actualités internationales

actualités internationales divulgation extra-financière normes de droit Responsabilité sociale des entreprises

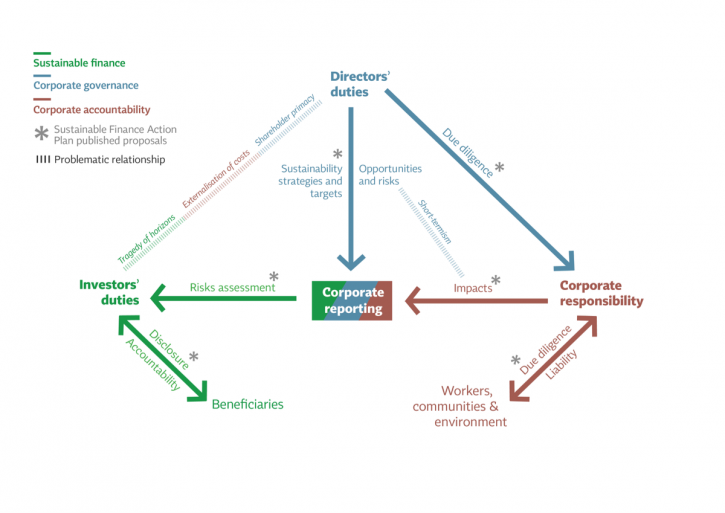

Double matérialité des enjeux de durabilité : quels défis relever pour se préparer à la CSRD ?

Ivan Tchotourian 14 mai 2024

C’est sous ce titre qu’Audencia – IFACI – Orse – PwC publie un rapport à lire tant il est pertinent.

Résumé :

Introduit par les normes de durabilité (ou European sustainability reporting standards – ESRS), l’exercice de double matérialité est la pierre angulaire de la CSRD, nouvelle directive européenne sur le reporting de durabilité.

De par ses niveaux d’exigence et de formalisation, cet exercice requiert de mettre en place une organisation dédiée, mobilisant des ressources humaines voire financières pour en assurer la fiabilité et l’auditabilité. C’est en cela qu’il est important de saisir cette opportunité, pour penser cet exercice au-delà de sa seule fonction réglementaire et en extraire toute la valeur possible.

Comment éviter « l’usine à gaz » et mettre à profit cet exercice pour l’orientation stratégique de l’entreprise ? Comment obtenir une information fiable et auditable ? Comment effectuer cette évaluation de façon engageante, efficace et conforme ?

À la prochaine…

actualités internationales Divulgation divulgation extra-financière Gouvernance mission et composition du conseil d'administration Nouvelles diverses Responsabilité sociale des entreprises

Le conseil d’administration et l’information extra-financière : rapport de l’IFA

Ivan Tchotourian 12 mai 2021 Ivan Tchotourian

Excellent travail de l’Institut français des administrateurs (IFA) qui vient de publier un rapport ô combien intéressant : « Le conseil d’administration et l’information extra-financière« .

- Pour se le procurer : ici

Résumé :

Si l’information extra-financière a connu une formidable montée en puissance, elle demeure encore en pleine évolution, avec des contours revisités, et ce, dans un contexte où les attentes en interne à l’entreprise comme de la part des parties prenantes externes vont grandissantes. L’information extra-financière s’invite désormais dans tous les aspects de la vie de l’entreprise, et touche à autant d’enjeux qui sont au cœur des missions du Conseil. Ce document synthétise les tendances qui vont structurer l’information extra-financière dans les prochaines années, et sur cette base, formule des recommandations sur les diligences clés à effectuer par le Conseil. Enfin et surtout, ce rapport affiche l’ambition et les convictions de l’IFA quant au rôle déterminant de l’administrateur en matière d’information extra-financière.

