finance sociale et investissement responsable Gouvernance objectifs de l'entreprise Valeur actionnariale vs. sociétale

Beyond the bottom line: should business put purpose before profit?

Ivan Tchotourian 4 janvier 2019

Dans le Financial Times, Andrew Edgecliffe-Johnson propose un article ô combien enrichissant montrant que les choses commencent à changer en matière de gouvernance d’entreprise : « For 50 years, companies have been told to put shareholders first. Now even their largest investors are challenging that consensus ». L,article est intitulé « Beyond the bottom line: should business put purpose before profit? » (4 janvier 2019) et je vous le recommande chaudement.

In sum, the purpose-first movement is still far from ubiquitous and lacking in reliable data, but is the pursuit of something beyond profit worse than Friedman’s singular focus on shareholder returns? Encouraging companies to have a clear mission, consider their communities and steer their innovative impulses to good ends may not add up to systemic change, but it is surely better than the alternative.Critics such as Giridharadas would rather society concentrate on restoring politics as the forum through which we address its challenges. But for as long as politicians are viewed with more suspicion than chief executives and investors, the purposeful capitalists may be our best hope.Consumers, employees and campaigners are already learning how effective they can be in pushing companies to balance other stakeholders’ concerns with their returns to shareholders. Companies, in turn, have discovered that doing so can improve their reputations, persuade investors that they have a sustainable strategy and, ultimately, benefit their bottom line.When corporate America is paying chief executives 168 times as much as the median employee, steering the windfall from a historic tax cut to options-boosting buybacks and consolidating into ever larger groups, executives claiming to be solving society’s ills can expect pushback.The pursuit of purpose will not end the questions over how much chief executives should earn, what wages and taxes companies should pay or how much corporate power society will tolerate. Nor will investors stop judging chief executives by their share prices. But 50 years of putting shareholders first left corporations little trusted by non-shareholders and many are ready to try something different.As companies’ self-interest converges with the interests of other stakeholders, those who would improve the world have a chance to get some of the world’s most powerful instruments for change onside. They should grasp the opportunity business’s moral money moment has given them.

À la prochaine…

Ivan

autres publications Divulgation finance sociale et investissement responsable Gouvernance normes de droit responsabilisation à l'échelle internationale Structures juridiques

Publication sur Contact : « Où va l’entreprise ? »

Ivan Tchotourian 12 décembre 2018 Ivan Tchotourian

Bonjour à toutes et à tous, mon nouveau billet de blogue sur Contact est arrivé : « Où s’en va l’entreprise ? » me suis-je posé comme question… Inspiré d’une conférence donnée à l’Université Toulouse Capitole 1 à la mi-novembre, je synthétise dans ce billet plusieurs évolutions récentes déjà abouties ou en marche.

Morceaux choisis :

Si l’on part de cette idée qu’une entreprise plus juste est nécessaire, comment le droit est-il en train de la construire ? Mais commençons par le commencement et posons-nous la question suivante : le droit s’intéresse-t-il à cette entreprise nouvelle ? Incontestablement oui ! Alors que jusqu’à présent, le droit des affaires consacrait des réformes essentiellement techniques (apportant des précisions sur certains aspects de leur constitution, leur fonctionnement ou leur financement), les choses changent. Leur ADN et la perception fondamentale de leur fonction primaire sont placés sous le microscope du législateur qu’il soit nord-américain ou européen. Quelles sont les caractéristiques de cette nouvelle entreprise ? Selon moi, elle est organisée autour de 4 points :

- De nouveaux objectifs.

- De nouvelles structures.

- De nouvelles normes de gouvernance.

- De nouvelles façons de rendre compte.

Bien que ces innovations ne soient pas implantées au même rythme suivant les pays, elles sont néanmoins présentes dans les discours juridiques.

Au final, le Canada peut mieux faire. Trouver la formule d’une entreprise nouvelle est sans doute complexe et ses composants difficiles à identifier, il n’en demeure pas moins qu’il faut que les juristes de droit de l’entreprise se mobilisent. L’entreprise est peut-être une chose économique, mais elle n’est plus l’inconnue du droit qu’elle a longtemps été. Son impact sur l’économie, la finance, la politique, la démocratie, la fiscalité des pays est tel qu’il ne peut en aller autrement. Le futur est devant, reste à l’écrire…

Sinon, attention qu’une autre nouvelle entreprise ne s’impose pas : une entreprise court-termiste, dominée par une logique financière, axée sur la valeur boursière, soumise un activisme d’un genre nouveau et ignorant ses parties prenantes (voire même prédatrice de ces parties prenantes).

