autres publications | Page 3

autres publications Gouvernance Normes d'encadrement normes de droit normes de marché

Governance goes green : à lire !

Ivan Tchotourian 6 juillet 2016

Beau rapport du cabinet Weil, Gotshal & Manges LLP qui montre que la RSE ne peut plus être ignoré par les entreprises : « Governance Goes Green ».

It’s not just us tree-huggers. Increasingly, institutional investors, pension plans and regulators are calling for (and in some cases requiring) companies to assess and report on the sustainability of their business operations and investments. Climate change and other environmental concerns are at the forefront of these calls. Institutional investors are focusing on sustainable business practices – a broad category in which environmental and social risks, costs and opportunities of doing business are analyzed alongside conventional economic considerations – as a key factor in long-term financial performance. Sustainability proponents are looking to boards of directors and management to integrate these considerations into their companies’ long-term business strategies.

Éléments essentiels à retenir :

- Institutional investors increasingly regard environmental and other sustainability issues as strategic matters for companies.

- Shareholders continue to submit environmental and other sustainability proposals, successfully garnering attention and prompting companies to make changes, despite their failure to win majority votes.

- Independent organizations are developing standards for sustainability and environmental reporting to provide investors with consistent metrics for assessing and comparing the sustainability of companies’ practices.

- Sustainability and environmental reporting remains in the SEC’s sights as it evaluates the effectiveness of current disclosure requirements and considers changes for the future.

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière Normes d'encadrement

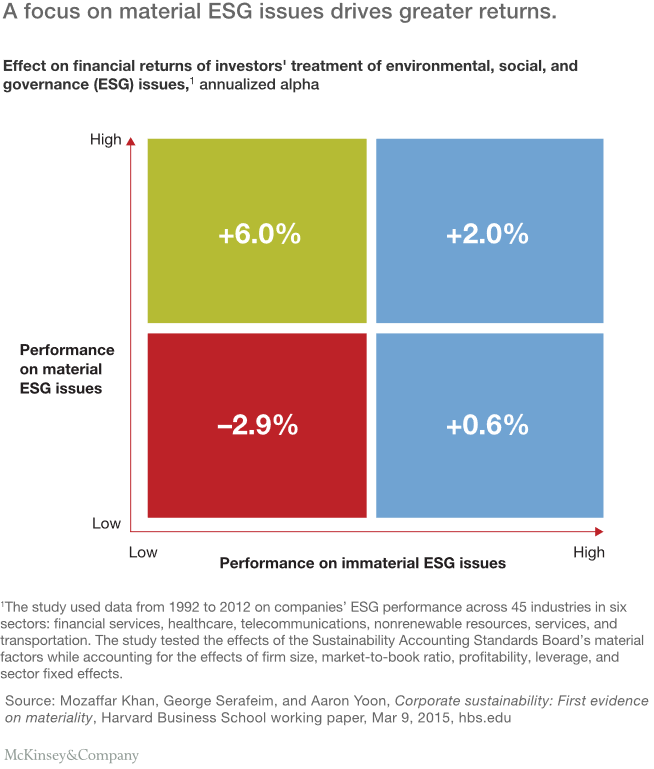

What institutional investors should do next on ESG : un beau rapport !

Ivan Tchotourian 26 juin 2016

C’est sous ce titre que le cabinet McKinsey (sous la plume de Jonathan Bailey, Bryce Klempner et Josh Zoffer) publie un excellent rapport en juin 2016 : « Sustaining sustainability: What institutional investors should do next on ESG ».

Mainstream institutions have made progress integrating environmental, social, and governance factors into their investing, but they still have far to go. Six ideas can take them to the next level.

Voici les 6 étapes énoncées :

- Require uniform corporate ESG-reporting standards based on the principle of materiality

- Build a shared ESG-rating system for external managers

- Work together to engage with corporations

- Stress-test portfolios for ESG risk factors

- Use a long-term ESG outlook to unlock new investment opportunities

- Confront the skepticism and misunderstanding that surround ESG head-on

À la prochaine…

Ivan Tchotourian

autres publications Normes d'encadrement objectifs de l'entreprise Valeur actionnariale vs. sociétale

La valeur actionnariale au rancart !

