engagement et activisme actionnarial

actualités internationales engagement et activisme actionnarial Gouvernance

The Distribution of Voting Rights to Shareholders

Ivan Tchotourian 22 mars 2021 Ivan Tchotourian

Vyacheslav Fos et Clifford Holderness publient un article sur la distribution des droits de vote des actionnaires sur la bourse NYSE : « The Distribution of Voting Rights to Shareholders » (ECGI Finance Series 733/2021).

Résumé

This is the first comprehensive study of the distribution of voting rights to shareholders. Only those owning stock on the record date may vote. Firms, however, reveal that date after the fact 91% of the time. With controversial votes, firms are more likely to do the opposite, and this is associated with a lower passage rate for shareholder-initiated proposals.

The NYSE sells non-public record-date information to select investors. When stocks go ex vote, prices decline and trading volume often surges, suggesting that investors are buying marginal votes. These trends are most pronounced with controversial votes.

À la prochaine…

engagement et activisme actionnarial Gouvernance Normes d'encadrement normes de droit

The Law and Practice of Shareholder Inspection Rights: A Comparative Analysis of China and the U.S.

Ivan Tchotourian 23 avril 2020 Ivan Tchotourian

Une belle comparaison entre les droits étatsuniens et chinois à propos des droits d’inspection des actionnaires dans : R. Huang et R. Thomas, « The Law and Practice of Shareholder Inspection Rights: A Comparative Analysis of China and the U.S. », European Corporate Governance Institute – Law Working Paper No. 499/2020.

Extrait :

Shareholder inspection rights allow a shareholder to access relevant documents and records of their company, so as to address the problem of information asymmetry inherent in the corporate form, and facilitate monitoring of the operation of the company and, if necessary, the bringing of further action for remedies.

In the United States (U.S.), all states have now codified shareholder inspection rights, albeit with some significant differences amongst them. Drawing upon overseas experiences such as the U.S. law, China has introduced the regime of shareholder inspection rights, but with some important adaptions made to its local environment. By providing access to relevant information, inspection rights have the potential to serve as an effective mechanism to deal with different types of agency problems in the company: not only the manager–shareholder conflict that is the most serious agency problem in the U.S., but also the conflict between majority and minority shareholders which mainly plagues the corporate governance system in China.

However, due to institutional differences, variations may exist between the two jurisdictions as to how inspection rights are structured and enforced. In our recent article, we thus compare shareholder inspection rights in China and the U.S. (that is mostly represented by Delaware, the preeminent corporate law jurisdiction in the U.S.), both in terms of the law on the books and the law in practice.

(…) Overall, we find that shareholder inspection rights play an important role in both the Chinese and US legal systems. While Chinese corporate governance and American corporate governance face different sets of agency cost problems, improved shareholder monitoring creates important benefits in both of them. There exist, however, some important differences in the structure and enforcement of the inspection rights regime between the two jurisdictions, which can be largely explained by reference to their different contexts of political economy.

À la prochaine…

actualités internationales engagement et activisme actionnarial Gouvernance Normes d'encadrement Nouvelles diverses

SEC et agences de conseil en vote : ça bouge !

Ivan Tchotourian 13 septembre 2019 Ivan Tchotourian

Intéressante information de The Advisor-s Edge concernant les agences de conseil en vote : « Updated: SEC addresses proxy voting concerns » (21 août 2019).

Extrait :

The U.S. Securities and Exchange Commission (SEC) set out its views on investment advisors fulfilling their proxy voting responsibilities. The guidance states that proxy voting advice constitutes a “solicitation” under federal rules and provides instructions on applying anti-fraud rules to proxy voting advice.

“Advisers who vote proxies must do so in a manner consistent with their fiduciary obligations and, to the extent they rely on voting advice from proxy advisory firms they must take reasonable steps to ensure the use of that advice is consistent with their fiduciary duties,” said SEC commissioner Elad Roisman, who led development of the new guidance.

