Responsabilité sociale des entreprises | Page 33

Gouvernance Normes d'encadrement objectifs de l'entreprise Responsabilité sociale des entreprises Valeur actionnariale vs. sociétale

From Shareholder Primacy to Stakeholder Capitalism

Ivan Tchotourian 26 octobre 2020 Ivan Tchotourian

Billet à lire de Frederick Alexander et al. : « From Shareholder Primacy to Stakeholder Capitalism » (Harvard Law School Forum on Corporate Governance, 26 octobre 2020).

Extrait :

This policy agenda includes the following categories of interventions required for a broad transition to Stakeholder Capitalism.

We have drafted proposed Federal legislative language, “The Stakeholder Capitalism Act,” attached in Exhibit A of the full paper linked to below, which incorporates each of the following ideas:

Responsible Institutions: We propose that the trustees of institutional investors be required to consider certain economic, social, and environmental effects of their decisions on the interests of their beneficiaries with respect to stewardship of companies within their portfolios. This clarified understanding of fiduciary duty will ensure that institutional investors use their authority to further the real interests of those beneficiaries who have stakes in all aspects of the economy, environment, and society. These changes can be achieved through an amendment to the Investment Company Act of 1940 (15 U.S.C. 80a) by inserting language after paragraph (54) of Section 2 and after subsection (c) of Section 36.

Responsible Companies: Just as trustees of invested funds must expand their notion of the interests of their beneficiaries, the companies in which they invest must also expand the understanding of the interests of the economic owners of their shares, who are more often than not those same beneficiaries. We propose a federal requirement that any corporation or other business entity involved in interstate commerce be formed under a state statute that requires directors and officers to account for the impact of corporate actions not only on financial returns, but also on the viability of the social, natural, and political systems that affect all stakeholders. This change can be achieved through the addition of a new Chapter 2F of Title 15 of the U.S. Code.

Tools for Institutional Accountability: In order to allow beneficiaries to hold institutional investors accountable for the impact of their stewardship on all the interests of beneficiaries, we propose laws that mandate disclosure as to how they are meeting their responsibility to consider these broad interests, including disclosure of proxy voting and engagement with companies. We propose that the Securities and Exchange Commission should promulgate rules requiring each investment company and each employee benefit plan required to file an annual report under section 103 of the Employee Retirement Income Security Act of 1974.

Tools for Company Accountability: Corporate and securities laws that govern businesses must also be changed in order to give institutional investors the tools to meet their enhanced responsibilities. This will include requiring large companies to meet new standards for disclosure regarding stakeholder impact as an important element of their accountability. This proposal can be achieved through an amendment added to The Securities Exchange Act of 1934 (15 U.S.C. 78a et seq.) after section 13A.

(…)

This tension cannot be wished away. The White Paper proposes a solution: rules that facilitate and encourage investor-sanctioned guardrails. Such guardrails would allow shareholders to insist that all companies that they own forgo profits earned through the exploitation of people and planet. Unlike executives, the institutional shareholders who control the markets are diversified, so that their success rises and falls with the success of the economy, rather than any single company. This means that these institutions suffer when individual companies pursue profits with practices that harm the economy. We believe that by leveling the competitive playing field, these changes will pave the way for the type of corporate behavior imagined by the New Paradigm, the Davos Manifesto and the Business Roundtable Statement.

Indeed, far from being “state corporatism,” as the memo claims, what we propose is “human capitalism,” where the workers, citizens, and other humans whose savings fund corporations are given a say in the kind of world they live in. Will it be one in which all compete in a manner that rejects unjust profits? Or, in contrast, will it be one in which corporations continue to lobby against regulation that protects workers while the corporate executives make 300 times the median salary of workers?

À la prochaine…

Gouvernance Responsabilité sociale des entreprises Valeur actionnariale vs. sociétale

Missing in Friedman’s Shareholder Value Maximization Credo: The Shareholders

Ivan Tchotourian 25 septembre 2020 Ivan Tchotourian

Luca Enriques a publié un intéressant billet sur l’Oxford Business Law Blog : « Missing in Friedman’s Shareholder Value Maximization Credo: The Shareholders » (25 septembre 2020).

Extrait :

What Friedman’s Essay Says

As Alex Edmans has noted here,

‘Friedman’s article is widely misquoted and misunderstood. Indeed, thousands of people may have cited it without reading past the title. They think they don’t need to, because the title already makes his stance clear: companies should maximize profits by price-gouging customers, underpaying workers, and polluting the environment’.

That is not, of course, what Friedman wrote. According to Friedman:

- Talking about the ‘social responsibility of business’ makes no sense because the responsibility lies with people. Public corporations are legal persons and may have their responsibilities, but they act through their directors and managers. Therefore, attention must be focused on the responsibilities of such players.