Ivan Tchotourian 31 mai 2016

Belle tribune de la professeure Lynn A Stout : « The Myth of Maximizing Shareholder Value » (OpenEdNew, 23 mai 2016).

By the end of the 20th century, a broad consensus had emerged in the Anglo-American business world that corporations should be governed according to the philosophy often called shareholder primacy. Shareholder primacy theory taught that corporations were owned by their shareholders; that directors and executives should do what the company’s owners/shareholders wanted them to do; and that what shareholders generally wanted managers to do was to maximize « shareholder value, » measured by share price. Today this consensus is crumbling. As just one example, in the past year no fewer than three prominent New York Times columnists have published articles questioning shareholder value thinking. Shareholder primacy theory is suffering a crisis of confidence. This is happening in large part because it is becoming clear that shareholder value thinking doesn’t seem to work, even for most shareholders.

Je vous laisse lire la suite…

Pour rappel, j’avais eu l’occasion de faire une recension du très bel ouvrage de Lynn A Stout dans la Revue international de droit économique – 2013/3 ((t. XXVII)) – : ici.

Lynn A. STOUT, The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations and the Public, Berrett-Koehler Publishers, 2012

1 – Un sujet d’une grande actualité

2 – Remise en cause de la norme de primauté actionnariale

3 – Les actionnaires d’aujourd’hui

4 – Mise en perspective de l’ouvrage

À la prochaine…

Ivan Tchotourian

autres publications engagement et activisme actionnarial Normes d'encadrement

Actions et contrats financiers : un travail prometteur

Ivan Tchotourian 27 mai 2016

M. Romain Dambre propose un bel ouvrage aux éditions Bruylant intitulé : « Les contrats financiers sur actions : Droit français et européen des sociétés ». Un beau sujet que l’auteur aborde !

Les contrats financiers permettent aux parties de façonner le monde à l’image d’un profil de risque optimal : les parties y créent les conditions d’une réalité dérivée, un monde synthétique purgé de risques indésirables. Instruments de transfert de risque, les contrats financiers portent la marque d’une forte abstraction à l’égard du bien sous-jacent. Si les parties peuvent souhaiter fixer les conditions d’un transfert différé de la propriété, elles privilégient souvent la vertu protectrice ou le potentiel spéculatif de ces instruments en considérant les attributs économiques attachés à la propriété du bien sous-jacent plutôt que sa titularité sur le plan juridique.

Se dégage alors une règle d’autonomie du contrat financier à l’égard du bien comme du contrat sous-jacents, justifiée notamment par des considérations d’ordre systémique tenant à la protection des marchés financiers. Cette logique est toutefois mise à l’épreuve au contact du droit des sociétés.

Technique contractuelle de synthétisation de la propriété, le contrat financier opère un hiatus potentiel entre le statut juridique de l’actionnaire et son exposition à l’aléa social, menaçant de ce fait les équilibres traditionnels du droit des sociétés, notamment en termes d’attribution de la qualité d’actionnaire et d’exercice du droit de vote.

Si la règle d’autonomie, bien qu’ébranlée, reste le principe en droit des sociétés, les principes directeurs du droit boursier – Transparence, Égalité, Intégrité – conduisent à y faire exception face aux perturbations engendrées par ces techniques de dissociation de la forme juridique et de la substance économique, que l’on pense aux hypothèses de vote « vide » ou de prises de contrôle rampantes. Aussi la réglementation boursière soumet-elle les contrats financiers sur actions à un régime similaire à celui applicable aux titres financiers sous-jacents, notamment en matière de transparence des participations, d’offre publique et de répression des abus de marché.

