Normes d’encadrement | Page 29

actualités canadiennes Gouvernance normes de droit

Vers une réforme du droit financier en Ontario ? Capital Markets Modernisation Taskforce (CMMT)

Ivan Tchotourian 31 juillet 2020 Ivan Tchotourian

Bonjour à toutes et à tous, voici une belle information pour celles et ceux intéressés par les problématiques de gouvernance et de droit des marchés. La province de l’Ontario a mis en place un groupe de travail pour envisager des réformes à l’encadrement réglementaire. 70 propositions ont été faites et la consultation sur celles-ci est ouverte jusqu’en septembre 2020 : « Capital Markets Modernisation Taskforce ».

Voici un résumé des principales pistes explorées… vraiment intéressant !

Extrait :

The CMMT was formed in February 2020 and reports directly to the Minister of Finance. It was tasked to develop “bold, innovative recommendations” to improve how capital markets function in Canada.

Twelve of the drafted proposals specifically target shareholder voting and company transparency, with the taskforce identifying an “imbalance” among Canada’s proxy and shareholder voting systems. Several stakeholders raised concerns to the CMMT about the influence of proxy advisors, errors in their reports and potential conflicts of interests where voting recommendations and consulting services were provided to the same businesses.

To remedy this, the CMMT proposes establishing a new regulatory framework that would provide companies with the right to ‘rebut’ reports from proxy advisors. In addition, the taskforce also hopes to restrict conflicts of interest by limiting the services proxy advisors can offer.

Several of the other proposals are aimed at reforming and improving the proxy plumbing. For instance, currently in Canada, the majority of shareholder votes are cast via proxies using either the company’s or dissident’s proxy ballot. Unfortunately, this means such proxy cards can look different and often confuse investors.

Therefore, the CMMT proposes the use of universal proxy ballots to improve standardisation and mandate voting disclosure for each side when a dispute arises.

At the same time, the taskforce has also proposed introducing rules to prevent over-voting and the requirement for companies listed on the Toronto Stock Exchange to have an annual shareholder votes on executive compensation. In further efforts to improve corporate governance standards, the taskforce proposes further legislative guidance be made around the role of independent directors in a bid to avoid conflicts of interest from arising, arguing that current laws do not fully address the role such directors play.

Elsewhere, the taskforce wants to reduce the ownership threshold for early warning reporting disclosure in Canadian companies from 10% to 5%. This would bring Canada in line with other major markets, with the CMMT also acknowledging that a shareholder can currently requisition a meeting with a holding of as little as 5%.

In a bid to improve transparency, the CMMT is also proposing the adoption of quarterly filing requirements for institutional investors of Canadian companies and – in a very encouraging step – the introduction of enhanced disclosure of material ESG information.

With stronger ESG reporting, Canada would be following in the footsteps of other jurisdictions and create a level playing field for its companies. In particular the taskforce identified the metrics used by the Sustainability Accounting Standards Board (SASB) and Taskforce on Climate-related Financial Disclosures (TCFD) as potential solutions.

Other CMMT’s recommendations include giving regulators new and enhanced powers when dealing with listed entities. For instance, the taskforce has proposed empowering the Ontario Securities Commission (OSC) to issue no-action letters. This already happens in the US where a company can seek a no-action letter from the Securities and Exchange Commission when it has the basis to exclude a particular shareholder proposal.

The CMMT has also proposed the introduction of broader remedies for the OSC when dealing with mergers and acquisitions. The taskforce proposes granting the OSC similar powers to those recently granted to the British Columbia Securities Commission, which can now rescind a transaction, require a person to dispose of securities in connection with a deal or even prohibit them from exercising voting rights.

À la prochaine…

engagement et activisme actionnarial Gouvernance Normes d'encadrement Responsabilité sociale des entreprises

Engagement actionnarial : photographie en 2020

Ivan Tchotourian 31 juillet 2020 Ivan Tchotourian

Novethic consacre une intéressante étude sur l’engagement actionnarial intitulée « Engagement actionnarial, les investisseurs responsables face aux dilemmes des AG 2020 », véritable cartographie des acteurs en présence et des enjeux de cette pratique.

