Le Ministère du travail américain soumet à commentaire une proposition inquiétante pour l’investissement responsable. Cette proposition est détaillée dans l’Harvard Law School Forum on Corporate Governance : « DOL Proposes New Rules Regulating ESG Investments » (7 juillet 2020).

Extrait :

The Department of Labor (“DOL”) has proposed for public comment rules that would further burden the ability of fiduciaries of private-sector retirement plans to select investments based on ESG factors and would bar 401(k) plans from using a fund with any ESG mandate as the default investment alternative for non-electing participants.

The proposed rules would prohibit a retirement plan fiduciary from making any investment, or choosing an investment fund, based on the consideration of an environmental, societal or governmental factor unless that factor independently represents a material economic investment consideration under generally accepted investment theories or serves as a tiebreaker in what the DOL characterizes as the rare case of economically equivalent investments. In order to select an investment with an ESG component, the plan fiduciaries would be required to compare investments or strategies on “pecuniary” factors such as diversification, liquidity and rate of return. Specific documentation would be required for the tiebreaker justification and for the selection and monitoring of an investment alternative in a 401(k) plan that includes ESG in its mandate or fund name. Most significantly, the proposed rules would prohibit a 401(k) plan from providing a qualified default investment alternative (“QDIA”) with an ESG component, no matter how small, even if that investment alternative satisfies the pecuniary factor requirements.

La crise de la COVID-19 met en relief l’importance de l’investissement responsable. Deux consultantes expertes dans le domaine invitent les comités de retraite à préparer les bonnes questions à poser à leurs gestionnaires de portefeuille.

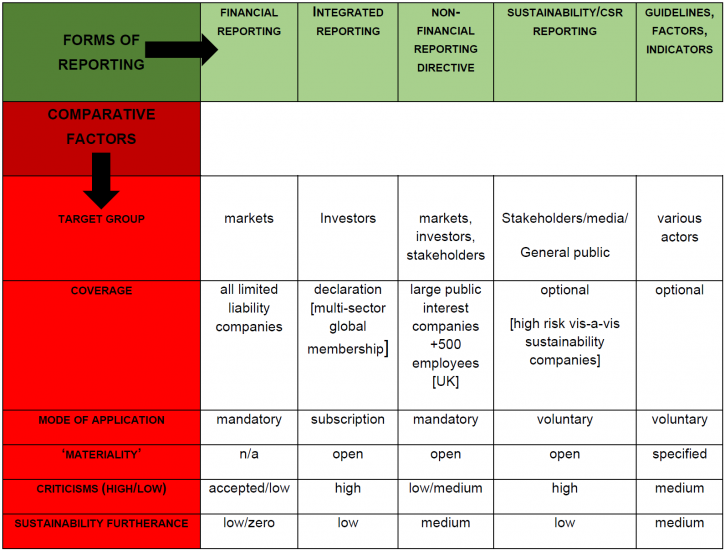

Random and arbitrary compliance with various initiatives makes companies’ sustainable practices ‘less’ rather than ‘more’ transparent. Our paper offers a comprehensive view on different reporting frameworks. It shows that there is a need to provide some clarity in this complex landscape. Fundamentally, the current reporting landscape is unlikely to impact positively on efforts towards sustainability. We suggest in our paper hat the scope of the NFRD, as the most promising of the existing initiatives, should be revisited so as to enhance its contribution to furthering corporations’ sustainable practices. Our paper supports reform of the NFRD which has constituted a positive step in the right direction. What is required now is stronger guidance on what to report and how to report it. Steps are being taken in the right direction towards clarifying metrics around sustainability (World Economic Forum 2020). A standardized and streamlined framework is necessary in order to pin companies down to something more concrete, rather than giving them too much choice on which guidelines, frameworks or recommendations they may opt to follow. Stronger, clearer and more concrete definitions of key concepts are required, as well as clarification of the rights of stakeholders in this area of activity. Proposals for reform that have arisen, with a consultation exercise by the European Commission, (European Commission Consultation 2020) are therefore to be welcomed. We suggest an expansion of the NFRD’s scope and that it represent sustainability as a positive instead of reducing the focus only to negative risks. EU member states and companies should have opportunities for effective compliance with the reporting requirements, with the NFRD better defining the concepts it refers to.

In this short essay (…), I take issue with the relevance and effectiveness of ’corporate purpose’ as a form of private ordering (eg, as a bylaws provision), or in other sources of soft-law (self-regulation in corporate governance codes, declarations of business associations, etc). I challenge whether these are, in fact, effective tools to induce greater commitment toward stakeholders.

(…) My possible disagreement with Mayer and other similar approaches and initiatives—or, more precisely, with a possible reading of these approaches and initiatives—lays in the excessive trust and emphasis that has been reserved to formulas concerning the purpose of the corporation and their possible consequences. Mayer argues that the corporate contract should include a reference to stakeholders and general social interests beyond value for shareholders, suggesting that this simple trick would have a meaningful impact on business conduct.

(…) The reasons are obvious.

First, these formulas are so broad, vague and ephemeral that they cannot possibly represent a compass for corporate action; they cannot provide meaningful guidance for virtually any specific corporate decision that implies a (legitimate) tradeoff between the interests of different stakeholders. Also, as precedents show, these formulas can be used even less to invoke the violation of directors’ duties and their liability. This conclusion is inevitable because the very essence of the agency relationship, the crucial function of a director or executive, is exactly mediating and balancing the different and often conflicting interests that converge on the corporation in an uncertain and evolving scenario. The idea of constraining the necessary discretion of directors within the boundaries of a simple purpose declaration is no better than the idea of writing in the contract with a painter that her work must be a masterpiece. Such an attempted shortcut to real value is self-evidently flawed.

Second, multiplying the goals and interests that directors must or can pursue, if it can have any effect at all, by definition increases their flexibility and discretion and makes it easier to justify, ex ante and ex post, very different choices. Without being cynical, from this perspective it is not surprising that these formulas are often welcomed, if not sponsored, by business associations and interest groups linked to managers, executives and entrenched shareholders.

Third, self-regulation and private ordering are often a way to avoid or delay the adoption of more stringent statutory or regulatory provisions. The former might be more or less effective, but they might also create an illusion of responsibility. The risk of putting too much trust into the beneficial consequences of these formulas is a disregard for more biting mandatory provisions, which may be necessary to avoid externalities and other market failures.

Petit panorama provenant de la Harvard Law School Forum on Corporate Governance des sujets sensibles auxquelles le Conseil d’administration doit être conscient !

Set out below are some key areas for companies and boards to consider as they seek to better understand and optimize the link between value and values, and as they assess how the current challenges present both risks and opportunities for the corporation’s pursuit of its purpose.

L’article s’intéresse aux problématiques suivantes :

Inégalités sociales et économiques ;

Parties prenantes ;

Covid-19 ;

Intelligence artificielle et nouvelles technologies ;

In particular, securities regulators should make pay ratio disclosures mandatory to improve transparency of executive pay packages at public companies. Pay ratio disclosures reveal the difference in the total remuneration between a company’s top executives and its rank and file workers….