“The future of business will be different,” surmised a director on a recent virtual board roundtable hosted by RSR Partners, “in ways we can’t anticipate in this moment. Our board is focused on assessing whether all our directors are truly ready for what’s coming.”

Over the past few months, RSR Partners hosted more than a dozen roundtables for sitting directors, providing a forum for the participants to share what their boards are learning as they navigate the current crisis and pivot into the “new normal.” While tackling topics as diverse as commercial strategy, operations, health and safety, and the future of business, one theme was pervasive throughout the discussions: leadership and stakeholders will be looking to the boardroom for guidance, and board members not only need to have the requisite experience and skills to confidently provide direction, but the leadership characteristics that will allow them to be effective.

Fundamentally, the global business disruption and current uncertainty has created a need for a higher level of involvement from board members. “This is a time to have board members who have experienced really tough issues, such as major ecessions, difficult mergers, major cost cutting, insolvency and bankruptcy, and top management departures, along with experience in reinventing companies, including supply chain, product engineering and simplification, digital transformation, offshore manufacturing and procurement, sale of subsidiaries, and comprehensive refinancing,” stated Edward A. Kangas, former Chairman and CEO of Deloitte Touche. “This is not a time for deep thinking. It’s time for people with real experience who know how to oversee and support management in a time of crisis and reinvention.” (Mr. Kangas currently serves on the following boards: Deutsche Bank USA Corp., Intelsat SA, VIVUS, Inc., and Hovnanian Enterprises, Inc.).

Characteristics of Directors Who Succeed in the “New Normal”

From a practical perspective, there is now a higher premium placed on a director’s proven ability to navigate a business through a crisis while mitigating risk and understanding how and when to pull the levers that will impact balance sheets. The demand to optimize results, sustain business, and adapt to changes in a regional and global market has increased alongside the time commitment and attention to detail required of directors to address these issues. Normal requirements for sound governance, audit oversight, compensation strategies, business performance goals, and succession of key leadership have continued to be paramount during the crisis. However, what the current crisis has forced boards to recognize is that a combination of specialized and diversified skillsets and characteristics will produce good corporate governance in and after 2020.

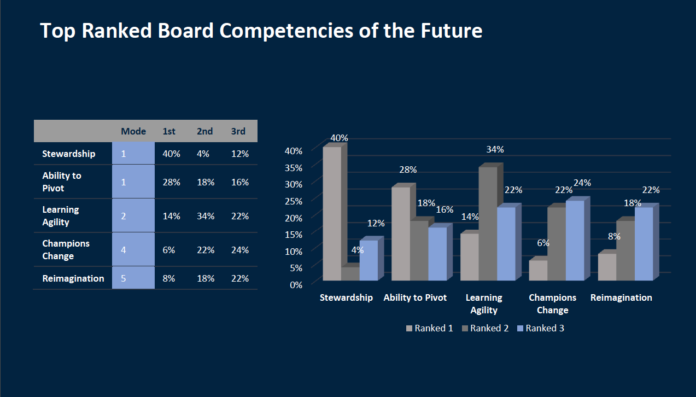

In addition to listening to the characteristics discussed in the recent roundtables, RSR Partners polled more than 250 public company board members of Fortune 50-1000 companies to identify the traits they hope to see emerge in this generation of board members. The results indicated that stewardship, the ability to pivot and learn agility, to be a champion of change, and to be capable of reimagination will be most needed by the directors charged with steering their boards in the “new normal.”

As businesses start to look beyond the COVID-19 crisis, the EY Global Integrity Report 2020 reveals divisions on the repercussions for company ethics as a result of the pandemic.

The findings are part of a survey of almost 3,000 respondents from 33 countries up to February 2020, analyzing the ethical challenges companies face in turbulent times. An additional 600 employees across all levels of seniority were surveyed at the height of the COVID-19 crisis in April in companies across six countries – China, Germany, Italy, the UK, India and the US.

The majority (90%) of respondents surveyed during the crisis believe that disruption, as a result of COVID-19, poses a risk to ethical business conduct, but there is a concerning disparity between boards, senior management and employees on the implications for compliance. While 43% of board members and 37% of senior managers surveyed believe the pandemic could lead to change and better business ethics, only 21% of junior employees appear to agree.

The survey highlights that signs of an integrity disconnect at different levels within organizations were evident even before the pandemic with more than half of board members (55%) believing management demonstrate professional integrity, but only 37% of junior employees sharing the same sentiment. In addition, over half of board members (55%) believe there are managers in their organization who would sacrifice integrity for short term gain.