Extrait :

L’étude détaille les différents rapports de force entre les acteurs en présence. Avec d’un côté, les investisseurs institutionnels, détenteurs de l’épargne ou des fonds de retraite, qui, pour les plus responsables, veulent s’assurer de la pérennité et de la croissance de leurs actifs sur le long terme. De l’autre, les sociétés de gestion, qui travaillent pour plusieurs investisseurs institutionnels et qui, dans leur stratégie d’engagement actionnarial, doivent faire la synthèse des souhaits de chacun de leurs clients. Enfin, se trouvent les entreprises cotées, pas toutes enclines à écouter les alertes et les revendications de leurs actionnaires de long terme.

Mais l’urgence climatique, de même que les risques grandissants liés aux inégalités sociales, poussent les acteurs financiers à l’action. La crise du Covid-19, avec son rôle d’amplificateur des risques environnementaux, sociaux et de gouvernance (ESG), s’est également invitée au programme des AG. Et malgré le huis clos des assemblées générales imposé par les mesures sanitaires, des victoires ont été remportées.

(…) La France semble avoir pris le virage, cette année, d’un engagement actionnarial plus actif, alors que les relations entre actionnaires et grandes entreprises cotées y étaient jusqu’alors plutôt feutrées. La réglementation pousse notamment les investisseurs institutionnels à plus de transparence sur leur pratique de l’engagement. Le mouvement mérite toutefois de prendre encore de l’ampleur. Selon l’étude de Novethic, près de la moitié des 100 plus grands investisseurs institutionnels français ne remplissent pas encore leur obligation, prévue dans la loi Pacte, de publier leur politique d’engagement actionnarial et un rapport sur son application.

Reste à transformer l’essai. De grandes sociétés de gestion demeurent encore sur la touche, en n’accordant pas toujours leurs votes lors des assemblées générales, à leurs propres déclarations sur le climat. Plusieurs études l’ont montré, comme celle d’InfluenceMap qui montre que des sociétés de gestion comme BlackRock ou Vanguard ne votent en général pas en faveur des résolutions externes sur le climat. De ce côté-là aussi, cela change : en début d’année, BlackRock a annoncé son adhésion à Climate Action 100+ et son intention d’avoir une politique de vote plus active. La saison des AG 2021 devrait donc s’avérer intéressante.

À la prochaine…

actualités internationales Gouvernance Normes d'encadrement objectifs de l'entreprise Responsabilité sociale des entreprises

En rappel : Stakeholder Principles in the COVID Era

Ivan Tchotourian 31 juillet 2020 Ivan Tchotourian

Alors que les entreprises se relancent péniblement, un rappel de ces mots du Forum économique mondial d’avril 2020 paraît adéquat (histoire de ne pas oublier et de ne pas faire primer l’économique et le financier sur toute autre considération).

Déclaration « Stakeholder Principles in the COVID Era »

As business leaders, we are experiencing how profoundly the COVID-19 emergency is affecting the world. Our employees face health risks in their daily lives, and challenges in performing their jobs. Our ecosystem of suppliers and customers is under extreme pressure. By doing all we can to coordinate our work, we can ensure that our society and economy get through this crisis and we can mitigate its negative impact on all of our stakeholders.

We accept our responsibility to address these crises. The first priority is to win the war against coronavirus. We need to do that while doing all we can to help our stakeholders now and, at the same time, to avoid a prolonged economic impact in the future. We will continue to embody “stakeholder capitalism” and do all we can to help those who are affected, and help secure our common prosperity.