À la prochaine…

Ivan

finance sociale et investissement responsable Gouvernance Normes d'encadrement objectifs de l'entreprise Valeur actionnariale vs. sociétale

We must rethink the purpose of the corporation

Ivan Tchotourian 12 décembre 2018 Ivan Tchotourian

« We must rethink the purpose of the corporation » : c’est sous ce titre d’un article paru au Financial Times que Martin Wolf propose une analyse de l’entrepris rarement entendu en s’appuyant sur la publication de deux ouvrages. L’objectif de la société par actions devraient être repensé, tel est le message de l’auteur !

Morceaux choisis :

Yet, as Colin Mayer of Oxford university’s Saïd Business School argues in a remarkable and radical new book, Prosperity, all is not well with the corporation. The public at large increasingly views corporations as sociopathic and so as indifferent to everything, other than the share price, and corporate leaders as indifferent to everything, other than personal rewards. Judged by real wages and productivity, their recent economic performance has been mediocre.

The first is most important. Profit is not itself a business purpose. Profit is a condition for — and result of — achieving a purpose. The purpose might be making cars, delivering products, disseminating information, or many other things. If a business substitutes making money for purpose, it will fail at both.

Second, when legislators allowed incorporation of limited liability companies, they were not thinking of profits, but of the economic possibilities afforded by huge agglomerations of capital, effort and natural resources.

Crucially, contrary to economic wisdom, shareholders are not, in the actual world, the bearers of the residual risks in the business (other than relative to bondholders). The incompleteness of markets ensures that employees, suppliers and locations also bear substantial risk. Moreover, stock markets allow shareholders to diversify their risks across the world, something employees, for example, cannot hope to do with respect to their company-specific capital stock of knowledge and personal relationships. Moreover, everybody else is at risk from shareholders’ opportunistic behaviour. This has to weaken the commitment of everybody else.

These books suggest that capitalism is substantially broken. Reluctantly, I have come to a similar conclusion. This is not to argue for the abandonment of the market economy, but for better companies and more competition. The implication of Prof Mayer’s book is that the canonical Anglo-American model of corporate governance, with equality among shareholders, widely distributed share-ownership, shareholder value maximisation and the market in control is just one of many possible ways of structuring corporations. There is no reason to believe it is always the best. In some cases, it works. In others, such as highly-leveraged banking, it really does not. We should be explicitly encouraging a thousand different flowers of governance and control to bloom. Let us see what works.

À la prochaine…

Ivan

finance sociale et investissement responsable Gouvernance Nouvelles diverses

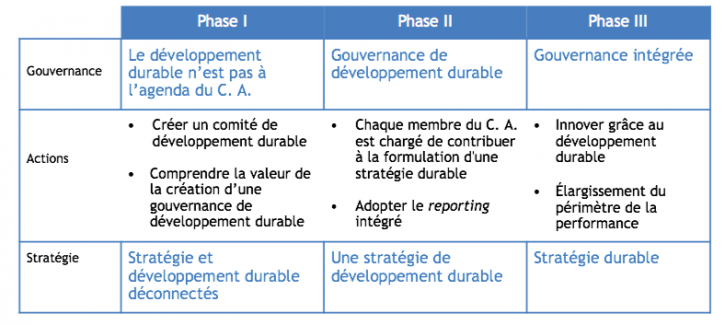

Modèle de « Gouvernance intégrée »

Ivan Tchotourian 11 décembre 2018 Ivan Tchotourian

En 2015, le Réseau entreprise et développement durable a publié un intéressant billet sur la manière d’intégrer systématiquement les enjeux ESG (Environnement, social et gouvernance) dans la stratégie de l’entreprise (ici).

Haykel Najlaoui de Neuvaction, discute ce mois-ci d’une nouvelle conception du rôle de la gouvernance, telle que proposée par différents organismes internationaux s’intéressant au reporting intégré. Au-delà de son ancrage théorique, il présente le modèle en trois phases qui permet d’opérationnaliser cette conception de la gouvernance et de propulser l’intégration du développement durable dans toutes les sphères de l’entreprise

L’auteur propose une démarche composée de trois phases permettant de passer d’une gouvernance qui ne tient pas compte du développement durable à une gouvernance intégrée.