À la prochaine…

actualités internationales Divulgation divulgation extra-financière normes de droit Responsabilité sociale des entreprises

Proposal for a Corporate Sustainability Reporting Directive (CSRD)

Ivan Tchotourian 29 avril 2021 Ivan Tchotourian

Le 21 avril 2021, l’Union européenne a publié une série de mesures touchant la taxonomie, le reporting extra-financier et les devoirs des investisseurs institutionnels.

Éléments essentiels :

The Commission adopted a proposal for a Corporate Sustainability Reporting Directive (CSRD), which would amend the existing reporting requirements of the NFRD. The proposal

- extends the scope to all large companies and all companies listed on regulated markets (except listed micro-enterprises)

- requires the audit (assurance) of reported information

- introduces more detailed reporting requirements, and a requirement to report according to mandatory EU sustainability reporting standards

- requires companies to digitally ‘tag’ the reported information, so it is machine readable and feeds into the European single access point envisaged in the capital markets union action plan

À la prochaine…

actualités internationales Divulgation divulgation extra-financière Gouvernance normes de droit

Les adieux au reporting extra-financier… vraiment ?

Ivan Tchotourian 29 avril 2021 Ivan Tchotourian

Blogging for sustainability offre un beau billet sur la construction européenne du reporting extra-financier : « Goodbye, non-financial reporting! A first look at the EU proposal for corporate sustainability reporting » (David Monciardini et Jukka Mähönen, 26 April 2021). Les auteurs soulignent la dernière position de l’Union européenne (celle du 21 avril 2021 qui modifie le cadre réglementaire du reporting extra-financier) et explique pourquoi celle-ci est pertinente. Du mieux certes, mais encore des critiques !

Extrait :

A breakthrough in the long struggle for corporate accountability?

Compared to the NFRD, the new proposal contains several positive developments.

First, the concept of ‘non-financial reporting’, a misnomer that was widely criticised as obscure, meaningless or even misleading, has been abandoned. Finally we can talk about mandatory sustainability reporting, as it should be.

Second, the Commission is introducing sustainability reporting standards, as a common European framework to ensure comparable information. This is a major breakthrough compared to the NFRD that took a generic and principle-based approach. The proposal requires to develop both generic and sector specific mandatory sustainability reporting standards. However, the devil is in the details. The Commission foresees that the development of the new corporate sustainability standards will be undertaken by the European Financial Reporting Advisory Group (EFRAG), a private organisation dominated by the large accounting firms and industry associations. As we discuss below, the most important issue is to prevent the risks of regulatory capture and privatization of EU norms. What is a step forward, though, is the companies’ duty to report on plans to ensure the compatibility of their business models and strategies with the transition towards a zero-emissions economy in line with the Paris Agreement.

Third, the scope of the proposed CSRD is extended to include ‘all large companies’, not only ‘public interest entities’ (listed companies, banks, and insurance companies). According to the Commission, companies covered by the rules would more than triple from 11,000 to around 49,000. However, only listed small and medium-sized enterprises (SMEs) are included in the proposal. This is a major flaw in the proposal as the negative social and environmental impacts of some SMEs’ activities can be very substantial. Large subsidiaries are thereby excluded from the scope, which also is a major weakness. Besides, instead of scaling the general standards to the complexity and size of all undertakings, the Commission proposes a two-tier regime, running the risk of creating a ‘double standard’ that is less stringent for SMEs.

Fourth, of the most welcomed proposals, however, is strengthening a ‘double materiality’ principle for standards (making it ‘enshrined’, according to the Commission), to cover not only just the risks of unsustainability to companies themselves but also the impacts of companies on society and the environment. Similarly, it is positive that the Commission maintains a multi-stakeholder approach, whereas some of the international initiatives in place privilege the information needs of capital providers over other stakeholders (e.g. IIRC; CDP; and more recently the IFRS).

Fifth, a step forward is the compulsory digitalisation of corporate disclosure whereby information is ‘tagged’ according to a categorisation system that will facilitate a wider access to data.