- Managers are employees of corporations, which in turn are owned by their shareholders. Therefore, managers must act in accordance with the wishes of the shareholders. Unless the shareholders themselves explicitly determine an altruistic purpose, this means ‘conduct[ing] the business in accordance with [shareholders’] desires, which generally will be to make as much money as possible while conforming to their basic rules of the society, both those embodied in law and those embodied in ethical custom’.

- If managers also had a social responsibility, they would find themselves in the position of having to act against the interests of shareholders, for example by hiring the ‘hardcore’ unemployed to combat poverty instead of hiring the most capable workers. By doing so, they would spend shareholders’ money to pursue a general interest. In other words, they would impose a tax on shareholders and also decide how to use its proceeds. Yet, it is countered, if there are serious and urgent economic and environmental problems, then it is necessary that managers face them without waiting for politicians’ action, which is always late and imperfect. According to Friedman, it is undemocratic for private individuals using other people’s money (and, importantly, exploiting the monopolistic rents of the large corporations they lead) to impose on the community their political preferences on how to solve urgent economic and environmental problems, which should instead be addressed through the democratic process.

- The market is based on the unanimity rule; in ‘an ideal free market’, there is no exchange without the consent of those who participate in it. Politics, on the other hand, operate according to the conformity principle, whereby a majority binds the dissenting minority. The intervention of politics is necessary because the market is imperfect. But the social responsibility doctrine would extend the mechanisms of politics to the market sphere, since a private subject (enjoying some monopoly power) would impose its political will on others.

- Often, the idea of corporate social responsibility (CSR) is just a public relations exercise to justify managerial choices already consistent with the interests of shareholders. Looking after the well-being of employees, devoting resources to the firm’s local communities, and so on may well be (and, as a rule, will be) in the long-term interest of corporations. Indeed, cloaking these actions under the label of CSR, as it was fashionable to do in 1970 (and is again today), can in itself contribute to increasing profits.

Missing from Friedman’s Picture: The Shareholders

Friedman’s essay assigned a totally passive role to what he calls the corporation’s ‘owners’ or ‘the employers’—that is, the shareholders. They are merely the beneficiaries of directors’ duty to increase profits, but they have no role to play in pursuing that very goal other than (as he notes in passing) when they elect the board.

That’s understandable. When Friedman wrote his piece, the shareholders of US companies were mostly individuals and rarely voted at annual meetings other than to rubber-stamp managers’ proposals. Today, a large majority of listed firms’ shares are held by institutional investors—that is, managers of other people’s funds. Institutions have become key players at US (as well as non-US) listed corporations (eg, this OECD study with data from across the world), because they regularly vote portfolio shares at shareholder meetings. And their pro-management vote is nowadays anything but certain.

This creates one additional layer of employee/employer relationships, to use Friedman’s terminology (today, we would say principal/agent relationships): the one between the institutions holding shares or (as Friedman saw it) their own managers, and the individuals (usually workers and pensioners) whose funds the managers invest. (To be sure, it is often more complicated than that because some institutions, such as pension funds, often delegate their asset management to other institutions; but this is not relevant for the purposes of my analysis).

Friedman’s essay raises the question: is there any room for asset managers to assume social responsibility duties in deciding how to invest and how to vote? In Friedman’s logic, the answer should be ‘no’, and it’s easy to imagine that he would chastise those fund managers who portray themselves (not always veritably) as socially responsible investors. Like corporate managers, fund managers manage other people’s money and should not grant themselves the license to make political choices, which will inevitably please some of their beneficiaries and not others. Their only goal should be giving their clients the highest returns on the funds invested.

Of course, much like a corporation can be set up with an altruistic (or mixed) purpose, so can asset management products expressly be marketed as socially responsible or ethically-investing. Intuitively, investors in such funds expect them to invest and vote in accordance with the socially responsible commitments undertaken. But absent a CSR connotation—namely, if the mutual fund has been marketed as a tool for generating financial returns—fund managers have to assume that the fund’s investors have a financial objective in mind and do not expect their own political preferences to be promoted by their fund manager, especially if that comes to the detriment of their return. Whether implicitly or explicitly, that’s the bargain with each of the fund shares buyers.

However, things are not always so straightforward. Passive institutional investors replicating indexes and, therefore, holding the entire market rather than picking stocks now hold more than 40 percent of the US stock market. As Madison Condon and Jack Coffee have noticed—here and here, respectively—for investors of that kind, portfolio value maximization may well mean pushing for ESG (Environment, Social and Governance) policies at the individual company level that, while not necessarily profitable for that company, will increase portfolio returns by making other companies more profitable. Think, for instance, of systemically important financial institutions adopting more conservative risk management policies that significantly reduce the chances of a potentially devastating financial crisis.

Hence, the overlap between socially responsible and profit-maximizing behavior, which Friedman himself acknowledged to be present at the individual company level and criticized only as being politically dangerous, is now even more pervasive at the institutional shareholder level.