To this end, we endorse the following Stakeholder Principles in the COVID Era:

− To employees, our principle is to keep you safe: We will continue do everything we can to protect your workplace, and to help you to adapt to the new working conditions

− To our ecosystem of suppliers and customers, our principle is to secure our shared business continuity: We will continue to work to keep supply chains open and integrate you into our business response

− To our end consumers, our principle is to maintain fair prices and commercial terms for essential supplies

− To governments and society, our principle is to offer our full support: We stand ready and will continue to complement public action with our resources, capabilities and know-how

− To our shareholders, our principle remains the long-term viability of the company and its potential to create sustained value

Finally, we also maintain the principle that we must continue our sustainability efforts unabated, to bring our world closer to achieving shared goals, including the Paris climate agreement and the United Nations Sustainable Development Agenda. We will continue to focus on those long-term goals.

The world has gone through other crises. As a global community, we will prevail this time as well. But, to do so, we must all bond together and coordinate our response. As business leaders, we pledge to stand at society’s service, to help preserve and rebuild a viable society and economy, and to do all we can for our stakeholders.

À la prochaine…

actualités internationales Gouvernance normes de droit Responsabilité sociale des entreprises Structures juridiques

Public Benefit Corporation : réforme en vue

Ivan Tchotourian 31 juillet 2020 Ivan Tchotourian

En cette période estivale, suivre l’actualité est toujours intéressant. Ma lecture d’un article ce matin « Renewed Interest in IPOs of Public Benefit Corporations » (de Cydney Posner) m’apprenait que l’État américain du Delaware est en train de débattre d’une réforme législative en matière d’entreprise à mission !

Pour accéder à cette réforme : ici

Extrait :

These and other similar risks are some of the reasons that, in adopting laws authorizing PBCs, the Delaware legislature made it particularly difficult to convert a traditional corporation to a PBC. For example, currently, the approval of 2/3 of the outstanding stock is required for a traditional corporation to amend its certificate of incorporation to become a PBC or to merge with another entity if the effect of the merger is to convert the shares into shares of a PBC. (Note that, originally, the vote required for conversion was 90%, which made it well nigh impossible for a traditional public company to convert to a PBC.) Appraisal rights are available to stockholders that did not vote in favor of the conversion or merger. And the same vote is required for conversion from a PBC form of entity into a traditional corporation.

The legislation that was just passed by the House in Delaware would, if ultimately signed into law, eliminate the 2/3 voting requirements, making it easier to convert a traditional corporation to a PBC or a PBC to a traditional corporation. Only the standard stockholder vote provisions would be applicable—generally a vote of a majority of the outstanding shares (or any greater or other vote required under the company’s certificate of incorporation) would be required. The amendments would also eliminate the special appraisal rights provisions, with the result that appraisal rights would not be available for conversions resulting from amendments to the certificate, but standard appraisal rights (§262) would be available in the context of mergers.

In addition, as noted above, the current PBC statute mandates that the board of directors manage the business and affairs of the PBC by balancing “the pecuniary interests of the stockholders, the best interests of those materially affected by the corporation’s conduct, and the specific public benefit or public benefits identified in its certificate of incorporation.” The statute provides that, with respect to a decision implicating the “balance requirement,” directors of PBCs will be deemed to satisfy their fiduciary duties to stockholders and the corporation if their decision “is both informed and disinterested and not such that no person of ordinary, sound judgment would approve.” A PBC is also permitted to include in its certificate, for purposes of its director exculpatory provisions under §102(b)(7) and its indemnification provisions under §145, that any disinterested failure to satisfy the mandate will not be considered to “constitute an act or omission not in good faith, or a breach of the duty of loyalty.”

The new legislation would also amp up the protections for directors of a PBC. The amendments would clarify that a director would not be considered “interested” in connection with a balancing decision solely because of the director’s interest in stock of the corporation, except to the extent that the same ownership would create a conflict of interest if the corporation were not a PBC. The amendments would also provide that, in the absence of a conflict, no failure to satisfy the balancing requirement would, for purposes of §102(b)(7) or §145, be considered “an act or omission not in good faith, or a breach of the duty of loyalty, unless the certificate of incorporation so provides.” That is, the certificate would no longer need to expressly provide for the protection for it to apply. In addition, the amendments would provide that, to bring any lawsuit to enforce the PBC balancing requirement, the plaintiffs must own at least 2% of the corporation’s outstanding shares or, for PBCs listed on a national securities exchange, shares with a market value of at least $2 million, if lower.

