Reporting non-financier : s’inspirer du modèle européen

Discussion intéressante sur le reporting non-financier de G. Tsagas et C. Villiers « Why ‘Less is More’ in non-Financial Reporting Initiatives: Concrete Steps Towards Supporting Sustainability » (Oxford Business Law Blog, 10 juin 2020).

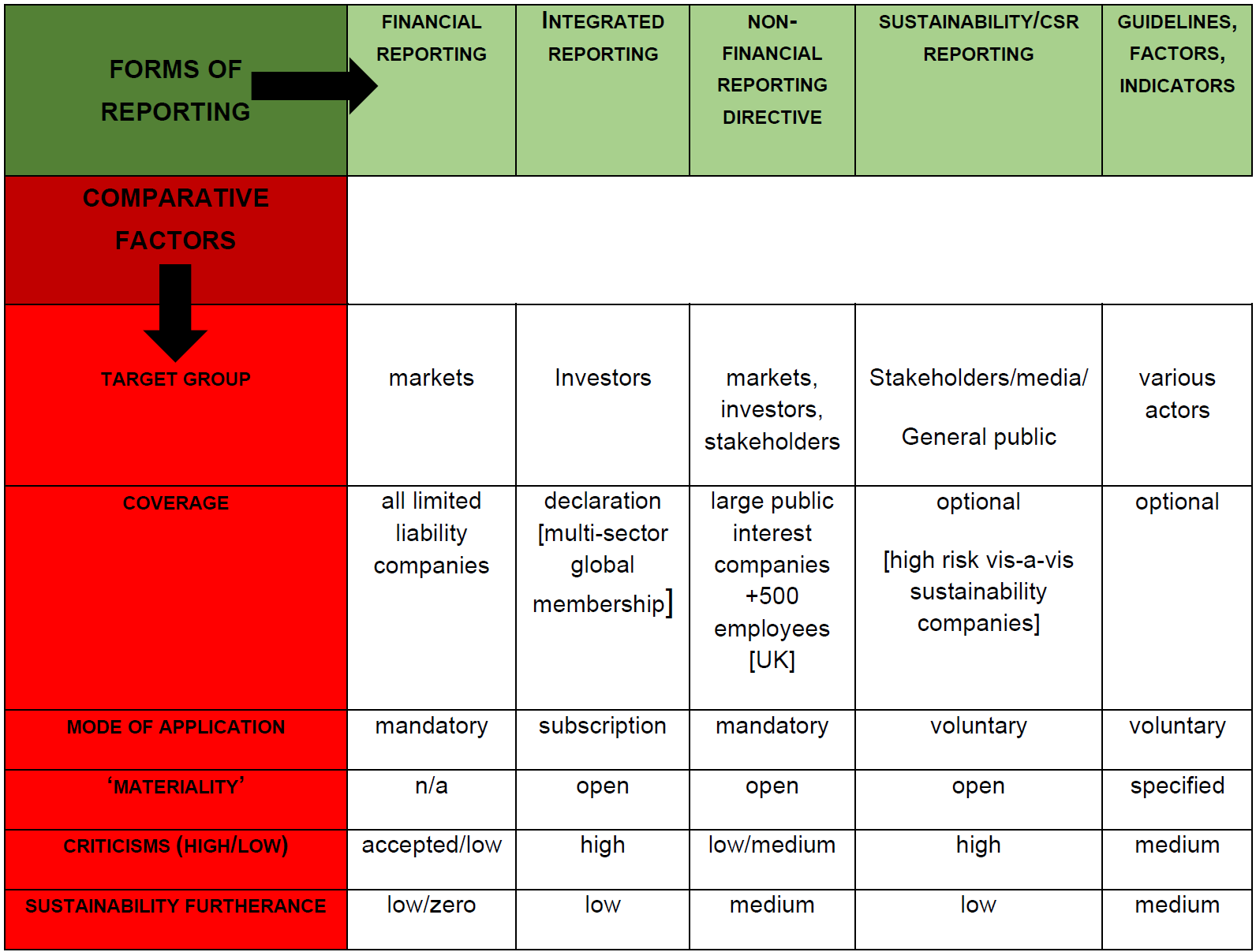

Random and arbitrary compliance with various initiatives makes companies’ sustainable practices ‘less’ rather than ‘more’ transparent. Our paper offers a comprehensive view on different reporting frameworks. It shows that there is a need to provide some clarity in this complex landscape. Fundamentally, the current reporting landscape is unlikely to impact positively on efforts towards sustainability. We suggest in our paper hat the scope of the NFRD, as the most promising of the existing initiatives, should be revisited so as to enhance its contribution to furthering corporations’ sustainable practices. Our paper supports reform of the NFRD which has constituted a positive step in the right direction. What is required now is stronger guidance on what to report and how to report it. Steps are being taken in the right direction towards clarifying metrics around sustainability (World Economic Forum 2020). A standardized and streamlined framework is necessary in order to pin companies down to something more concrete, rather than giving them too much choice on which guidelines, frameworks or recommendations they may opt to follow. Stronger, clearer and more concrete definitions of key concepts are required, as well as clarification of the rights of stakeholders in this area of activity. Proposals for reform that have arisen, with a consultation exercise by the European Commission, (European Commission Consultation 2020) are therefore to be welcomed. We suggest an expansion of the NFRD’s scope and that it represent sustainability as a positive instead of reducing the focus only to negative risks. EU member states and companies should have opportunities for effective compliance with the reporting requirements, with the NFRD better defining the concepts it refers to.

À la prochaine…

Ce contenu a été mis à jour le 30 mars 2022 à 5 h 35 min.

Commentaires