In theory, all portfolio value maximizers’ decisions on ESG matters should be based on an assessment of the effects that the adoption of a given policy by an individual portfolio company would have, both on its value and on the value of the totality of other portfolio companies. Because ESG policies require widespread adoption to be effective, different scenarios will have to be elaborated and factored in to estimate those effects. Multiple other variables will have to be considered and a number of questionable assumptions made.

Passive investors, like any organization, are unlikely to have the human and financial resources to fully engage with this kind of assessment, let alone reach solid conclusions. And it would be naïve to assume that political preferences do not affect the simplified analysis they inevitably resort to in determining their ESG preferences.

Owing to shareholder pressure and/or managers’ desire to retain their jobs, the ESG preferences of portfolio value-maximizing institutions may well trickle down to the individual portfolio company level. Under what conditions that is the case will depend on a number of factors, including whether the company is protected from competition, undiversified shareholders’ stakes in the company, how politically divisive the socially responsible action is, and so on. Yet in some cases, and in respect of some of the socially and politically sensitive issues, managers will yield to those preferences. Given Friedman’s premise that ‘increasing profits’ must be the only corporate goal because the shareholders are the owners/employers, there is some irony to that.

Irony aside, today’s corporate world is very different from the one Milton Friedman wrote in. Yet, his essay still provides a useful framework for understanding the implications of managing companies for one purpose or another. And perhaps also for answering the reframed question of whether corporate managers should cater to the preferences of their portfolio-value-maximizing indexing investors when making decisions on behalf of their corporations.

À la prochaine

devoirs des administrateurs Gouvernance normes de droit Responsabilité sociale des entreprises Valeur actionnariale vs. sociétale

Corporations, Directors’ Duties and the Public/Private Divide

Ivan Tchotourian 25 septembre 2020 Ivan Tchotourian

La professeur australienne Jennifer Hill (toujours intéressante à lire, je vous la conseille vivement !) vient de publier ce nouvel article « Corporations, Directors’ Duties and the Public/Private Divide » dans l’ECGI Law Series 539/2020 (25 septembre 2020). Par rapport à nos thématiques du site, cette étude est un incontournable !

Extrait :

Business history and theory reflect a tension between public and private conceptions of the corporation. This tension and conceptual ambiguity lay close to the surface of The Modern Corporation and Private Property, in which Berle and Means portrayed the modern public corporation as straddling the public/private divide. It is also embodied in the famous Berle-Dodd debate, which provides the basis for contemporary clashes between “different visions of corporatism,” such as the conflict between shareholder primacy and stakeholder-centered versions of the corporation.

This chapter examines a number of recent developments suggesting that the pendulum, which swung so clearly in favour of a private conception of the corporation from the 1980s onwards, is in the process of changing direction.

The chapter provides two central insights. The first is that there is not one problem, but multiple problems in corporate law, and that different problems may come to the forefront at different times. Although financial performance is a legitimate concern in corporate law, it is also important to recognize, and address, the danger that corporate conduct may result in negative externalities and harm to society. The chapter argues that it is therefore, a mistake to view the two sides of the Berle-Dodd debate as binary and irreconcilable. The second insight is that corporate governance techniques (such as performance-based pay), which are designed to ameliorate one problem in corporate law, such as corporate performance, can at the same time exacerbate other problems involving the social impact of corporations.

As the chapter shows, a number of recent developments in corporate law have highlighted the negative externalities and social harm that corporate actions can cause. These developments suggest the emergence of a more cohesive vision of the corporation that encompasses both private and public aspects. The developments also potentially affect the role and duties of company directors, who are no longer seen merely as monitors of corporate performance, but also as monitors of corporate integrity and the risk of social harm.

À la prochaine…

Gouvernance Normes d'encadrement normes de droit normes de marché Responsabilité sociale des entreprises

RSE : où en est-on ?

Ivan Tchotourian 24 septembre 2020 Ivan Tchotourian

Mme Hoyé propose une tribune intéressante sur la RSE dans son article « Responsabilité sociale des entreprises: où en sommes-nous ? » publié sur Ligere.fr le 17 septembre 2020. Elle fait le point et soulève le chemin encore à parcourir…

Extrait :

Au cours de ces dix dernières année, une évolution a été observée dans le sens de la nécessité croissante de « redéfinir le droit des sociétés » pour mieux prendre en compte l’évolution de l’analyse du droit et de l’économie. L’objectif sociétaire traditionnel porté par la « doctrine juridique de la personnalité d’entreprise », tient à la protection des intérêts des membres et des créanciers de la société. Les profits générés sont ensuite partagés entre les actionnaires considérés comme propriétaires de l’entreprise. Ainsi, l’approche de la théorie contractuelle prévaut et la promesse tacite des dirigeants de maximiser la richesse des actionnaires s’opère. En effet, selon la théorie de la Corporate Governance, il existe une nette distinction entre le rôle des propriétaires d’une société (les actionnaires) et des dirigeants (le conseil d’administration) lorsqu’il s’agit de prendre des décisions stratégiques efficaces. L’actuelle « coutume de la retenue » en matière d’éthique, complète l’accent mis sur une analyse économique de la fonction d’entreprise où les concepts d’efficience et de rentabilité semblent persister. Caractérisés par ses propres règles de position, les bénéfices sont considérés comme la « ligne de fond » de l’entreprise, et par conséquent, selon l’argument, il n’y a aucune possibilité d’évaluer moralement les activités menées dans ce cadre d’activité.

