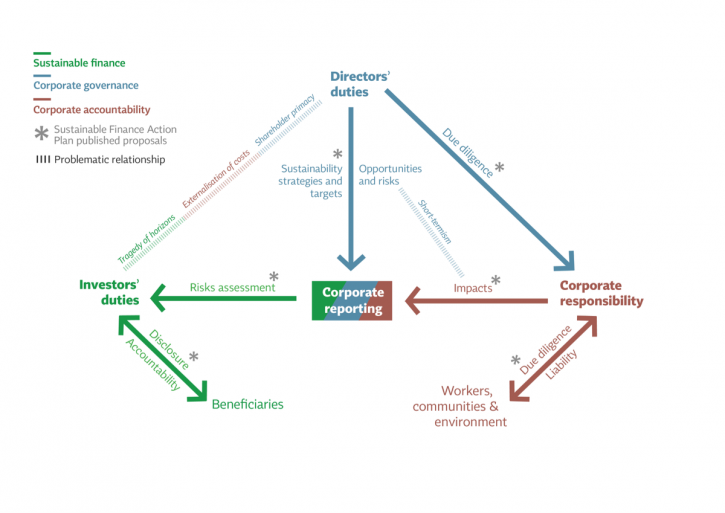

Introduit par les normes de durabilité (ou European sustainability reporting standards – ESRS), l’exercice de double matérialité est la pierre angulaire de la CSRD, nouvelle directive européenne sur le reporting de durabilité.

De par ses niveaux d’exigence et de formalisation, cet exercice requiert de mettre en place une organisation dédiée, mobilisant des ressources humaines voire financières pour en assurer la fiabilité et l’auditabilité. C’est en cela qu’il est important de saisir cette opportunité, pour penser cet exercice au-delà de sa seule fonction réglementaire et en extraire toute la valeur possible.

Comment éviter « l’usine à gaz » et mettre à profit cet exercice pour l’orientation stratégique de l’entreprise ? Comment obtenir une information fiable et auditable ? Comment effectuer cette évaluation de façon engageante, efficace et conforme ?

Intéressante initiative en France de l’ADEME : cette agence propose un guide téléchargeable et un test d’auto-évaluation afin d’aider à comprendre les enjeux d’un message plus responsable, à décrypter la « mécanique du greenwashing » et à se poser les bonnes questions pour réduire les risques de greenwashing.

Ces tests vous aideront à estimer si la qualité et la teneur de votre démarche/produit ou service sont suffisantes pour permettre l’utilisation d’arguments écologique et « développement durable ».

Il s’agit d’un outil de sensibilisation, d’aide à la décision et à la création dans le respect des règles d’une communication plus responsable. Ces tests ne délivrent pas de label et les résultats obtenus ne sont pas des sanctions, mais un mode de sensibilisation à la question du greenwashing, avec des pistes d’amélioration de vos pratiques.

Choisissez le type de message puis le test auquel vous souhaitez répondre. Pour chaque question, sélectionner la lettre correspondant à votre réponse. Les réponses sont additionnées et le résultat permet d’obtenir un « profil ». Tout au long des tests, cliquer sur les termes soulignés pour obtenir un complément d’information.

Excellent travail de l’Institut français des administrateurs (IFA) qui vient de publier un rapport ô combien intéressant : « Le conseil d’administration et l’information extra-financière« .

Si l’information extra-financière a connu une formidable montée en puissance, elle demeure encore en pleine évolution, avec des contours revisités, et ce, dans un contexte où les attentes en interne à l’entreprise comme de la part des parties prenantes externes vont grandissantes. L’information extra-financière s’invite désormais dans tous les aspects de la vie de l’entreprise, et touche à autant d’enjeux qui sont au cœur des missions du Conseil. Ce document synthétise les tendances qui vont structurer l’information extra-financière dans les prochaines années, et sur cette base, formule des recommandations sur les diligences clés à effectuer par le Conseil. Enfin et surtout, ce rapport affiche l’ambition et les convictions de l’IFA quant au rôle déterminant de l’administrateur en matière d’information extra-financière.

Le 21 avril 2021, l’Union européenne a publié une série de mesures touchant la taxonomie, le reporting extra-financier et les devoirs des investisseurs institutionnels.

The Commission adopted a proposal for a Corporate Sustainability Reporting Directive (CSRD), which would amend the existing reporting requirements of the NFRD. The proposal

extends the scope to all large companies and all companies listed on regulated markets (except listed micro-enterprises)

requires the audit (assurance) of reported information

introduces more detailed reporting requirements, and a requirement to report according to mandatory EU sustainability reporting standards

requires companies to digitally ‘tag’ the reported information, so it is machine readable and feeds into the European single access point envisaged in the capital markets union action plan

Blogging for sustainability offre un beau billet sur la construction européenne du reporting extra-financier : « Goodbye, non-financial reporting! A first look at the EU proposal for corporate sustainability reporting » (David Monciardini et Jukka Mähönen, 26 April 2021). Les auteurs soulignent la dernière position de l’Union européenne (celle du 21 avril 2021 qui modifie le cadre réglementaire du reporting extra-financier) et explique pourquoi celle-ci est pertinente. Du mieux certes, mais encore des critiques !