À la prochaine…

Ivan

finance sociale et investissement responsable Gouvernance Normes d'encadrement

Too Many Corporations Act For The Short-Term. That Should Change

Ivan Tchotourian 6 septembre 2018 Ivan Tchotourian

Dans un article paru le 30 août 2018 dans Forbes, Arne Alsin livre une belle tribune en faveur du long-termisme des entreprises : « Too Many Corporations Act For The Short-Term. That Should Change ». Il revient par la même occasion sur le rachat d’actions par les entreprises, sur l’activisme actionnariale et sur le rôle que doivent jouer les investisseurs institutionnels.

Extrait :

As long-term investors, we want corporations to be thinking about the future. Unfortunately, from our vantage point, short-term thinking has become endemic on Wall Street. While CEOs publicly profess their commitment to the long-term interests of shareholders, too often we see how their actions directly contradict their words.

First, let’s consider a major factor of short-termism: stock buybacks. The immense buyback boom of 2018 is truly staggering. This year, S&P 500 companies are on pace to spend a record-breaking $1 trillion on stock buybacks, according to an analysis by Bloomberg. While executives often pitch these buybacks as a “return of capital” to shareholders, plenty of research suggests the truth is more complicated for long-term investors.

When executives choose to spend shareholder cash on buybacks, it’s a rather simple process: A company executive decides that “extra” cash on the balance sheet is better off being spent repurchasing shares. Without the input of shareholders—and often without any rigorous explanation to shareholders—CEOs then buy up stock, which drives up EPS, which, in turn, helps drive up the stock price. That’s the short-term view.

In the long-term, however, companies that spend billions on buybacks—like GE, Cisco, Oracle, and IBM to name a few—they effectively siphon money away from innovation, research and development, worker training, and reinvestment into new lines of business.

(…) In general, over the next few years, we anticipate seeing a wave of shareholder activism—through proposals and campaigns that align with the interests of long-term shareholders and target short-term mindsets. This isn’t just about buybacks, either. We expect long-term shareholders to fight for corporate issues surrounding fossil fuels, board diversity, worker pay, and so on.

Many of these fights have already begun, and that’s a positive development. Shirley Westcott, a senior vice President at Alliance Advisors LLC, recently noted that proposals are indeed on the rise. “Calls for various types of climate action have resonated strongly with investors as have social initiatives on gun violence, sexual misconduct and the opioid epidemic,” M. Westcott writes. “Pay programs have faced more frequent rebukes and even auditors, in isolated events, have been challenged over independence and performance.”

Corporate democracy may seem like an oxymoron in today’s top-down corporate structures, but the truth is that in a healthy economic system, corporate directors listen to and respond to feedback from all shareholders. Very often, we’ll see that conversation being dominated by short-term-minded activist hedge funds, whose managers buy up large positions in a stock, and then push management into short-term decisions that drive the stock up—but leave little left for reinvestment that create value over the long-term.

“Armed with their huge war chests,” writes Bill Lazonick, an economist at UMass, “these new-style corporate predators use a corrupt proxy-voting system, “wolf pack” hook-ups with other hedge funds, and once-illegal engagement with management to compel corporations to hand over profits that the hedge funds did nothing to create.”

True, but we believe activist hedge funds will have an increasingly major force to contend with: Major institutional shareholders, long-term investors, and, especially, pension funds.

À la prochaine…

engagement et activisme actionnarial finance sociale et investissement responsable Gouvernance

Des valeurs de RSE portées par les investisseurs

Ivan Tchotourian 30 août 2018

Bonjour à toutes et à tous, signalons que les investisseurs s’unissent de plus en plus pour défendre la responsabilité sociétale : « Onze investisseurs s’unissent pour changer les choses » (Le Devoir, 7 juin 2018).

Alors que s’apprête à débuter le Sommet du G7, 11 investisseurs institutionnels menés entre autres par la Caisse de dépôt et placement du Québec unissent leurs forces dans l’espoir de réaliser une série d’avancées dans les domaines des changements climatiques, de l’égalité entre les sexes ainsi que du déficit d’infrastructures. En collaboration avec le Régime de retraite des enseignantes et enseignants de l’Ontario, la Caisse souhaite que le groupe d’investisseurs — dont l’actif sous gestion dépasse 6000 milliards — mette à profit son approche à plus long terme, généralement plus adéquate pour relever des défis d’envergure. Leurs intentions ont été dévoilées à Toronto, mercredi, dans le cadre d’une conférence de presse à laquelle participaient entre autres le ministre fédéral des Finances, Bill Morneau, ainsi que son homologue à l’Environnement et au Changement climatique, Catherine McKenna.

finance sociale et investissement responsable Gouvernance mission et composition du conseil d'administration normes de droit Structures juridiques Valeur actionnariale vs. sociétale

Un projet de loi américain ambitieux : S.3348 – Accountable Capitalism Act

Ivan Tchotourian 17 août 2018 Ivan Tchotourian

Bonjour à toutes et à tous, la sénatrice Élisabeth Warren vient d’introduire un projet de loi très ambitieux (!) : le S.3348 – Accountable Capitalism Act.