Pourtant, face aux nouveaux enjeux auxquels se confrontent les sociétés au XXIème siècle, la thèse de « l’entreprise- profit » soutenue par Friedman ne semble plus être à l’ordre du jour. Dès lors, les entreprises peuvent-elles entreprendre une activité économique dite « durable », où la recherche exclusive de bénéfices s’estompe au profit d’une meilleure éthique entrepreneuriale? L’éthique s’érige désormais comme élément incontournable de l’ensemble des concepts que nous pourrions utiliser pour tenir compte de la fonction organisationnelle que détiennent les entreprises. Non pas que les actions des sociétés peuvent avoir des effets puissants, à la fois bénéfiques et/ou préjudiciables, mais parce qu’une prise en compte éthique des actions des sociétés est presque impérative pour atteindre une croissance durable. Il s’agit d’optimiser les performances en évoluant vers une responsabilité sociale et environnementale (RSE) où les sociétés sont responsables de l’impact de leurs actions sur la société civile. L’entreprise doit alors intégrer à sa stratégie l’ensemble de sa chaîne de valeur, dont les parties prenantes (« stakeholders »), de manière à minimiser et à compenser les effets négatifs de son activité. L’objectif étant d’atteindre une qualité de vie au moins aussi bonne que celle dont nous bénéficions aujourd’hui, comme le soutien le « rapport Brutland » (1987). Pour cela, il est primordial que les structures de gouvernance d’entreprise agissent tant en termes de bien-être des employés, qu’en termes d’efficacité et de productivité. Cela implique l’utilisation de critères éthiques, sociaux et environnementaux (les 3 piliers de la théorie de « corporate governance ») dans la sélection et la gestion des portefeuilles de placements. De ce point de vue, l’idée d’équilibrer les responsabilités de l’entreprise se développe, acceptant le fait que les entreprises peuvent créer de la valeur en gérant mieux le capital naturel, humain et social.

(…) Dans le cadre transnational, divers outils d’orientation souvent à caractère facultatif visent à promouvoir le développement durable et le civisme social. En tant que préoccupation mondiale, une croissance durable ne peut être atteinte que si tous les pays agissent de concert mettant en oeuvre des actions coordonnées. C’était notamment l’objectif de l’accord de Paris en « faisant en sorte que les flux financiers soient cohérents avec une voie vers une réduction des émissions de gaz à effet de serre et un développement résilient au climat ». Le pacte Mondial lancé officiellement en 2000 invite les entreprises à adhérer, appliquer et promouvoir 10 principes en matière de droits fondamentaux. Cette adhésion a été assortie à l’obligation pour les entreprises de publier chaque année une communication sur les progrès réalisés dans l’application des principes. L’entreprise qui ne réalise pas cette obligation est considérée comme « non communicante » et peut être à terme radiée. Aussi, les Nations Unies ont présenté un projet de normes sur les responsabilités des sociétés transnationales et autres entreprises commerciales en matière de droits de l’homme. Les principes de Rugie font peser sur les entreprises des contrôles et vérifications périodiques par des organes nationaux ou multinationaux, permettant ainsi de prescrire un grand nombre d’actions concrètes à mener par les entreprises pour respecter les droits de l’homme . Ces travaux ont abouti à l’adoption d’une résolution du Conseil des Droits de l’Homme de l’ONU s’articulant autour de trois axes: « protéger, respecter et remédier » contribuant à faire progresser le débat juridique sur le rôle des Etats et des entreprises dans le domaine des droits de l’homme.

Pour autant, malgré la construction d’une voie de responsabilité internationale des entreprises, de nombreuses divergences peuvent encore être mises en évidence. C’est surtout l’absence de réglementation uniforme qui a attiré l’attention de la Commission européenne poussée à établir une certaine crédibilité et une harmonisation des pratiques avec une transparence des critères afin de combler le vide existant. Ainsi, dans sa stratégie RSE du 25 octobre 2011, la Commission fournit un cadre normatif de protection, via des sections comprenant la Direction Générale des Entreprises et la Société de l’Information qui guident le comportement des entreprises afin d’étendre l’influence de la RSE pour les responsabiliser vis-à-vis des effets qu’elles exercent sur la société. Par ailleurs, le levier du droit fiscal a été adopté par l’Union européenne dans un contexte juridique de financement durable, mettant en place une taxation corrective qui promeut les projets les plus respectueux et taxe ceux qui sont dommageables dans le but d’orienter les comportements vers une situation économique jugée optimale. Ces initiatives ont été prises par les institutions européennes afin d’encourager les entreprises à « aller au-delà de la conformité », soulignant qu’il existe une relation entre les actions proactives et l’amélioration de la compétitivité. Au moins, la politique de l’UE indique clairement que les actions volontaires des entreprises ne doivent pas être considérées comme un substitut à la réglementation légale. C’est pourquoi l’UE doit continuer à soutenir de manière proactive les activités qui peuvent faciliter le progrès de la conduite responsable des entreprises en encourageant les acteurs des secteurs clés à s’appuyer sur des projets responsables et à définir des exigences de diligence raisonnable.