The impact of the losses on shareholders will be significant. Investors, however, are being forced to rely on news reports to try to understand how the crisis is impacting companies in their portfolios and how those companies are responding. The SEC must act to require companies to provide consistent, reliable data to investors about the economic impact of the pandemic on their business, human capital management practices, and supply chain risks. These disclosures should include:

Workplace COVID-19 Prevention and Control Plan—Companies should disclose a written infectious disease prevention and control plan including information such as the company’s practices regarding hazard identification and assessment, employee training, and provision of personal protective equipment.

Identification, Contact Tracing, and Isolation—Companies should disclose their policies for identifying employees who are infected or symptomatic, contact tracing and notification for potentially exposed employees and customers, and leave policies for infected employees who are isolating.

Compliance with Quarantine Orders and phased reopening orders—Companies should disclose how they are complying with federal, state, and local government quarantine orders and public health recommendations to limit operations.

Financial Implications—Companies should disclose the impact of the COVID-19 pandemic on their cash flows and balance sheet as well as steps taken to preserve liquidity such as accessing credit facilities, government assistance, or the suspension of dividends and stock buybacks.

Executive Compensation—Companies should promptly disclose the rationale for any material modifications of senior executive compensation due to the COVID-19 pandemic, including changes to performance targets or issuance of new equity compensation awards.

Employee Leave—Companies should disclose whether or not they provide paid sick leave to encourage sick workers to stay home, paid leave for quarantined workers, paid leave at any temporarily closed facilities, and family leave options to provide for childcare or sick family

Health Insurance—Companies should disclose the health insurance coverage ratio of their workforce and whether the company has a policy to provide employer-paid health insurance for any employees who are laid off during the COVID-19 pandemic.

Contingent Workers—Companies should disclose if part-time employees, temporary workers, independent contractors, and subcontracted workers receive all the protections and benefits provided to full-time company employees, including those outlined above.

Supply Chains-Companies should disclose whether they are current on payments to their supply chain vendors. Timely and prompt payments to suppliers will help retain suppliers’ workforces and ensure that a stable supply chain is in place for business operations going forward.

Workers’ Rights-Companies should disclose their policies for protecting employees who raise concerns about workplace health and safety from retaliation, including whistleblower protections and contractual provisions protecting workers’ rights to raise concerns about workplace conditions.

Political activity—Companies should disclose all election spending and lobbying activity, especially money spent through third parties like trade associations and social welfare 501(c)4 organizations.

Prior to the onset of COVID-19, it was often argued that human rights, worker protection and supply chain matters were moral issues not relevant to a company’s financial performance. As millions of workers are laid off and supply chains unravel, the pandemic has proven that view wrong. Businesses that protect workers and consumers will be better positioned to continue operations and respond to consumer demand throughout the pandemic. The disclosures outlined above will provide investors with important information to help them understand how COVID-19 is impacting the companies they are invested in. In addition, by requiring these disclosures, the Commission has the opportunity to encourage companies to review their current practices and consider whether updates are necessary in light of recent events. The process of preparing these disclosures may help some public companies to recognize that their current practices are not sufficiently robust to protect their workers, consumers, supply chains and, as a result, their investors’ capital given the impact of the pandemic.

Des chefs de direction se targuent d’avoir renoncé à une partie de leur salaire dans le contexte de la pandémie, mais leur conseil d’administration pourrait modifier leur régime de rémunération globale pour préserver leur train de vie.

Selon l’agence de presse Associated Press (AP), dans le contexte du dévoilement d’une étude Equilar/AP au sujet de la rémunération de 329 chefs de la direction d’entreprises inscrites à l’indice boursier S&P 500, des investisseurs et actionnaires restent sur leurs gardes, car des CA considèrent revoir les objectifs de performance de leur chef de direction, afin de les rendre plus faciles à atteindre dans le contexte actuel, donc de rendre plus accessibles les incitatifs financiers liés à la performance.

De plus, par exemple, des CA pourraient aussi décider d’octroyer de plus gros blocs d’actions à leur chef de la direction, de manière à « compenser les chutes des valeurs boursières plus tôt cette année, comme plusieurs entreprises avaient fait après la crise financière de 2008 ».

Dans les deux cas, « le risque est que s’il y a un fort rebond du marché, cela pourrait mener à une manne financière », selon la directrice générale adjointe du Council of Institutional Investors, Amy Borrus, citée par l’AP, d’autant plus que « le marché a déjà récupéré plus de la moitié de ses pertes », ajoute l’AP.

De son côté, la firme de gestion d’actifs Vanguard considère que les cibles de performance ne devraient pas être rendues plus faciles à atteindre, parce que les formes de rémunération non garanties devraient demeurer non garanties.