Extrait :

A breakthrough in the long struggle for corporate accountability?

Compared to the NFRD, the new proposal contains several positive developments.

First, the concept of ‘non-financial reporting’, a misnomer that was widely criticised as obscure, meaningless or even misleading, has been abandoned. Finally we can talk about mandatory sustainability reporting, as it should be.

Second, the Commission is introducing sustainability reporting standards, as a common European framework to ensure comparable information. This is a major breakthrough compared to the NFRD that took a generic and principle-based approach. The proposal requires to develop both generic and sector specific mandatory sustainability reporting standards. However, the devil is in the details. The Commission foresees that the development of the new corporate sustainability standards will be undertaken by the European Financial Reporting Advisory Group (EFRAG), a private organisation dominated by the large accounting firms and industry associations. As we discuss below, the most important issue is to prevent the risks of regulatory capture and privatization of EU norms. What is a step forward, though, is the companies’ duty to report on plans to ensure the compatibility of their business models and strategies with the transition towards a zero-emissions economy in line with the Paris Agreement.

Third, the scope of the proposed CSRD is extended to include ‘all large companies’, not only ‘public interest entities’ (listed companies, banks, and insurance companies). According to the Commission, companies covered by the rules would more than triple from 11,000 to around 49,000. However, only listed small and medium-sized enterprises (SMEs) are included in the proposal. This is a major flaw in the proposal as the negative social and environmental impacts of some SMEs’ activities can be very substantial. Large subsidiaries are thereby excluded from the scope, which also is a major weakness. Besides, instead of scaling the general standards to the complexity and size of all undertakings, the Commission proposes a two-tier regime, running the risk of creating a ‘double standard’ that is less stringent for SMEs.

Fourth, of the most welcomed proposals, however, is strengthening a ‘double materiality’ principle for standards (making it ‘enshrined’, according to the Commission), to cover not only just the risks of unsustainability to companies themselves but also the impacts of companies on society and the environment. Similarly, it is positive that the Commission maintains a multi-stakeholder approach, whereas some of the international initiatives in place privilege the information needs of capital providers over other stakeholders (e.g. IIRC; CDP; and more recently the IFRS).

Fifth, a step forward is the compulsory digitalisation of corporate disclosure whereby information is ‘tagged’ according to a categorisation system that will facilitate a wider access to data.

Finally, the proposal introduces for the first time a general EU-wide audit requirement for reported sustainability information, to ensure it is accurate and reliable. However, the proposal is watered down by the introduction of a ‘limited’ assurance requirement instead of a ‘reasonable’ assurance requirement set to full audit. According to the Commission, full audit would require specific sustainability assurance standards they have not yet planned for. The Commission proposes also that the Member States allow firms other than auditors of financial information to assure sustainability information, without standardised assurance processes. Instead, the Commission could have follow on the successful experience of environmental audit schemes, such as EMAS, that employ specifically trained verifiers.

No time for another corporate reporting façade

As others have pointed out, the proposal is a long-overdue step in the right direction. Yet, the draft also has shortcomings, which will need to be remedied if genuine progress is to be made.

In terms of standard-setting governance, the draft directive specifies that standards should be developed through a multi-stakeholder process. However, we believe that such a process requires more than symbolic trade union and civil society involvement. EFRAG shall have its own dedicated budget and staff so to ensure adequate capacity to conduct independent research. Similarly, given the differences between sustainability and financial reporting standards, EFRAG shall permanently incorporate a balanced representation of trade unions, investors, civil society and companies and their organisations, in line with a multi-stakeholder approach.

The proposal is ambiguous in relation to the role of private market-driven initiatives and interest groups. It is crucial that the standards are aligned to the sustainability principles that are written in the EU Treaties and informed by a comprehensive science-based understanding of sustainability. The announcement in January 2020 of the development of EU sustainability reporting standards has been followed by the sudden move by international accounting body the IFRS Foundation to create a global standard setting structure, focusing only on financially material climate-related disclosures. In the months to come, we can expect enormous pressure on EU policy-makers to adopt this privatised and narrower approach, widely criticised by the academic community.