(…)

Ainsi, il apparaît essentiel de définir un équilibre stable entre les impératifs moraux et économiques. Les entreprises, comme l’ensemble des agents ont des devoirs moraux, des responsabilités sociales et devraient être de « bonnes entreprises citoyennes ». C’est ce que met en exergue le nouveau « duty of care » ( devoir de diligence) désormais attendu des sociétés, qui encourage une voie de réorientation de la logique du système productif vers de nouveaux objectifs plus responsables. Ce devoir conduirait à l’acceptation d’une rentabilité financière moindre à court terme, en renonçant aux bénéfices immédiats, afin d’encourager un développement éthique, social et durable sur une activité économique à plus long terme. Un tel principe doit être appuyé par toutes les parties prenantes afin que le mouvement soit étendu à l’ensemble des agents économiques. Néanmoins, il est encore tôt pour prédire les effets de ces changements, qui soulèvent la question des méthodes de régulation, leur introduction étant encore récente et sans changement réel, notamment du fait du peu de mesures actuelles permettant d’imposer des sanctions. Par ailleurs, il convient également de noter la spécificité des questions environnementales, qui ne sont pas seulement dépendantes de la gouvernance des entreprises mais font appel à d’autres acteurs (dépendance à la science, prospective, etc.) et suggèrent des investissements importants afin de se libérer des ressources naturelles et éviter une complète destruction de la valeur. Le problème ne dépend plus de l’ignorance, mais de la vitesse des changements ainsi que de la propagation des déséquilibres. Par conséquent, le droit des sociétés peut être une réponse, mais la réflexion interdisciplinaire semble hautement nécessaire pour parvenir à la possibilité d’un équilibre entre le développement durable et la primauté des actionnaires.

Gouvernance mission et composition du conseil d'administration place des salariés Responsabilité sociale des entreprises

Salariés dans les CA = moins bonne performance ?

Ivan Tchotourian 24 septembre 2020 Ivan Tchotourian

Dans The conversation, les chercheurs Nagati, Boukadhaba et Nekhili livrent un constat étonnant sur la présence des salariés dans les CA en France : oui, ils sont plus présents que par le passé, mais leur impact sur la performance de l’entreprise est critiquable… d’où la méfiance des actionnaires ! (« Salariés dans les conseils d’administration : une présence qui dérange les actionnaires… », 17 septembre 2020).

Extrait :

Une gouvernance de plus en plus partenariale

Pour ce qui est des critères de gouvernance, la régulation du mode de fonctionnement du conseil d’administration n’a ainsi cessé d’évoluer ces dernières années. Celle-ci contraint davantage les entreprises à une plus grande diversité des membres du conseil d’administration, qui intègrent notamment de plus en plus de salariés.

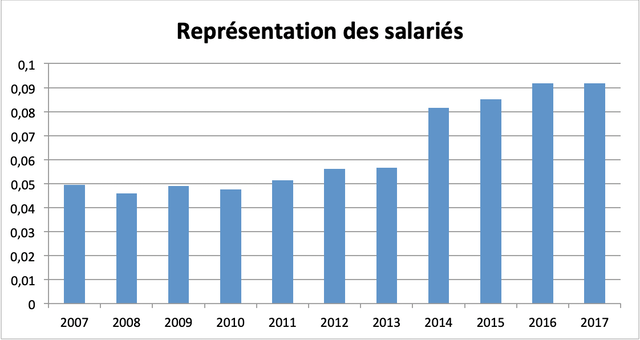

Le taux moyen de représentation des salariés dans le conseil d’administration des sociétés non financières du SBF 120 a ainsi évolué de 4,95 % en 2007 à 9,17 % en 2017 (voir graphique ci-dessous).

Une augmentation significative est notamment constatée à partir de 2014. Celle-ci s’explique par la loi n° 2013-504 de 14 juin 2013 relative à la sécurisation de l’emploi rendant obligatoire la présence d’au moins deux représentants de salariés pour les entreprises ayant des conseils d’administration de plus de 12 administrateurs et d’au moins un représentant pour les autres.

Cela témoigne de la volonté de s’orienter vers une gouvernance partenariale (stakeholders) qui s’oppose, dans ses grands principes, à la gouvernance actionnariale (shareholders).

Or, la présence de salariés au sein des conseils d’administration est généralement vue d’un mauvais œil par les actionnaires. C’est ce qui ressort de notre article de recherche publié en 2019 dans la revue International Journal of Human Resource Management sous le titre ESG Performance and Market Value : the Moderating Role of Employee Board Representation.

