Les adieux au reporting extra-financier… vraiment ?

Blogging for sustainability offre un beau billet sur la construction européenne du reporting extra-financier : « Goodbye, non-financial reporting! A first look at the EU proposal for corporate sustainability reporting » (David Monciardini et Jukka Mähönen, 26 April 2021). Les auteurs soulignent la dernière position de l’Union européenne (celle du 21 avril 2021 qui modifie le cadre réglementaire du reporting extra-financier) et explique pourquoi celle-ci est pertinente. Du mieux certes, mais encore des critiques !

Compared to the NFRD, the new proposal contains several positive developments.

First, the concept of ‘non-financial reporting’, a misnomer that was widely criticised as obscure, meaningless or even misleading, has been abandoned. Finally we can talk about mandatory sustainability reporting, as it should be.

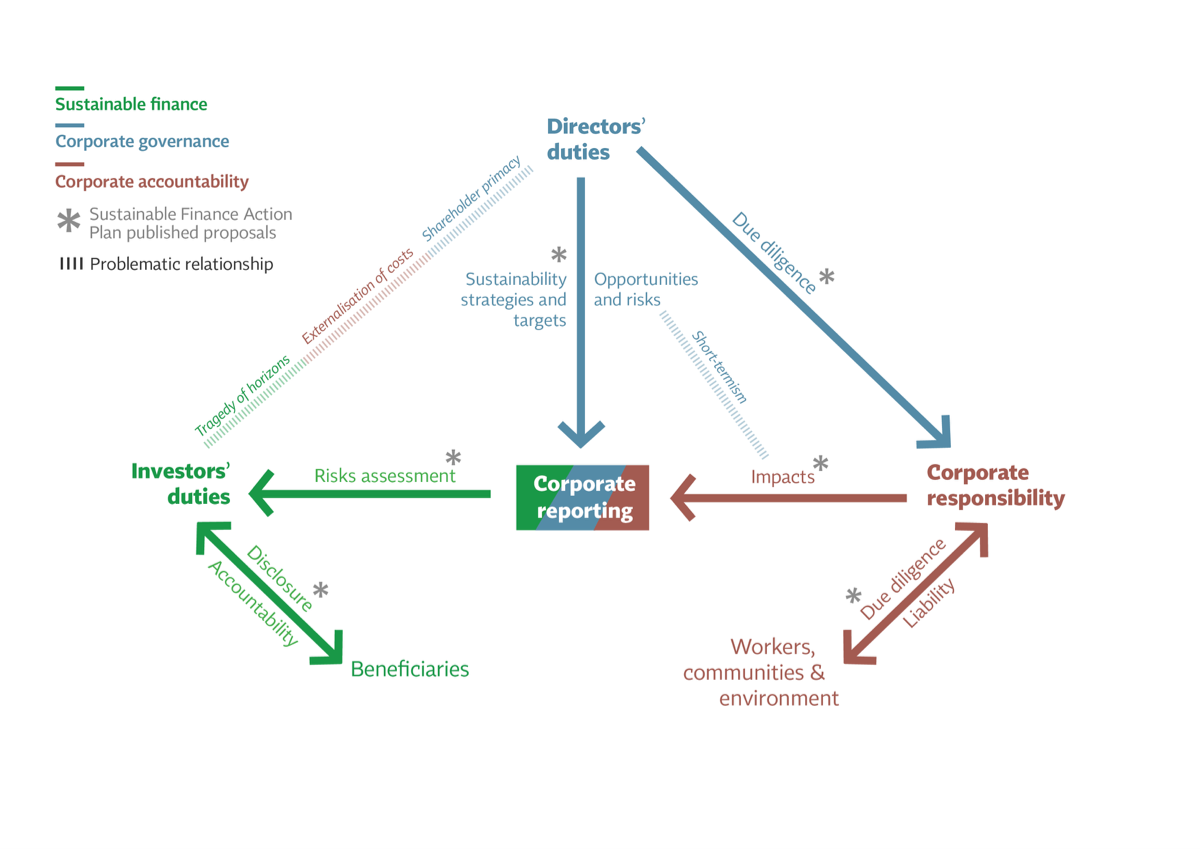

Second, the Commission is introducing sustainability reporting standards, as a common European framework to ensure comparable information. This is a major breakthrough compared to the NFRD that took a generic and principle-based approach. The proposal requires to develop both generic and sector specific mandatory sustainability reporting standards. However, the devil is in the details. The Commission foresees that the development of the new corporate sustainability standards will be undertaken by the European Financial Reporting Advisory Group (EFRAG), a private organisation dominated by the large accounting firms and industry associations. As we discuss below, the most important issue is to prevent the risks of regulatory capture and privatization of EU norms. What is a step forward, though, is the companies’ duty to report on plans to ensure the compatibility of their business models and strategies with the transition towards a zero-emissions economy in line with the Paris Agreement.