À la prochaine…

Ivan Tchotourian

autres publications mission et composition du conseil d'administration Normes d'encadrement

Comité de nomination : un intéressant rapport britannique

Ivan Tchotourian 24 mai 2016

En mai 2016, l’Institute of Chartered Secretaries and Administrators (ICSA) a publié avec Ernst & Young un rapport sur le rôle du comité de nomination : « The Nomination Committee – Coming out of the Shadows ».

While its role may be less clearly defined than that of the audit committee, and its profile lower than that of the remuneration committee, it is arguably the most important of the three. It plays a pivotal role in appointing directors to the board and, if the board lacks the right balance, knowledge, skills and attributes, the likelihood of it and its committees operating effectively is greatly reduced.

Concernant sa mission et ses membres, il est précisé les points suivants :

-

What the appropriate role of the committee should be, e.g., whether the committee should look at executive talent if it does not already do so, and whether the board would benefit from combining the committee into a nomination and governance committee.

-

Whether the following processes are clearly linked: the discussion of current board composition and future composition in light of the company’s strategy, the executive and senior talent succession planning and company strategy, the outcome of the board evaluation exercise and board succession plans, and the link between board evaluations and development and training plans.

-

The existence of a two-pronged approach to identify succession plans in both emergency and steady-state situations.

À propos de la planification de la relève et la détection de talent, le rapport mentionne relativement au comité :

-

The extent to which nomination committee looks across the market and internally to identify four or five potential successors to the CEO.

-

How deeply into the organisation the committee should be looking to identify future talent.

-

The best way to develop the skills of future executive leaders in the business.

À la prochaine…

Ivan Tchotourian

autres publications mission et composition du conseil d'administration Normes d'encadrement responsabilisation à l'échelle internationale

Droits de l’homme et CA : un guide en 5 étapes

Ivan Tchotourian 24 mai 2016

L’EHRC vient de publier un guide « Business and human rights – A five-step guide for company boards » bien intéressant pour les CA. Comme le précise ce document : « We recommend that boards should follow five steps to ensure that their company is fulfilling its responsibility to respect human rights in a robust and coherent manner that meets the expectations of the UN Guiding Principles and UK statutory reporting obligations. Boards should be aware of the company’s salient, or most severe, human rights risks, and ensure ».

The following are the five steps that it is recommended boards should follow to ensure that their company is fulfilling its responsibility to meet human rights in a robust and coherent manner that meets the expectations of the UN Guiding Principles and UK statutory reporting obligations:

- the company should embed the responsibility to respect human rights into its culture, knowledge and practices;

- the company should identify and understands its salient, or most severe, risks to human rights;

- the company should systematically address its salient, or most severe, risks to human rights and provide for remedies when needed;

- the company should engage with stakeholders to inform its approach to addressing human rights risks; and

- the company should report on its salient, or most severe, human rights risks and meet regulatory reporting requirements.

Attention : encore une fois, tout cela n’est que du droit international et donc du droit « mou ». Ce guide l’exprime très bien en ces termes : « The Guiding Principles do not create any new international legal obligations on companies, but they can help boards to operate with respect for human rights and meet their legal responsibilities set out in domestic laws ».

À la prochaine…

Ivan Tchotourain

autres publications mission et composition du conseil d'administration Normes d'encadrement

Banque d’Angleterre : supervisory statement pour le CA

Ivan Tchotourian 19 mai 2016

L’Autorité prudentielle de la Banque d’Angleterre vient de publier un Supervisory Statement intitulé « Corporate governance: Board responsibilities » (SS5/16, mars 2016).

The Prudential Regulation Authority has published a policy statement and accompanying supervisory statement concerning the responsibilities of boards.

The purpose of this supervisory statement is to identify, for the boards1 of firms regulated by the Prudential Regulation Authority (PRA), those aspects of governance to which the PRA attaches particular importance and to which the PRA may devote particular attention in the course of its supervision. It is not intended to provide a comprehensive guide for boards of what constitutes good or effective governance. There are more general guidelines for that purpose, for example the UK Corporate Governance Code, published by the Financial Reporting Council.

À la prochaine…

Ivan Tchotourian