Plusieurs points saillants ressortent de ce projet :

- La création d’un Office of United States Corporations.

- La possibilité de s’enregistrer auprès de cet organisme fédéral (alors que jusqu’à maintenant, rappelons-le, l’enregistrement se faisait auprès des États et notamment celui du Delaware).

- Les salariés représenteraient 40 % du CA.

- L’entreprise devrait poursuivre une mission sociétale.

- La redéfintion des devoirs des administrateurs et hauts-dirigeants.

Pour en savoir plus, lire cet article ici du The Guardian.

Extrait du projet de loi

SEC. 5. Responsibilities of United States corporations.

(a) Definitions.—In this section:

(1) GENERAL PUBLIC BENEFIT.—The term “general public benefit” means a material positive impact on society resulting from the business and operations of a United States corporation, when taken as a whole. (…)

(1) IN GENERAL.—The charter of a large entity that is filed with the Office shall state that the entity is a United States corporation.

(2) CORPORATE PURPOSES.—A United States corporation shall have the purpose of creating a general public benefit, which shall be—

(A) identified in the charter of the United States corporation; and

(B) in addition to the purpose of the United States corporation under the articles of incorporation in the State in which the United States corporation is incorporated, if applicable.

(c) Standard of conduct for directors and officers.—

(c) Standard of conduct for directors and officers.—

(1) CONSIDERATION OF INTERESTS.—In discharging the duties of their respective positions, and in considering the best interests of a United States corporation, the board of directors, committees of the board of directors, and individual directors of a United States corporation—

(A) shall manage or direct the business and affairs of the United States corporation in a manner that—

(i) seeks to create a general public benefit; and

(ii) balances the pecuniary interests of the shareholders of the United States corporation with the best interests of persons that are materially affected by the conduct of the United States corporation; and

(B) in carrying out subparagraph (A)—

(i) shall consider the effects of any action or inaction on—

(I) the shareholders of the United States corporation;

(II) the employees and workforce of—

(aa) the United States corporation;

(bb) the subsidiaries of the United States corporation; and

(cc) the suppliers of the United States corporation;

(III) the interests of customers and subsidiaries of the United States corporation as beneficiaries of the general public benefit purpose of the United States corporation;

(IV) community and societal factors, including those of each community in which offices or facilities of the United States corporation, subsidiaries of the United States corporation, or suppliers of the United States corporation are located;

(V) the local and global environment;

(VI) the short-term and long-term interests of the United States corporation, including—

(aa) benefits that may accrue to the United States corporation from the long-term plans of the United States corporation; and

(bb) the possibility that those interests may be best served by the continued independence of the United States corporation; and

(VII) the ability of the United States corporation to accomplish the general public benefit purpose of the United States corporation;

(ii) may consider—

(I) other pertinent factors; or

(II) the interests of any other group that are identified in the articles of incorporation in the State in which the United States corporation is incorporated, if applicable; and

(iii) shall not be required to give priority to a particular interest or factor described in clause (i) or (ii) over any other interest or factor.

(2) STANDARD OF CONDUCT FOR OFFICERS.—Each officer of a United States corporation shall balance and consider the interests and factors described in paragraph (1)(B)(i) in the manner described in paragraph (1)(B)(iii) if—

(A) the officer has discretion to act with respect to a matter; and

(B) it reasonably appears to the officer that the matter may have a material effect on the creation by the United States corporation of a general public benefit identified in the charter of the United States corporation.

(3) EXONERATION FROM PERSONAL LIABILITY.—Except as provided in the charter of a United States corporation, neither a director nor an officer of a United States corporation may be held personally liable for monetary damages for—

(A) any action or inaction in the course of performing the duties of a director under paragraph (1) or an officer under paragraph (2), as applicable, if the director or officer was not interested with respect to the action or inaction; or

(B) the failure of the United States corporation to pursue or create a general public benefit. (…)

(d) Right of action.—

(1) LIMITATION ON LIABILITY OF CORPORATION.—A United States corporation shall not be liable for monetary damages under this section for any failure of the United States corporation to pursue or create a general public benefit.

À la prochaine…

Ivan Tchotourian