Finally, the proposal introduces for the first time a general EU-wide audit requirement for reported sustainability information, to ensure it is accurate and reliable. However, the proposal is watered down by the introduction of a ‘limited’ assurance requirement instead of a ‘reasonable’ assurance requirement set to full audit. According to the Commission, full audit would require specific sustainability assurance standards they have not yet planned for. The Commission proposes also that the Member States allow firms other than auditors of financial information to assure sustainability information, without standardised assurance processes. Instead, the Commission could have follow on the successful experience of environmental audit schemes, such as EMAS, that employ specifically trained verifiers.

No time for another corporate reporting façade

As others have pointed out, the proposal is a long-overdue step in the right direction. Yet, the draft also has shortcomings, which will need to be remedied if genuine progress is to be made.

In terms of standard-setting governance, the draft directive specifies that standards should be developed through a multi-stakeholder process. However, we believe that such a process requires more than symbolic trade union and civil society involvement. EFRAG shall have its own dedicated budget and staff so to ensure adequate capacity to conduct independent research. Similarly, given the differences between sustainability and financial reporting standards, EFRAG shall permanently incorporate a balanced representation of trade unions, investors, civil society and companies and their organisations, in line with a multi-stakeholder approach.

The proposal is ambiguous in relation to the role of private market-driven initiatives and interest groups. It is crucial that the standards are aligned to the sustainability principles that are written in the EU Treaties and informed by a comprehensive science-based understanding of sustainability. The announcement in January 2020 of the development of EU sustainability reporting standards has been followed by the sudden move by international accounting body the IFRS Foundation to create a global standard setting structure, focusing only on financially material climate-related disclosures. In the months to come, we can expect enormous pressure on EU policy-makers to adopt this privatised and narrower approach, widely criticised by the academic community.

Furthermore, the proposal still represents silo thinking, separating sustainability disclosure from the need to review and reform financial accounting rules (that remain untouched). It still emphasises transparency over governance. Albeit it includes a requirement for companies to report on sustainability due diligence and actual and potential adverse impacts connected with the company’s value chain, it lacks policy coherence. The proposal’s link with DG Justice upcoming legislation on the boards’ sustainability due diligence duties later this year is still tenuous.

After decades of struggles for mandatory high-quality corporate sustainability disclosure, we cannot afford another corporate reporting façade. It is time for real progress towards corporate accountability.

À la prochaine…

actualités internationales Divulgation divulgation extra-financière Gouvernance Normes d'encadrement normes de droit normes de marché Responsabilité sociale des entreprises

Approche juridique sur la transparence ESG

Ivan Tchotourian 3 août 2020 Ivan Tchotourian

Excellente lecture ce matin de ce billet du Harvard Law School Forum on Corporate Governance : « Legal Liability for ESG Disclosures » (de Connor Kuratek, Joseph A. Hall et Betty M. Huber, 3 août 2020). Dans cette publication, vous trouverez non seulement une belle synthèse des référentiels actuels, mais aussi une réflexion sur les conséquences attachées à la mauvaise divulgation d »information.

Extrait :

3. Legal Liability Considerations

Notwithstanding the SEC’s position that it will not—at this time—mandate additional climate or ESG disclosure, companies must still be mindful of the potential legal risks and litigation costs that may be associated with making these disclosures voluntarily. Although the federal securities laws generally do not require the disclosure of ESG data except in limited instances, potential liability may arise from making ESG-related disclosures that are materially misleading or false. In addition, the anti-fraud provisions of the federal securities laws apply not only to SEC filings, but also extend to less formal communications such as citizenship reports, press releases and websites. Lastly, in addition to potential liability stemming from federal securities laws, potential liability could arise from other statutes and regulations, such as federal and state consumer protection laws.

