Gouvernance | Page 4

divulgation financière engagement et activisme actionnarial Gouvernance

Changement climatique : BlackRock met la pression sur les entreprises

Ivan Tchotourian 15 mars 2017

En voilà une nouvelle ! Le gérant américain d’actifs BlackRock a fait savoir qu’il entendait s’intéresser à la manière dont les entreprises géraient les problèmes liés au changement climatique : « Exclusive: BlackRock vows new pressure on climate, board diversity » (Reuters, 13 mars 2017).

BlackRock Inc(BLK.N), which wields outsized clout as the world’s largest asset manager, planned on Monday to put new pressure on companies to explain themselves on issues including how climate change could affect their business as well as boardroom diversity.

The move by BlackRock, a powerful force in Corporate America with $5.1 trillion under management, could bolster efforts like climate-risk disclosure practices developed by the Financial Stability Board, the international body that monitors and makes recommendations about the global financial system.

BlackRock, which holds stakes in most major U.S. corporations, identified its top « engagement priorities » for meetings this year with corporate leaders in documents to be posted on its website on Monday, with climate risk and boardroom diversity on the list. Reuters received advance copies of the materials.

Quand on connaît le poids de ce gérant d’actifs, il y a peut-être de l’avenir pour le changement climatique !

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance normes de droit Nouvelles diverses

Capital-actions à classe multiple : c’est commun !

Ivan Tchotourian 13 mars 2017

IR Magazine offre un bel article sur la situation des entreprises américaines ayant fait leur entrée en bourse en assumant un capital-actions à classe action multiple : « How common are restricted voting rights for US shareholders? » (8 mars 2017). Une excellente occasion de revenir sur la discussion qui a entouré la récente entrée en bourse de Snap Inc.

Petits extraits d’une tendance en pleine expansion :

Snap’s IPO last week will likely be the biggest and most controversial on the NYSE in 2017. The operating company in charge of Snapchat drew ire from certain parts of Wall Street for its three-tier voting structure, which offered no voting rights to any new investors that participated in the IPO.

(…) While it is unprecedented to offer no voting rights during an IPO, the number of companies offering restricted voting rights is on the rise.

According to data from Dealogic, 27 of the 174 IPOs in the US in 2015 used dual-class structures – roughly half of these were technology companies. In 2005, just 1 percent of all IPOs used that structure.

(…) Bob Lamm, senior adviser to Deloitte’s Center for Boardroom Effectiveness, says that companies can still maintain positive relationships with investors while operating with a restricted share structure.

‘Most public companies can develop good governance practices and explain why they do what they do,’ he says, speaking to IR Magazine. ‘But if they don’t convey good corporate governance practices, they run the risk of investor discontent.’

À la prochaine…

Ivan Tchotourian

autres publications engagement et activisme actionnarial Normes d'encadrement Nouvelles diverses

US Stewardship Code : une proposition de l’ISG

Ivan Tchotourian 10 février 2017

Le 31 janvier 2017, le Investor Stewardship Group (réunissant plus de 16 investisseur), a publié un premier projet de code de gouvernance d’entreprise et de code de gérance des investisseurs. Concernant le Stewardship Code, les principes sont les suivants :

Principle A: Institutional investors are accountable to those whose money they invest.

Principle B: Institutional investors should demonstrate how they evaluate corporate governance factors with respect to the companies in which they invest.

Principle C: Institutional investors should disclose, in general terms, how they manage potential conflicts of interest that may arise in their proxy voting and engagement activities.

Principle D: Institutional investors are responsible for proxy voting decisions and should monitor the relevant activities and policies of third parties that advise them on those decisions.

Principle E: Institutional investors should address and attempt to resolve differences with companies in a constructive and pragmatic manner.

Principle F: Institutional investors should work together, where appropriate, to encourage the adoption and implementation of the Corporate Governance andStewardship principles.

Pour accéder à ces principes : cliquez ici.

À la prochaine…

Ivan Tchotourian

mission et composition du conseil d'administration normes de droit

L’indépendance d’un administrateur expliqué par les juges du Delaware

Ivan Tchotourian 2 février 2017

Dans un de ces derniers billets sur Les affaires.com, Yvan Allaire revient sur la décision américaine Sandys v. Pincus qui traite de la notion d’indépendance : « Petite révolution pour l’indépendance des administrateurs ».

Le 5 décembre 2016, la Cour suprême du Delaware a rendu une décision (dans la cause Sandys v. Pincus) qui ouvre la porte à ce que les Cours puissent évaluer l’ensemble des faits, le contexte, afin de décider si une personne, qualifiée de membre indépendant, l’est bien en réalité.

(…) Selon cette décision d’une Cour influente (près de 65% des sociétés du S&P 500 sont sous la juridiction du Delaware), la notion d’indépendance, en cas de litiges du moins, doit comporter l’examen des relations sociales et des relations d’affaires entre les membres du conseil, tout particulièrement, s’il y a lieu, avec un actionnaire de contrôle siégeant au conseil.

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance Nouvelles diverses

Can America’s Companies Survive America’s Most Aggressive Investors?

Ivan Tchotourian 24 novembre 2016

Quel bel article d’Alana Semuels dans The Atlantic (ici) ! Cette étude revient sur la politique des fonds de couverture (hedge funds) et l’implication de leur activisme sur les politiques et les stratégies mises en place par les entreprises américaines.