Cette étude porte sur un échantillon de grandes entreprises françaises non financières de l’indice SBF 120 durant la période 2007-2017.

À travers l’appréciation de la performance boursière des entreprises, les résultats de nos estimations montrent que, si le marché financier réagit positivement à la performance extrafinancière, il reste néanmoins réticent à la représentation des salariés dans le conseil d’administration.

En effet, la valeur moyenne de la performance boursière, mesurée par le Q de Tobin (rapport entre la somme de la capitalisation boursière et de la valeur de la dette, d’une part, et le total de l’actif du bilan, d’autre part), est de 1,142 chez les entreprises d’au moins un administrateur représentant des salariés contre 1,271 chez les entreprises n’ayant pas d’administrateurs représentants de salariés.

Conflits d’intérêts

De toute évidence, les actionnaires sont sensibles à la réalisation d’une bonne performance extrafinancière dont ils supportent à eux seuls les coûts s’y rapportant. Cependant, les actionnaires peuvent aussi voir dans la réalisation d’une bonne performance extrafinancière une stratégie pour les dirigeants de s’enraciner en jouant la carte des autres stakeholders, principalement les salariés, dont les intérêts ne coïncident pas nécessairement avec leurs propres intérêts.

Pour les actionnaires, donner des droits de vote aux salariés au sein du conseil d’administration peut donc contrebalancer leur pouvoir, mettant fin à leur suprématie, si relative soit-elle, dans le processus décisionnel.

Partant de l’idée qu’il existe une relation, souvent entretenue par des intérêts communs, entre les dirigeants et les employés, les recherches antérieures mettent en avant le postulat que les dirigeants peuvent procéder à l’augmentation des investissements sociétaux dans un objectif moins louable qui est celui de gagner le soutien et la confiance des salariés pour se soustraire du pouvoir, parfois excessif, des actionnaires.

De surcroît, la réalisation d’un niveau élevé de performance extrafinancière doublée par la nomination des administrateurs salariés dans le conseil d’administration ne peut que renforcer le sentiment de prudence des actionnaires envers les choix stratégiques des dirigeants en matière de développement sociétal.

Les mêmes résultats sont aussi trouvés lorsqu’on considère individuellement les différents piliers de la performance extrafinancière (environnemental, social, et de gouvernance). Nos conclusions confortent l’idée de la présence de conflits d’intérêts majeurs entre les actionnaires et les salariés autour des questions relatives au développement sociétal.

En somme, nos résultats interrogent la façon dont la participation des salariés à la prise de décision est conçue et présentée aux investisseurs financiers. Ces enseignements devraient inciter les entreprises à renforcer leurs efforts de formation et de communication pour plaider en faveur de l’adoption d’un conseil d’administration ouvert aux différentes parties prenantes.

Gouvernance Normes d'encadrement Responsabilité sociale des entreprises Structures juridiques

Purpose et revitalisation du droit des sociétés

Ivan Tchotourian 24 septembre 2020 Ivan Tchotourian

La professeure australienne Rosemary Teele Langford offre un bel article relayé par l’Oxford Business Law Blog : « Purpose-Based Governance and Revitalisation of Company Law to Facilitate Purpose-Based Companies » (18 septembre 2020).

Extrait :

The permissibility of corporations pursuing purposes other than profit has been the subject of debate for a number of years. This debate has intensified recently with proposals from bodies such as the British Academy and the Business Round Table (as discussed in previous OBLB posts) to allow or mandate the adoption of purposes by corporations. The challenges posed by COVID-19 have also focused attention on corporate purpose. In addition, there is increasing demand for appropriate vehicles for the conduct of social enterprises and other purpose-based ventures. At the same time, purpose is central to governance in the charitable sphere. In two recent articles I critically analyse the role of purpose in Australian company and charity law and demonstrate revitalisation of the law to facilitate adoption of, and governance centred on, purpose.

(…)

The second article, ‘Use of the Corporate Form for Public Benefit – Revitalisation of Australian Corporations Law’, provides extended detail on relevant aspects of the company law regime and focuses more closely on particular issues that arise in the facilitation of purpose-based companies. These include the application of directors’ duties in the context of such companies, with particular focus on the application of the duty to act in good faith in the interests of the company where companies have multiple purposes. This in turn has relevance for the drafting of appropriate constitutional provisions. Other issues arise in relation to standing and enforcement, departure from purposes and signalling. The focus of analysis is on the for-profit corporate form given that it is uncontroversial that other corporate forms (such as companies limited by guarantee) can be used for charitable and not-for-profit purposes.

In this respect, experience from the UK and US can provide helpful insights in the revitalisation of Australian law. In particular, scholarly analysis of the issues arising from these overseas legislative regimes, and suggested solutions, are invaluable in determining the application of directors’ duties to purpose-based companies and in framing appropriate constitutional provisions. Although changes to the law are not necessary to enable companies to adopt purposes, these lessons from other jurisdictions that have legislated to allow for special-purpose companies are therefore instructive in revitalising Australian law.