A. Federal Securities Laws

When they arise, claims relating to a company’s ESG disclosure are generally brought under Section 11 of the Securities Act of 1933, which covers material misstatements and omissions in securities offering documents, and under Section 10(b) of the Securities Exchange Act of 1934 and rule 10b-5, the principal anti-fraud provisions. To date, claims brought under these two provisions have been largely unsuccessful. Cases that have survived the motion to dismiss include statements relating to cybersecurity (which many commentators view as falling under the “S” or “G” of ESG), an oil company’s safety measures, mine safety and internal financial integrity controls found in the company’s sustainability report, website, SEC filings and/or investor presentations.

Interestingly, courts have also found in favor of plaintiffs alleging rule 10b-5 violations for statements made in a company’s code of conduct. Complaints, many of which have been brought in the United States District Court for the Southern District of New York, have included allegations that a company’s code of conduct falsely represented company standards or that public comments made by the company about the code misleadingly publicized the quality of ethical controls. In some circumstances, courts found that statements about or within such codes were more than merely aspirational and did not constitute inactionable puffery, including when viewed in context rather than in isolation. In late March 2020, for example, a company settled a securities class action for $240 million alleging that statements in its code of conduct and code of ethics were false or misleading. The facts of this case were unusual, but it is likely that securities plaintiffs will seek to leverage rulings from the court in that class action to pursue other cases involving code of conducts or ethics. It remains to be seen whether any of these code of conduct case holdings may in the future be extended to apply to cases alleging 10b-5 violations for statements made in a company’s ESG reports.

B. State Consumer Protection Laws

Claims under U.S. state consumer protection laws have been of limited success. Nevertheless, many cases have been appealed which has resulted in additional litigation costs in circumstances where these costs were already significant even when not appealed. Recent claims that were appealed, even if ultimately failed, and which survived the motion to dismiss stage, include claims brought under California’s consumer protection laws alleging that human right commitments on a company website imposed on such company a duty to disclose on its labels that it or its supply chain could be employing child and/or forced labor. Cases have also been dismissed for lack of causal connection between alleged violation and economic injury including a claim under California, Florida and Texas consumer protection statutes alleging that the operator of several theme parks failed to disclose material facts about its treatment of orcas. The case was appealed to the U.S. Court of Appeals for the Ninth Circuit, but was dismissed for failure to show a causal connection between the alleged violation and the plaintiffs’ economic injury.

Overall, successful litigation relating to ESG disclosures is still very much a rare occurrence. However, this does not mean that companies are therefore insulated from litigation risk. Although perhaps not ultimately successful, merely having a claim initiated against a company can have serious reputational damage and may cause a company to incur significant litigation and public relations costs. The next section outlines three key takeaways and related best practices aimed to reduce such risks.

C. Practical Recommendations

Although the above makes clear that ESG litigation to date is often unsuccessful, companies should still be wary of the significant impacts of such litigation. The following outlines some key takeaways and best practices for companies seeking to continue ESG disclosure while simultaneously limiting litigation risk.

Key Takeaway 1: Disclaimers are Critical

As more and more companies publish reports on ESG performance, like disclaimers on forward-looking statements in SEC filings, companies are beginning to include disclaimers in their ESG reports, which disclaimers may or may not provide protection against potential litigation risks. In many cases, the language found in ESG reports will mirror language in SEC filings, though some companies have begun to tailor them specifically to the content of their ESG reports.

From our limited survey of companies across four industries that receive significant pressure to publish such reports—Banking, Chemicals, Oil & Gas and Utilities & Power—the following preliminary conclusions were drawn:

- All companies surveyed across all sectors have some type of “forward-looking statement” disclaimer in their SEC filings; however, these were generic disclaimers that were not tailored to ESG-specific facts and topics or relating to items discussed in their ESG reports.

- Most companies had some sort of disclaimer in their Sustainability Report, although some were lacking one altogether. Very few companies had disclaimers that were tailored to the specific facts and topics discussed in their ESG reports:

- In the Oil & Gas industry, one company surveyed had a tailored ESG disclaimer in its ESG Report; all others had either the same disclaimer as in SEC filings or a shortened version that was generally very broad.