“In addition, proxy advisory firms, to the extent they engage in solicitations, must comply with applicable law,” he noted.

Pour accéder au texte de la SEC : « Commission Guidance Regarding Proxy Voting Responsibilities of Investment Advisers » (17 CFR Parts 271 and 276)

Résumé :

The Securities and Exchange Commission (the “SEC” or the “Commission”) is publishing guidance regarding the proxy voting responsibilities of investment advisers under Rule 206(4)-6 under the Investment Advisers Act of 1940 (the “Advisers Act”), and Form N-1A, Form N-2, Form N-3, and Form N-CSR under the Investment Company Act of 1940 (the “Investment Company Act”).

À la prochaine…

engagement et activisme actionnarial Gouvernance normes de droit

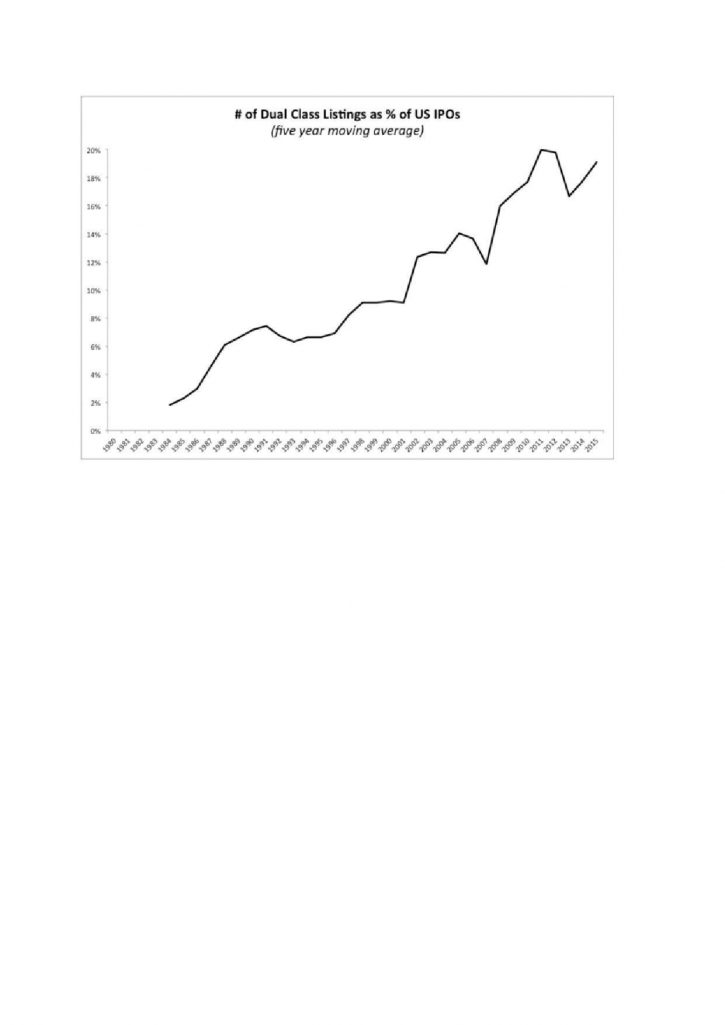

Capital-actions à classe multiple : le graphique qui donne à réfléchir

Ivan Tchotourian 21 mars 2018 Ivan Tchotourian

Un rapport à paraître de l’Investor Advisory Committee de la SEC montre qu’entre 2005 et 2015, le nombre de sociétés cotées comportant des classes d’actions à droit de vote multiple a augmenté de 44%. La liste inclut Google, Facebook, Snap, LinkedIn, Nike… La courbe reproduite ci-dessous parle d’elle-même.

Merci au professeur Alain Pietrancosta de cette information diffusée sur LinkedIn !

