and in particular those that could have a potential impact on future cash flows. We believe that this is important in identifying the boundary of information that would be relevant to investors’ decision-making. As with any project with multiple objectives there will be instances where a trade-off is necessary. Consistent principles are important, but absolute uniformity in disclosures detracts from careful consideration and communication of information that is relevant for its users. Whilst climate related risks will be important to many companies any recommendations must be proportionate and balanced, to avoid excessive focus on one set of risks to the detriment of disclosures of the other principal risks and uncertainties a company faces. Boards must retain responsibility for determining what disclosures, if any, on climate related risks are relevant and material. This requires an understanding of the potential impacts of climate change and legislative responses, and the application of judgement. Identification of factors to be considered by management when making such an assessment will be helpful.

Portée

The recommendation should provide preparers and their boards an understanding of the factors to consider when assessing, mitigating and, where necessary, reporting the climate change risks they might face. Factors to consider might include the sensitivity of its business model to climate related legislation (for example, the existence of low carbon substitute products or processes); the energy use and carbon emissions of the company, its products and suppliers; the company’s investment planning periods; and the geographical location of operations and its distribution channels. High risk sectors could then be used to illuminate those factors.

Utilisateurs

We note from the Phase 1 Report that the intended users for the information goes beyond those making direct investments in companies to those further back in the capital supply chain. We welcome this to ensure more informed capital allocation decisions. However the disclosure recommendations will need to take into consideration the needs of the intended audience and be dependent on the type of preparer as different considerations will apply for climate related risks arising from companies reporting on their own operational activities in their annual report and those investing in a portfolio of assets or advising on investment activities. We also encourage the TCFD to consider the placement of information outside the annual report when recommending disclosures that might go beyond the needs of the annual report’s intended audience. We encourage reporting of more detailed voluntary information for investors or other users outside the annual report so that it does not detract from the key messages.

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière Normes d'encadrement

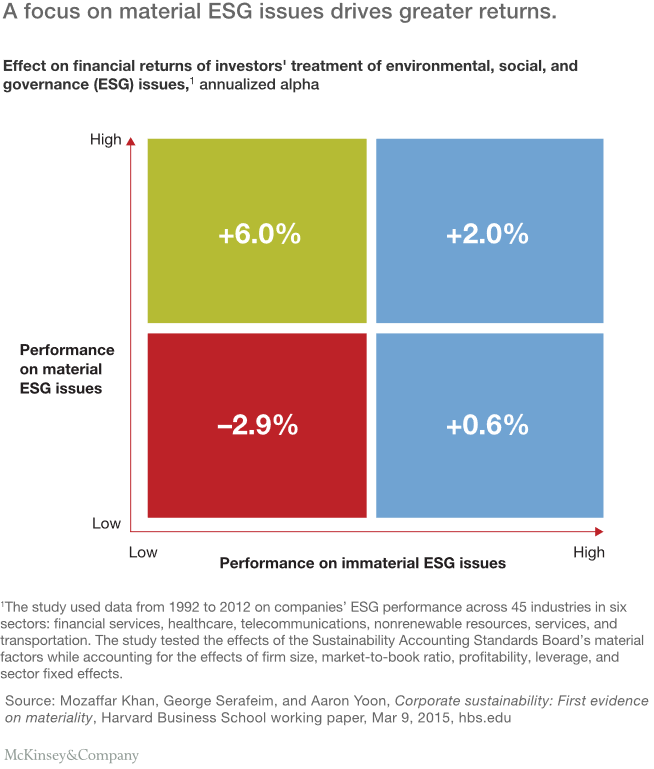

What institutional investors should do next on ESG : un beau rapport !

Ivan Tchotourian 26 juin 2016

C’est sous ce titre que le cabinet McKinsey (sous la plume de Jonathan Bailey, Bryce Klempner et Josh Zoffer) publie un excellent rapport en juin 2016 : « Sustaining sustainability: What institutional investors should do next on ESG ».

Mainstream institutions have made progress integrating environmental, social, and governance factors into their investing, but they still have far to go. Six ideas can take them to the next level.