Extrait :

DuPont is one of dozens of American companies that have abandoned a long-term approach to doing business after being the target of so-called activist investors. These investors buy up shares of a company and attempt to maximize the returns to their shares, usually by replacing members of the board of directors with hand-picked candidates who will push the company to cut costs. Activity by such investors has skyrocketed of late. In a 20-month stretch in 2005 and 2006, there were only 52 activist campaigns, according to John C. Coffee, a professor at Columbia University Law School. Between 2010 and early 2014, by contrast, there were 1,115 activist campaigns. “Hedge-fund activism has recently spiked, almost hyperbolically,” Coffee writes in a 2016 paper, “The Wolf at The Door: The Impact of Hedge Fund Activism on Corporate Governance.”

These campaigns are damaging to the long-term outlook of individual companies like DuPont and also to America’s economy more generally. They often result in big cuts to research and development, substantial reductions in the workforce, and a focus on outcomes—in particular short-term profit—that hurt a company’s ability to survive in the long-term. The threat of activism affects companies across the economy: Even public companies not targeted by activists often change their behavior and cut costs to avoid becoming a target. This may be one of the reasons why America is slipping in funding research and development projects when compared with other countries.

À la prochaine…

Ivan Tchotourian

Gouvernance

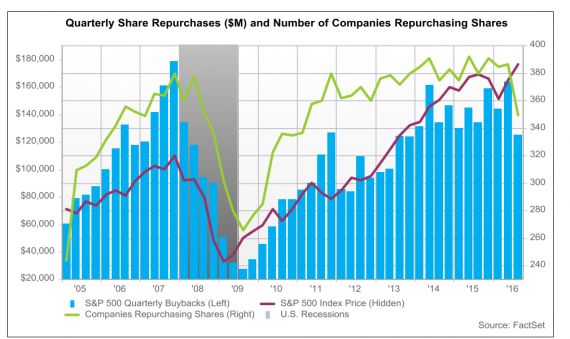

Rachat des actions : une tendance à la baisse

Ivan Tchotourian 11 octobre 2016

Mme Dominique Beauchamps a publié un billet sur son blogue de Les affaires.com intitulé : « Devrait-on s’inquiéter du recul des rachats d’actions? ». La question que pose l’auteure est centrale : est-ce une bonne chose qu’il y ait un recul des achats de ses propres actions par les entreprises ?

Les entreprises du S&P 500 ont été les moins nombreuses depuis 2010 à racheter leurs actions au deuxième trimestre et la valeur des rachats d’actions a aussi été la plus faible depuis 2013.

Quelque 275 sociétés ont racheté 127,5 milliards de dollars américains (G$US) d’actions, soit 21% de moins qu’au trimestre précédent et 3% de moins qu’un an plus tôt, rapporte S&P Dow Jones Indices.

Devrait-on s’inquiéter de voir le moins grand appétit des entreprises à racheter leurs actions?

J’ai eu l’occasion de m’exprimer il y a peu sur cette thématique dans un billet du blogue Contact : « Rachat d’actions: cul-de-sac pour les entreprises? ». Je me montre quelque peu critique sur la politique de rachat des actions et me dit que répondre à la question de Mme Beauchamp est peut-être simple : c’est non !

Comme je l’ai démontré, le rachat d’actions est donc une décision atypique qui soulève ses propres contradictions et réserves. Si une décision de racheter des actions est prise par le CA d’une entreprise, celle-ci doit en mesurer les conséquences:

- Ouvrir assurément et facilement la voie à la critique.

- Envoyer un signal souvent interprété de manière différente par les partenaires internes (je pense aux actionnaires et aux salariés, par exemple) et externes d’une entreprise.

Plus grave, à mon sens, le rachat d’actions peut cacher une politique de court terme lourde de sens: empêcher des investissements d’avenir indispensables à la relance de l’économie.

Sous peine de menacer l’équilibre dans la répartition de richesse, l’économie ne saurait en être une de rachat d’actions. Entreprises et CA, vous avez là une responsabilité qui dépasse l’entreprise: une responsabilité sociétale!

À la prochaine…

Ivan Tchotourian

Gouvernance normes de droit Nouvelles diverses

Speech de la SEC : la dénonciation encensée

Ivan Tchotourian 20 septembre 2016

Bonjour à toutes et à tous, je vous informe qu’Andrew Ceresney (directeur de la division Enforcement à la SEC) s’est exprimé lors de la Sixteenth Annual Taxpayers Against Fraud Conference à Washington le 14 septembre 2016 (« The SEC’s Whistleblower Program: The Successful Early Years »). À cette occasion, M. Ceresney est revenu sur la dénonciation, son histoire et son succès actuel… ainsi que l’influence qu’a exercé le programme de dénonciation américain pour le Canada (Ontario et Québec) et l’Australie.

Whistleblowers provide an invaluable public service, often at great personal and professional sacrifice and peril. I cannot overstate the appreciation we have for the willingness of whistleblowers to come forward with evidence of potential securities law violations. I often speak of the transformative impact that the program has had on the Agency, both in terms of the detection of illegal conduct and in moving our investigations forward quicker and through the use of fewer resources.

Dans son allocution, M. Ceserney fournit des chiffres :

- The success of the program can be seen, in part, in the over $107 million we have paid to 33 whistleblowers for their valuable assistance, in cases with more than $500 million ordered in sanctions

- Since the inception of the program, the Office has received more than 14,000 tips from whistleblowers in every state in the United States and from over 95 foreign countries. What’s more, tips from whistleblowers increased from 3,001 in fiscal year 2012 — the first full fiscal year that the Commission’s Whistleblower Office was in operation — to nearly 4,000 last year, an approximately 30% increase. And we are on target to exceed that level this year. During fiscal year 2015, the Office returned over 2,800 phone calls from members of the public. By the end of fiscal year 2015, the Commission and Claims Review Staff had issued Final Orders and Preliminary Determinations with respect to over 390 claims for whistleblower awards.

À la prochaine…

Ivan Tchotourian