- In the Banking industry, two companies lacked disclaimers altogether, but the rest had either their SEC disclaimer or a shortened version.

- In the Utilities & Power industry, one company had no disclaimer, but the rest had general disclaimers.

- In the Chemicals industry, three companies had no disclaimer in their reports, but the rest had shortened general disclaimers.

- There seems to be a disconnect between the disclaimers being used in SEC filings and those found in ESG In particular, ESG disclaimers are generally shorter and will often reference more detailed disclaimers found in SEC filings.

Best Practices: When drafting ESG disclaimers, companies should:

- Draft ESG disclaimers carefully. ESG disclaimers should be drafted in a way that explicitly covers ESG data so as to reduce the risk of litigation.

- State that ESG data is non-GAAP. ESG data is usually non-GAAP and non-audited; this should be made clear in any ESG Disclaimer.

- Have consistent disclaimers. Although disclaimers in SEC filings appear to be more detailed, disclaimers across all company documents that reference ESG data should specifically address these issues. As more companies start incorporating ESG into their proxies and other SEC filings, it is important that all language follows through.

Key Takeaway 2: ESG Reporting Can Pose Risks to a Company

This article highlighted the clear risks associated with inattentive ESG disclosure: potential litigation; bad publicity; and significant costs, among other things.

Best Practices: Companies should ensure statements in ESG reports are supported by fact or data and should limit overly aspirational statements. Representations made in ESG Reports may become actionable, so companies should disclose only what is accurate and relevant to the company.

Striking the right balance may be difficult; many companies will under-disclose, while others may over-disclose. Companies should therefore only disclose what is accurate and relevant to the company. The US Chamber of Commerce, in their ESG Reporting Best Practices, suggests things in a similar vein: do not include ESG metrics into SEC filings; only disclose what is useful to the intended audience and ensure that ESG reports are subject to a “rigorous internal review process to ensure accuracy and completeness.”

Key Takeaway 3: ESG Reporting Can Also be Beneficial for Companies

The threat of potential litigation should not dissuade companies from disclosing sustainability frameworks and metrics. Not only are companies facing investor pressure to disclose ESG metrics, but such disclosure may also incentivize companies to improve internal risk management policies, internal and external decisional-making capabilities and may increase legal and protection when there is a duty to disclose. Moreover, as ESG investing becomes increasingly popular, it is important for companies to be aware that robust ESG reporting, which in turn may lead to stronger ESG ratings, can be useful in attracting potential investors.

Best Practices: Companies should try to understand key ESG rating and reporting methodologies and how they match their company profile.

The growing interest in ESG metrics has meant that the number of ESG raters has grown exponentially, making it difficult for many companies to understand how each “rater” calculates a company’s ESG score. Resources such as the Better Alignment Project run by the Corporate Reporting Dialogue, strive to better align corporate reporting requirements and can give companies an idea of how frameworks such as CDP, CDSB, GRI and SASB overlap. By understanding the current ESG market raters and methodologies, companies will be able to better align their ESG disclosures with them. The U.S. Chamber of Commerce report noted above also suggests that companies should “engage with their peers and investors to shape ESG disclosure frameworks and standards that are fit for their purpose.”

À la prochaine…

actualités internationales Divulgation divulgation extra-financière finance sociale et investissement responsable Gouvernance Normes d'encadrement Responsabilité sociale des entreprises

Il faut améliorer l’information non financière

Ivan Tchotourian 6 juin 2020 Ivan Tchotourian

Pour M. Ben Aamar et Mme Martinez, il faut que les entreprises doivent dépasser le « greenwashing » pour informer les investisseurs sur la résilience de leur modèle économique aux chocs environnementaux. Je vous invite à lire leur tribune : « Améliorer l’information environnementale des investisseurs doit devenir une priorité « (Le Monde, 5 juin 2020).