Third, the scope of the proposed CSRD is extended to include ‘all large companies’, not only ‘public interest entities’ (listed companies, banks, and insurance companies). According to the Commission, companies covered by the rules would more than triple from 11,000 to around 49,000. However, only listed small and medium-sized enterprises (SMEs) are included in the proposal. This is a major flaw in the proposal as the negative social and environmental impacts of some SMEs’ activities can be very substantial. Large subsidiaries are thereby excluded from the scope, which also is a major weakness. Besides, instead of scaling the general standards to the complexity and size of all undertakings, the Commission proposes a two-tier regime, running the risk of creating a ‘double standard’ that is less stringent for SMEs.

Fourth, of the most welcomed proposals, however, is strengthening a ‘double materiality’ principle for standards (making it ‘enshrined’, according to the Commission), to cover not only just the risks of unsustainability to companies themselves but also the impacts of companies on society and the environment. Similarly, it is positive that the Commission maintains a multi-stakeholder approach, whereas some of the international initiatives in place privilege the information needs of capital providers over other stakeholders (e.g. IIRC; CDP; and more recently the IFRS).

Fifth, a step forward is the compulsory digitalisation of corporate disclosure whereby information is ‘tagged’ according to a categorisation system that will facilitate a wider access to data.

Finally, the proposal introduces for the first time a general EU-wide audit requirement for reported sustainability information, to ensure it is accurate and reliable. However, the proposal is watered down by the introduction of a ‘limited’ assurance requirement instead of a ‘reasonable’ assurance requirement set to full audit. According to the Commission, full audit would require specific sustainability assurance standards they have not yet planned for. The Commission proposes also that the Member States allow firms other than auditors of financial information to assure sustainability information, without standardised assurance processes. Instead, the Commission could have follow on the successful experience of environmental audit schemes, such as EMAS, that employ specifically trained verifiers.

As others have pointed out, the proposal is a long-overdue step in the right direction. Yet, the draft also has shortcomings, which will need to be remedied if genuine progress is to be made.

In terms of standard-setting governance, the draft directive specifies that standards should be developed through a multi-stakeholder process. However, we believe that such a process requires more than symbolic trade union and civil society involvement. EFRAG shall have its own dedicated budget and staff so to ensure adequate capacity to conduct independent research. Similarly, given the differences between sustainability and financial reporting standards, EFRAG shall permanently incorporate a balanced representation of trade unions, investors, civil society and companies and their organisations, in line with a multi-stakeholder approach.

The proposal is ambiguous in relation to the role of private market-driven initiatives and interest groups. It is crucial that the standards are aligned to the sustainability principles that are written in the EU Treaties and informed by a comprehensive science-based understanding of sustainability. The announcement in January 2020 of the development of EU sustainability reporting standards has been followed by the sudden move by international accounting body the IFRS Foundation to create a global standard setting structure, focusing only on financially material climate-related disclosures. In the months to come, we can expect enormous pressure on EU policy-makers to adopt this privatised and narrower approach, widely criticised by the academic community.

Furthermore, the proposal still represents silo thinking, separating sustainability disclosure from the need to review and reform financial accounting rules (that remain untouched). It still emphasises transparency over governance. Albeit it includes a requirement for companies to report on sustainability due diligence and actual and potential adverse impacts connected with the company’s value chain, it lacks policy coherence. The proposal’s link with DG Justice upcoming legislation on the boards’ sustainability due diligence duties later this year is still tenuous.

After decades of struggles for mandatory high-quality corporate sustainability disclosure, we cannot afford another corporate reporting façade. It is time for real progress towards corporate accountability.

À la prochaine…

Ce contenu a été mis à jour le 30 mars 2022 à 5 h 54 min.

Commentaires