À la prochaine…

finance sociale et investissement responsable Gouvernance normes de droit normes de marché Publications publications de l'équipe Responsabilité sociale des entreprises

Une publication de l’équipe sur les entreprises à mission

Ivan Tchotourian 30 juillet 2020 Ivan Tchotourian / Margaux Morteo

Nouvelle publication sur l’entreprise à mission sociétale dans la revue Vie & sciences de l’entreprise 2019/2 (N° 208) sous le titre : « Entreprises à mission sociétale : regard de juristes sur une institutionnalisation de la RSE ».

Merci à Margaux d’avoir partagé la plume…

Résumé :

L’évolution actuelle du droit des affaires démontre une influence considérable de la Responsabilité Sociétale des Entreprises (RSE) dans la gouvernance des sociétés. Suite à de nombreux scandales d’envergure internationale, le choix de la RSE se dessine désormais comme un incontournable pour les entrepreneurs d’aujourd’hui et de demain. Le droit traduit cette nouvelle orientation du système économique au travers de l’évolution combinée du droit dur et du droit souple. L’émergence depuis plusieurs années d’entreprises à mission sociétale en constitue une illustration marquante. Toutefois, le risque d’aboutir à une RSE sans contenu est présent, comme l’illustre la thématique connue de « l’écoblanchiment ». Pour y faire face, le droit a passé la vitesse supérieure avec la récente réforme française portée par le projet de loi PACTE. Ces nouveaux mécanismes, souvent salués et parfois institutionnalisés, posent tout de même la question de l’efficacité pour la RSE d’irriguer la sphère économique, de savoir si le droit se construit de la bonne manière et, finalement, de déterminer si cette finance sociale est une réelle opportunité d’appropriation sociétale pour ces organisations qualifiées d’hybrides.

À la prochaine…

finance sociale et investissement responsable Normes d'encadrement normes de marché Responsabilité sociale des entreprises

Placement ESG : un rappel judicieux

Ivan Tchotourian 29 juillet 2020 Ivan Tchotourian

Intéressant article dans Le Temps consacré à la financiarisation de la RSE : « Les placements ESG allient recherche du profit et valeurs individuelles » (6 juillet 2020). Une belle synthèse !

Extrait :

En 2019, selon l’association sectorielle Swiss Sustainable Finance, quelque 1163 milliards de francs ont été investis de façon durable en Suisse, soit une hausse de 62% par rapport à l’année précédente. Cela démontre que les investisseurs actuels se soucient de savoir où va leur argent. Ils aspirent à générer des rendements solides avec leur patrimoine tout en assumant leur responsabilité sociale et en contribuant ainsi à rendre notre monde un peu meilleur.

L’une des options pour y parvenir réside dans les placements durables, associés fréquemment aux trois lettres E, S et G, soit ESG. A cet égard, les entreprises dans lesquelles il s’agit d’investir sont passées au peigne fin. Qu’en est-il du facteur E comme «environnement»? Comment abordent-elles concrètement les questions écologiques? Comment gèrent-elles le S, à savoir les aspects sociaux, à l’interne comme à l’extérieur? Et à quoi ressemble le G comme «gouvernance», soit la gestion de l’entreprise?

Par le biais de critères fondés scientifiquement, il est possible de mesurer et d’évaluer les performances correspondantes des entreprises. Les investisseurs peuvent ainsi savoir si leurs investissements sont en adéquation avec leurs valeurs personnelles et s’ils ont un impact positif, notamment en fonction des 17 Objectifs de développement durable de l’ONU (ODD). C’est précisément parce que les placements durables responsabilisent les entreprises qu’ils fournissent une importante contribution à l’atteinte desdits objectifs.