Extrait :

La pandémie actuelle peut aboutir à une prise de conscience collective et à un renforcement de la lutte contre les causes du dérèglement climatique, ou bien, au contraire, à une mise entre parenthèses des initiatives en ce sens, car l’attention ainsi que toutes les ressources financières seront consacrées à des mesures de relance économique. La cause climatique passerait alors au second plan face à l’urgence, avec, à terme, des conséquences désastreuses.

Le rôle des gouvernants est majeur. Mais pour orienter correctement les flux financiers, publics comme privés, améliorer l’information environnementale des investisseurs doit également devenir une priorité. Le sujet est peu connu du grand public car d’apparence technique. Pourtant, les enjeux sont considérables.

À la prochaine…

actualités internationales Divulgation divulgation extra-financière Gouvernance Normes d'encadrement Nouvelles diverses Responsabilité sociale des entreprises

Rapport français sur la communication non financière des grandes entreprises

Ivan Tchotourian 14 novembre 2019 Ivan Tchotourian

L’AMF France vient de publier son 3e rapport sur la communication des informations non financières.

Résumé :

A l’occasion de son nouveau rapport sur la responsabilité sociale, sociétale et environnementale des sociétés cotées, l’AMF a mené une analyse sur les premières déclarations de performance extra-financière (DPEF) de 24 sociétés cotées françaises. Pour mieux les guider dans cette démarche vers une économie plus durable, le régulateur détaille les enjeux clés de ce reporting extra-financier.

Dans le cadre de sa stratégie 2018-2022, l’AMF a fait de la finance durable un axe prioritaire pour accompagner et encourager l’ensemble du système financier dans sa transition. La qualité des données environnementales et sociales et donc de l’information extra-financière des sociétés cotées constitue un préalable à une telle avancée : elle est indispensable à la décision des investisseurs et au suivi, par ces derniers, de leur politique d’engagement. Pour la quatrième édition de son rapport sur la responsabilité sociale, sociétale et environnementale des sociétés cotées, l’AMF s’est ainsi fixée pour objectif d’accompagner les entreprises dans l’élaboration de leurs futures déclarations de performance extra-financière.

Dans le cadre de leur rapport de gestion pour l’exercice 2018, les entreprises devaient cette année, pour la première fois, élaborer cette déclaration. L’AMF a passé en revue l’information fournie dans la section dédiée à cette déclaration dans leur document de référence par un échantillon de 19 sociétés appartenant à l’indice CAC 40 et de 5 sociétés du SBF 120.

Exemples à l’appui, l’AMF détaille les enjeux d’une communication extra-financière de qualité, que sont :

- la structure, la concision et la cohérence d’ensemble de cette déclaration ;

- le respect des dispositions légales concernant le périmètre de reporting, élargi le cas échéant pour prendre en compte les spécificités du modèle d’affaires ;

- l’information sur le processus d’identification des enjeux et risques extra-financiers, et sur l’horizon de temps auquel ces risques peuvent se matérialiser, ainsi que leurs impacts éventuels ;

- le choix d’indicateurs clés de performance pertinents et justifiés pour illustrer les politiques mises en place ;

- la détermination d’objectifs pour mesurer les progrès réalisés dans le cadre illustrer des politiques mises en place.

Pistes de réflexion pour le cadre européen

Afin d’analyser l’information extra-financière disponible chez plusieurs émetteurs européens du même secteur et de constater dans quelle mesure une convergence des pratiques s’opère, le rapport consacre par ailleurs un chapitre à une comparaison internationale réalisée sur le secteur pétrolier. Les 9 constats issus de cette étude dessinent des pistes de réflexion pour l’avenir du reporting extra-financier comme par exemple la nécessité d’encourager, au niveau européen, une meilleure harmonisation des méthodologies sous-jacentes aux indicateurs de performance extra-financiers.

À la prochaine…