This analysis demonstrates that revitalisation of Australian law to allow purpose-based companies is feasible. In fact, it is opportune. This in turn allows company law to be attuned to practical and conceptual developments in the corporate sphere and more broadly. Such revitalisation does not require a fundamental shift, particularly given the malleability of directors’ duties. Indeed, given that the origins of the corporate form were connected with public ends, this evolution of the corporate form, and the attendant adaption of directors’ duties, are a natural adaptation rather than a radical reformulation.

À la prochaine…

Gouvernance Nouvelles diverses parties prenantes Responsabilité sociale des entreprises

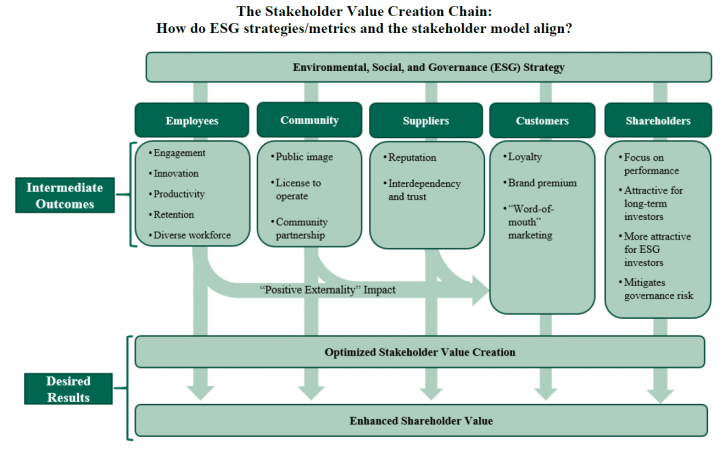

The Stakeholder Model and ESG

Ivan Tchotourian 17 septembre 2020 Ivan Tchotourian

Intéressant article sur l’Harvard Law School Forum on Corporate Governance consacré au modèle partie prenante et à ses liens avec les critères ESG : « The Stakeholder Model and ESG » (Ira Kay, Chris Brindisi et Blaine Martin, 14 septembre 2020).

Extrait :

Is your company ready to set or disclose ESG incentive goals?

ESG incentive metrics are like any other incentive metric: they should support and reinforce strategy rather than lead it. Companies considering ESG incentive metrics should align planning with the company’s social responsibility and environmental strategies, reporting, and goals. Another essential factor in determining readiness is the measurability/quantification of the specific ESG issue.

Companies will generally fall along a spectrum of readiness to consider adopting and disclosing ESG incentive metrics and goals:

- Companies Ready to Set Quantitative ESG Goals: Companies with robust environmental, sustainability, and/or social responsibility strategies including quantifiable metrics and goals (e.g., carbon reduction goals, net zero carbon emissions commitments, Diversity and Inclusion metrics, employee and environmental safety metrics, customer satisfaction, etc.).

- Companies Ready to Set Qualitative Goals: Companies with evolving formalized tracking and reporting but for which ESG matters have been identified as important factors to customers, employees, or other These companies likely already have plans or goals around ESG factors (e.g., LEED [Leadership in Energy and Environmental Design]-certified office space, Diversity and Inclusion initiatives, renewable power and emissions goals, etc.).

- Companies Developing an ESG Strategy: Some companies are at an early stage of developing overall ESG/stakeholder strategies. These companies may be best served to focus on developing a strategy for environmental and social impact before considering linking incentive pay to these priorities.

We note it is critically important that these ESG/stakeholder metrics and goals be chosen and set with rigor in the same manner as financial metrics to ensure that the attainment of the ESG goals will enhance stakeholder value and not serve simply as “window dressing” or “greenwashing.” [9] Implementing ESG metrics is a company-specific design process. For example, some companies may choose to implement qualitative ESG incentive goals even if they have rigorous ESG factor data and reporting.

Will ESG metrics and goals contribute to the company’s value-creation?

The business case for using ESG incentive metrics is to provide line-of-sight for the management team to drive the implementation of initiatives that create significant differentiated value for the company or align with current or emerging stakeholder expectations. Companies must first assess which metrics or initiatives will most benefit the company’s business and for which stakeholders. They must also develop challenging goals for these metrics to increase the likelihood of overall value creation. For example:

- Employees: Are employees and the competitive talent market driving the need for differentiated environmental or social initiatives? Will initiatives related to overall company sustainability (building sustainability, renewable energy use, net zero carbon emissions) contribute to the company being a “best in class” employer? Diversity and inclusion and pay equity initiatives have company and social benefits, such as ensuring fair and equitable opportunities to participate and thrive in the corporate system.

- Customers: Are customer preferences driving the need to differentiate on sustainable supply chains, social justice initiatives, and/or the product/company’s environmental footprint?