Faire bonne figure

Selon l’AP, la rémunération globale 2020 des chefs de direction sera examinée à la loupe en 2021, par exemple aux assemblées annuelles, par les actionnaires, les investisseurs potentiels et les parties intéressées, comme le public.

« Vous ne pouvez pas être l’organisation qui a mis à pied des employés […] et dont le chef de direction a néanmoins reçu des hausses de salaire et de bonis », selon une associée du cabinet-conseil Compensation Advisory Partners, Melissa Burek, elle aussi citée par l’AP.

Selon Vanguard, les CA devraient considérer la dimension sociale de leurs décisions en matière de rémunération des hauts dirigeants, la manière dont ces décisions seront perçues par le public, ainsi les risques réputationnels pour l’organisation liés à l’octroi au mauvais moment de rémunérations déconnectées de la réalité et du vécu des parties intéressées, comme les employés et la communauté.

Dans un moment si chaotique et incertain, la contribution des actionnaires s’avère essentielle au succès du plan de relance du Canada et du Québec. Une fois cette observation faite, encore faut-il répondre à nombre de questions : que devraient alors faire les actionnaires ? Quelle attitude devraient-ils adopter ? Comment devraient-ils s’engager ? Une idée-force émerge que les Principes d’investissement responsable des Nations unies (PRI) expriment avec netteté : « As for the responsible investment community, it’s time for us to step up and play our role as long-term holders of capital, to call corporations to account ».

(…) Plusieurs positions récemment publiées par les PRI et des organisations d’investisseurs institutionnels (ICGN et ICCR) apportent un précieux éclairage sur le contenu de l’engagement COVID-19 en fournissant des recommandations aux actionnaires. Ces normes de comportement (désignées sous le vocable de « stewardship ») s’organisent autour des éléments suivants :

Rester calme

Se concentrer sur la COVID-19

Défendre une approche de long terme

S’assurer de sécuriser la position des salariés

Abandonner les sacro-saints dividendes

Se montrer financièrement prudent et souple

Maintenir les relations avec leurs fournisseurs et consommateurs

Être vigilant sur la démocratie actionnariale

(…) Alors actionnaires, retenez une chose de la crise sanitaire mondiale : que cela vous plaise ou non, il va falloir sérieusement vous engager. C’est à ce prix que les entreprises vont pouvoir se redresser. Clap de fin pour la responsabilité limitée des actionnaires, même si elle demeure ancrée dans le droit des sociétés par actions !

Corporate social responsibility (CSR) is a concept that notoriously evades definition. Some have said that companies should act in socially responsible ways in their daily operations while charitable donations have historically been brought under this umbrella. The former understanding of CSR is often preferred because simply making charitable donations while doing business in an irresponsible manner causing harm to various stakeholders is clearly undesirable.

India’s company law has a CSR provision requiring companies to donate 2% of their profits from the preceding three years on activities designated by the government. (You can read a detailed analysis of the law in an article by Sandeep Gopalan and me here.) One criticism of such an understanding of CSR is that the meaning restricts itself to charitable donations without venturing into how companies conduct their day to day business.

The coronavirus has given us an unpleasant jolt with which to test if companies are happy to simply comply with the CSR provision and do nothing else to accommodate various stakeholders that are suffering in this crisis. Yet many big businesses in India (Bajaj Auto, Tata Sons, Vedanta Group) promised not to cut salaries of staff during the pandemic. Instead, some companies suggested that they were considering a pay cut for CEOs and other members of the promoter group (the controlling shareholder group in India, typically a family).

(…) When viewed from the perspective of the epidemic, charitable contribution seems like a perfectly valid form of CSR. This is not only because the company is addressing an urgent need at the moment but also because the initiatives have come from individual companies rather than as a response to a forced government mandate of requiring a certain amount of expenditure on CSR activities. The Ministry of Corporate Affairs (MCA) issued an order stating that companies’ responses to the covid crisis could be classified as CSR. The companies Act only allows spending on designated categories to be classified as CSR. Since one of the designated categories is ‘combating human immunodeficiency virus, acquired immune deficiency syndrome, malaria and other diseases’, the order from the MCA was not too surprising. Obviously, India’s rigid definition of CSR means that innovative responses from companies that offered their resorts to be used as temporary care facilities will not be considered CSR.

The lesson to take beyond the pandemic is for the Indian government to resist the urge to intervene in how companies comply with the CSR provision in the law. Allowing companies to be creative and using their CSR activities to gain reputational capital is not a bad idea. In fact, this should be further encouraged by letting companies disclose their social activities along with the CSR disclosures (relating to the required spending) required by the law.