Furthermore, the proposal still represents silo thinking, separating sustainability disclosure from the need to review and reform financial accounting rules (that remain untouched). It still emphasises transparency over governance. Albeit it includes a requirement for companies to report on sustainability due diligence and actual and potential adverse impacts connected with the company’s value chain, it lacks policy coherence. The proposal’s link with DG Justice upcoming legislation on the boards’ sustainability due diligence duties later this year is still tenuous.

After decades of struggles for mandatory high-quality corporate sustainability disclosure, we cannot afford another corporate reporting façade. It is time for real progress towards corporate accountability.

Après les révélations sur l’entreprise, qui avait manipulé son bilan, un projet de loi en discussion souhaite notamment renforcer les pouvoirs du gendarme de la Bourse allemand.

La finance allemande a-t-elle des pratiques malsaines ? Depuis la faillite au mois de juin de l’ancienne star de la finance Wirecard, après qu’elle a reconnu avoir lourdement manipulé son bilan, les révélations sur l’affaire se sont accumulées, soulignant les graves insuffisances du système de contrôle des marchés financiers outre-Rhin. Des manquements qui sont devenus un enjeu politique majeur. Sous pression, le ministre des finances, Olaf Scholz, pousse en faveur d’une réforme rapide du système. Son projet de loi, en discussion depuis mercredi 21 octobre dans les ministères, doit être voté « avant l’été », a-t-il annoncé.

Le texte, porté également par la ministre de la justice, Christine Lambrecht, révèle en creux les limites de l’approche allemande en matière de surveillance des entreprises cotées, et le tournant culturel amorcé par le scandale Wirecard. Le système reposait jusqu’ici sur la responsabilisation et la participation consensuelle des sociétés au processus de contrôle des bilans. L’examen des comptes était confié non pas à la BaFin, le gendarme allemand de la Bourse, mais à une association privée, la DPR (« organisme de contrôle des bilans »), qui disposait de très peu de moyens réels. L’affaire Wirecard a montré l’impuissance de cette approche dans le cas d’une fraude délibérément orchestrée. La future loi doit renforcer considérablement les pouvoirs de la BaFin, qui disposera d’un droit d’investigation pour examiner elle-même les bilans des entreprise

(…) Les cabinets d’audit, dont le manque de zèle à alerter sur les irrégularités de bilan a été mis au jour par le scandale, devront aussi se soumettre à une réforme. Leur mandat au service d’une même entreprise ne pourra excéder dix ans. Le projet de loi exige qu’une séparation plus nette soit faite, au sein de ces cabinets, entre leur activité d’audit et leur activité de conseil, afin d’éviter les conflits d’intérêts.

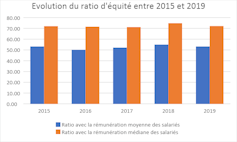

Bel article de Vanessa Serret et Mohamed Khemissi dans The conversation (27 juillet 2020) : « Rémunération des dirigeants : la transparence ne fait pas tout ». Cet article revient sur le ratio d’équité : non seulement son utilité, mais encore son niveau (20 ? 100 ?…)

Le ratio d’équité apprécie l’écart entre la rémunération de chaque dirigeant et le salaire (moyen et médian) des salariés à temps plein de son entreprise. Il est prévu un suivi de l’évolution de ce ratio au cours des cinq derniers exercices et sa mise en perspective avec la performance financière de la société. Ces comparaisons renseignent sur la dynamique du partage de la création de valeur entre le dirigeant et les salariés.

(…)

Un premier état des lieux

Sur la base des rémunérations versées en 2019 par les entreprises composant l’indice boursier du CAC 40, les patrons français ont perçu un salaire moyen de 5 millions d’euros, soit une baisse de 9,1 % par rapport à 2018.

Évolution du ratio d’équité par rapport à la rémunération moyenne (bleu) et médiane (orange) des salariés de 2015 à 2019. auteurs

Ce chiffre représente 53 fois la rémunération moyenne de leurs employés (72 fois la rémunération médiane) : un ratio acceptable, selon l’agence de conseil en vote Proxinvest. En effet, selon cette agence, et afin de garantir la cohésion sociale au sein de l’entreprise, le ratio d’équité ne doit pas dépasser 100 (par rapport à la rémunération moyenne des salariés).

Deux dirigeants s’attribuent néanmoins des rémunérations qui dépassent le maximum socialement tolérable à savoir Bernard Charlès, vice-président du conseil d’administration et directeur général de Dassault Systèmes et Paul Hudson, directeur général de Sanofi avec un ratio d’équité qui s’établit respectivement de 268 et de 107.

Notons également que pour les deux sociétés publiques appartenant à l’indice boursier du CAC 40, le ratio d’équité dépasse le plafond de 20 (35 pour Engie et 38 pour Orange) fixé par le décret n° 2012-915 du 26 juillet 2012, relatif au contrôle de l’État sur les rémunérations des dirigeants d’entreprises publiques.