- Long-Term Sustainability: Are long-term macro environmental factors (carbon emissions, carbon intensity of product, etc.) critical to the Company’s ability to operate in the long term?

- Brand Image: Does a company want to be viewed by all constituencies, including those with no direct economic linkage, as a positive social and economic contributor to society?

There is no one-size-fits-all approach to ESG metrics, and companies fall across a spectrum of needs and drivers that affect the type of ESG factors that are relevant to short- and long-term business value depending on scale, industry, and stakeholder drivers. Most companies have addressed, or will need to address, how to implement ESG/stakeholder considerations in their operating strategy.

Conceptual Design Parameters for Structuring Incentive Goals

For those companies moving to implement stakeholder/ESG incentive goals for the first time, the design parameters range widely, which is not different than the design process for implementing any incentive metric. For these companies, considering the following questions can help move the prospect of an ESG incentive metric from an idea to a tangible goal with the potential to create value for the company:

- Quantitative goals versus qualitative milestones. The availability and quality of data from sustainability or social responsibility reports will generally determine whether a company can set a defined quantitative goal. For other companies, lack of available ESG data/goals or the company’s specific pay philosophy may mean ESG initiatives are best measured by setting annual milestones tailored to selected goals.

- Selecting metrics aligned with value creation. Unlike financial metrics, for which robust statistical analyses can help guide the metric selection process (e.g., financial correlation analysis), the link between ESG metrics and company value creation is more nuanced and significantly impacted by industry, operating model, customer and employee perceptions and preferences, etc. Given this, companies should generally apply a principles-based approach to assess the most appropriate metrics for the company as a whole (e.g., assessing significance to the organization, measurability, achievability, etc.) Appendix 1 provides a list of common ESG metrics with illustrative mapping to typical stakeholder impact.

- Determining employee participation. Generally, stakeholder/ESG-focused metrics would be implemented for officer/executive level roles, as this is the employee group that sets company-wide policy impacting the achievement of quantitative ESG goals or qualitative milestones. Alternatively, some companies may choose to implement firm-wide ESG incentive metrics to reinforce the positive employee engagement benefits of the company’s ESG strategy or to drive a whole-team approach to achieving goals.

- Determining the range of metric weightings for stakeholder/ESG goals. Historically, US companies with existing environmental, employee safety, and customer service goals as well as other stakeholder metrics have been concentrated in the extractive, industrial, and utility industries; metric weightings on these goals have ranged from 5% to 20% of annual incentive scorecards. We expect that this weighting range would continue to apply, with the remaining 80%+ of annual incentive weighting focused on financial metrics. Further, we expect that proxy advisors and shareholders may react adversely to non-financial metrics weighted more than 10% to 20% of annual incentive scorecards.

- Considering whether to implement stakeholder/ESG goals in annual versus long-term incentive plans. As noted above, most ESG incentive goals to date have been implemented as weighted metrics in balanced scorecard annual incentive plans for several reasons. However, we have observed increased discussion of whether some goals (particularly greenhouse gas emission goals) may be better suited to long-term incentives. [10] There is no right answer to this question—some milestone and quantitative goals are best set on an annual basis given emerging industry, technology, and company developments; other companies may have a robust long-term plan for which longer-term incentives are a better fit.

- Considering how to operationalize ESG metrics into long-term plans. For companies determining that sustainability or social responsibility goals fit best into the framework of a long-term incentive, those companies will need to consider which vehicles are best to incentivize achievement of strategically important ESG goals. While companies may choose to dedicate a portion of a 3-year performance share unit plan to an ESG metric (e.g., weighting a plan 40% relative total shareholder return [TSR], 40% revenue growth, and 20% greenhouse gas reduction), there may be concerns for shareholders and/or participants in diluting the financial and shareholder-value focus of these incentives. As an alternative, companies could grant performance restricted stock units, vesting at the end of a period of time (e.g., 3 or 4 years) contingent upon achievement of a long-term, rigorous ESG performance milestone. This approach would not “dilute” the percentage of relative TSR and financial-based long-term incentives, which will remain important to shareholders and proxy advisors.

Conclusion

As priorities of stakeholders continue to evolve, and addressing these becomes a strategic imperative, companies may look to include some stakeholder metrics in their compensation programs to emphasize these priorities. As companies and Compensation Committees discuss stakeholder and ESG-focused incentive metrics, each organization must consider its unique industry environment, business model, and cultural context. We interpret the BRT’s updated statement of business purpose as a more nuanced perspective on how to create value for all stakeholders, inclusive of shareholders. While optimizing profits will remain the business purpose of corporations, the BRT’s statement provides support for prioritizing the needs of all stakeholders in driving long-term, sustainable success for the business. For some companies, implementing incentive metrics aligned with this broader context can be an important tool to drive these efforts in both the short and long term. That said, appropriate timing, design, and communication will be critical to ensure effective implementation.

À la prochaine…