(…) Ce dernier a d’ailleurs encore gagné en importance en raison de la pandémie de Covid-19. Actuellement, les Etats encouragent assidûment la recherche d’un vaccin. Auprès des investisseurs, les placements durables connaissent précisément un essor sans précédent. Karsten Güttler, Senior Sustainable Investment Specialist chez UBS Asset Management: «Durant le premier trimestre de cette année, les fonds à orientation durable ont attiré un niveau record de capitaux sur les marchés mondiaux, même lorsque ceux-ci se trouvaient sous le joug de la pandémie. Les fonds durables mondiaux ont connu un afflux de quelque 50 milliards de dollars, tandis que, selon Morningstar, l’univers de fonds plus large a enregistré un assèchement de l’ordre de 400 milliards de dollars.»

Cette tendance est due à deux facteurs: «Les données du marché illustrent que les indices ESG tels que le MSCI SRI global et l’ACWI ont réalisé des rendements ajustés au risque supérieurs à ceux de leurs pendants traditionnels sur trois et cinq ans», explique Karsten Güttler. Il est également possible de mieux exploiter les opportunités à long terme, notamment en misant sur des placements durables ou des investissements liés aux 17 Objectifs de développement durable. «Si l’on saute dans le train à temps, on a des chances de réaliser des bénéfices. Davantage que dans les secteurs en stagnation à faible potentiel de croissance.» En associant croissance et durabilité, on crée une plus-value pour les investisseurs comme pour la société dans son ensemble.

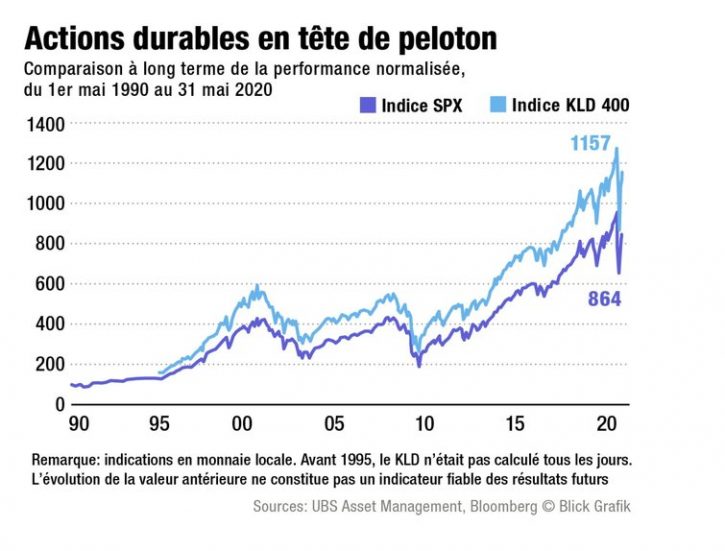

L’excellente rentabilité des placements durables est illustrée par la comparaison de l’indice S&P 500, qui regroupe les actions des 500 principales entreprises américaines cotées en bourse, et du KLD 400. Le KLD 400 reflète le développement des entreprises américaines présentant un meilleur profil ESG. Karsten Güttler: «Le KLD 400 l’emporte haut la main, comme en témoigne l’analyse de 1990 à nos jours. Et cela était déjà le cas bien avant que la thématique ne devienne monnaie courante.» Le KLD 400 englobe environ 250 actions du S&P 500, une centaine d’autres entreprises importantes non listées dans le S&P 500, ainsi qu’environ 50 sociétés qui se distinguent par un profil social soutenu.

Pour les investisseurs, il n’a donc jamais été plus judicieux de placer leur argent durablement et d’intégrer ce faisant les critères ESG dans le processus de décision. Attention toutefois: miser exclusivement sur des entreprises au bilan ESG favorable ne suffit pas. «Investissez également dans les changements positifs en matière de développement durable, conseille Karsten Güttler. Même si cela paraître illogique de prime abord, vous bénéficiez ainsi d’un outil performant attrayant financièrement et qui réalise une plus-value sociale maximale, étant donné qu’il intègre l’ensemble des sujets économiques.»

Autre facteur important: en tant qu’individu, on ne peut pas déplacer des montagnes avec son droit de vote. En investissant dans un fonds, en revanche, toutes les forces sont concentrées et s’érigent tel un puissant glaive des investisseurs. «Cela fait la différence.»