Voici les 6 étapes énoncées :

- Require uniform corporate ESG-reporting standards based on the principle of materiality

- Build a shared ESG-rating system for external managers

- Work together to engage with corporations

- Stress-test portfolios for ESG risk factors

- Use a long-term ESG outlook to unlock new investment opportunities

- Confront the skepticism and misunderstanding that surround ESG head-on

À la prochaine…

Ivan Tchotourian

divulgation financière Gouvernance Normes d'encadrement

Gouvernance, qualité du « reporting » et performance boursière

Ivan Tchotourian 15 mars 2016

Par l’intermédiaire de son blogue (ici), Jacques Grisé propose une analyse intéressante de M. Félix Zogning sur les liens entre gouvernance, qualité de reporting et performance des entreprises.

Son article, paru sur le site de l’Ordre des administrateurs agréés du Québec (OAAQ) en janvier 2016, fait une excellente analyse de l’efficacité des pratiques de gouvernance eu égard à l’amélioration de la divulgation des informations et à la performance boursière de l’entreprise.

Accéder à cet article : « Gouvernance, qualité du « reporting » et performance boursière ».

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière mission et composition du conseil d'administration Normes d'encadrement normes de droit

Divulgation extra-financière en Angleterre : quel bilan ?

Ivan Tchotourian 3 février 2016

Le Climate Disclosure Standards Board a publié un bilan de la divulgation extra-financière des entreprises dans les domaines environnemental et des gaz à effet de serre du FTSE500 (ici), suite à la réforme introduite au Company Act 2006 en 2013 (Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013).

Voici quelques chiffres extraits de ce bilan :

Principal risks : 41% of companies consider environmental risks in their analysis of the principal risks to their company.

KPIs : 27% of companies make use of environmental KPIs. Of those that do, the majority use one of four main categories of KPIs based on: GHG emissions, energy, water or waste management (Figure 1).

Future development : 42% of companies identify environmental matters when considering the future development, performance or position of their company.

Environmental policies : 87% of companies disclosed environmental policies, 78% disclosed their policies and provided an indication of the effectiveness of those policies.

Environmental impacts : 90% of companies disclosed information regarding the environmental impacts of their business operations (Figure 2). Of the 10% that did not, 70% provided an explanation as to why that information was omitted.

GHG emissions : The Regulations require the disclosure of total annual GHG emissions (CO2e) for which a company is responsible. 90% of companies disclosed their total annual GHG emissions. 77% of companies disclosed the breakdown of both Scope 1 and 2 GHG emissions. 41% of companies disclosed omitted emission sources and explained the reasons for omission. Of the companies who explained omissions, the majority (44%) cited materiality as the main reason for omission (Figure 3). The sources of GHG emissions omitted by companies varied widely. Figure 4 shows the range of general categories of information omitted.

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière Normes d'encadrement

Information extra-financière : les conseils des CPA

Ivan Tchotourian 1 octobre 2015

Bonsoir à toutes et à tous, Une nouvelle publication des Comptables professionnels agréés du Canada (CPA Canada) traite de l’évolution de l’information d’entreprise, en particulier en ce qui concerne les questions relatives au développement durable. Le guide de CPA Canada intitulé « L’évolution de l’information d’entreprise : Exposé sur l’information sur le développement durable, l’information intégrée et l’information sur les questions environnementales, sociales et de gouvernance » aide les sociétés ouvertes à comprendre les trois ensembles de lignes directrices concernant l’information d’entreprise volontaire élaborés par :

- la Global Reporting Initiative (GRI);

- l’International Integrated Reporting Council (IIRC);

- le Sustainability Accounting Standards Board (SASB).

La communication de l’information d’entreprise sur le développement durable est envisagée de différentes manières dans les trois ensembles de lignes directrices présentés. Rappelons que cette information, de même que l’information intégrée, est essentiellement volontaire au Canada, et va au-delà de ce qu’exigent les autorités de réglementation en valeurs mobilières en matière sociale et environnementale.

À la prochaine…

Ivan Tchotourian