À la prochaine…

Gouvernance mission et composition du conseil d'administration Normes d'encadrement

Repenser la gouvernance : 3 pistes pour le CA

Ivan Tchotourian 29 juillet 2020 Ivan Tchotourian

Douglas Chia dans Corporate Board Member offre une belle lecture sur les trois voies autour desquelles le CA pourrait penser la gouvernance d,entreprise de demain : « Three Ways for Boards to Rethink Governance ».

Extrait :

1. The Board’s Role: Rethink what the board is there to do.

Everyone agrees that the role of the board has changed over the past two decades, not from the perspective of a director’s fiduciary duties, but rather through stakeholders with increased expectations for what the board is there to do and lower tolerance for underperformance from their perspectives. For many boards, the ground that represents their role has noticeably shifted under their feet. But, when was the last time the board met in executive session for the express purpose of thinking about how the company’s stakeholders look at the board’s role and what that particular company needs from its board? Most annual board self-evaluations are brief sessions for the independent directors to ask each other “How do we think we’re doing?” without deeper thought about what it is they need to be doing to best serve that company.

Boards should set aside time to rethink their role in the context of the fundamental changes their companies will be facing going forward. A board can do this by taking its self-evaluation to the next level and by revisiting its charter, mission statement or governance principles as an exercise in rethinking its purpose. As companies face a new world order, it is more important than ever for the entire board to be on the same page for what it is there to do.

2. The Board’s Committees: Rethink whether the board’s committee structure is stakeholder-driven.

The tide of companies turning away from shareholder primacy and committing (or recommitting) to the stakeholder model of governance creates the conditions for boards to step back and look at how they allocate their attention to the interests of each of the commonly-thought-of key stakeholders: customers, employees, communities and shareholders. A board typically handles its agenda by covering high-level concerns at the full board level and delegating to its standing committees those subjects of particular importance to the company requiring more specific and deeper dives.

Currently, the committees prescribed by law are audit, compensation and nominating. These three committees are largely designed look after the direct interests of the shareholders. So, where do the direct interests of the other three stakeholders get covered? If the answer is “at the full board level,” it may be time to rethink whether that still works and if certain interests of stakeholders other than shareholders should receive deeper-dive treatment in committee. The board can do this by mapping each of the items it covers—both at the full board and in committees—to one or more of the four stakeholders. Upon doing this, it may become apparent that the allocation of the board’s time is out of balance, and the customers, employees, and communities could use more attention at the committee level.

This may mean adjusting or redesigning the structure and scope of the board’s committees. Some boards already have standing committees to cover subjects that relate more directly to its customers (e.g., risk, product safety, innovation) and communities (e.g., public policy). Recently, there have been calls for boards to “reimagine” the scope of their compensation committees to cover the company’s overall workforce and issues of human capital going far beyond executive compensation and benefits. It may be time for boards go even further to rethink whether its governance is truly stakeholder-driven and reimagine how to restructure its agenda and committees to understand and balance the interests of the corporation’s four key stakeholders.

3. The Board’s Resources: Rethink whether the board is sufficiently resourced versus sufficiently paid.

Before March 2020, director compensation had been on a steady, upward trend on the notion that directors are being asked to spend more and more time on their board duties and should be paid commensurate with the amount of work. During the COVID-19 pandemic, in addition to cutting the pay of the CEO and other executives, many boards have temporarily reduced director compensation, not so much hold down costs, but to show employees that the people with ultimate accountability are willing to impose real sacrifices on themselves. If the assumption is that director compensation will go back up to its original levels once business goes “back to normal,” boards need to rethink that.

Boards have felt the pile-on effect of stakeholders continually expecting them to oversee additional areas of concern and own them in a bigger way: political spending, climate change, cybersecurity, data privacy, human capital, artificial intelligence and now pandemic preparedness, just to name a few. Like with all individuals, while a director can be compensated for increased amounts of work, his or her capacity to do a good job will eventually reach its limit, regardless of how much you pay them. What they need are additional resources.

À la prochaine…