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance normes de droit

Agences de conseil en vote : un projet de loi américain qui ressurgit

Ivan Tchotourian 12 janvier 2018

Bonjour à toutes et à tous, sacré nouvelle dans le domaine des agences de conseil ! Selon The Hill, « Congress should end corporate governance conflicts for investors » (8 janvier 2018). Un nouveau projet de loi vient d’être déposé pour encadrer les conflits d’intérêts des agences de conseil en vote : « H.R. 4015 – Corporate Governance Reform and Transparency Act of 2017 ».

In late December, the U.S. House of Representatives passed the Corporate Governance Reform and Transparency Act on a bipartisan basis. This bill is good news for investors in our capital markets, managers, employees, and other stakeholders of public corporations.

The Corporate Governance Reform and Transparency Act is squarely focused on addressing this conflict. The bill requires governance and proxy advisors to disclose to the U.S. Securities and Exchange Commission any conflict of interest they have when advising institutional investors on how to vote on various proxy items. It also provides for a standard process and timeframe for companies to review and provide feedback to the governance and proxy advisors on important company decisions including proxy items, before the advisors send their recommendations to investors.

Pour rappel, en juin 2016, un projet de loi intitulé « Corporate Governance Reform and Transparency Act » a été introduit à l’initiative du Comité sur les services financiers de la chambre des représentants devant le 114e congrès (H.R. 5311, Corporate Governance Reform and Transparency Act, 114e congrès, 2e session, Union Calendar no. 621, Report no. 114-798). Bien que ce projet de loi ait disparu de l’agenda législatif avec la fin du 114e congrès, son étude témoigne d’une volonté politique d’adopter une ligne plus dure envers les agences de conseil en vote. Afin d’« (…) améliorer la qualité des agences de conseil en vote pour la protection des investisseurs et de l’économie américaine, dans l’intérêt public, en encourageant la responsabilité, la transparence, la réactivité et la concurrence dans l’industrie du conseil en vote », ce projet propose la modification du Securities Exchange Act of 1934 pour imposer aux agences plusieurs obligations, dont celle d’être enregistrée auprès de la SEC.

Dans ses grandes orientations, cette réforme établissait une procédure exigeant des agences de conseil en vote qu’elles soumettent de nombreux documents et informations (notamment sur leur structure organisationnelle, sur les procédures en place relativement à la gestion des conflits d’intérêts et sur les procédures et la méthodologie utilisée pour en arriver à des recommandations de vote) afin d’obtenir une certification obligatoire pour poursuivre leurs activités. L’information fournie à cette occasion, ainsi que toute information subséquente contenue dans des mises à jour, était rendue publique sous réserve d’exceptions. Le projet de loi visait aussi à imposer aux agences de conseil en vote la mise en place de procédures raisonnables permettant aux entreprises de recevoir une version préliminaire des recommandations et de disposer d’un délai pour fournir leurs commentaires. Enfin, les agences se voyaient contraintes de mettre en place un ombudsman afin de recevoir les plaintes des entreprises, plaintes qui doivent être traitées dans un délai raisonnable et avant que ne se tienne le vote.

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance normes de droit

Capital-actions à classe multiple au moment d’une IPO : le « Yes we can » de Bernard Sharfman

Ivan Tchotourian 28 août 2017

Dans l’Oxford Business Law Blog, Bernard Sharfman revient sur la création de multiples classes actions notamment au moment de la première entrée en bourse d’une entreprise pour en souligner… tous les points positifs : « How Dual Class Shares in IPOs Can Create Value » (25 août 2017).

Une conclusion qui ne laisse guère place aux doutes :

The shareholder empowerment movement (the ‘movement’), driven primarily by public pension funds and union-related funds with over $3 billion in assets, has renewed its effort to eliminate, restrict, or at least discourage companies from creating dual class share structures in initial public offerings (IPOs). The impetus was the issuance of non-voting stock in the recent Snap Inc. IPO. Such advocacy, if successful, would not be trivial, as many of our most valuable and dynamic companies, including Alphabet (Google) and Facebook, have gone public by offering shares with unequal voting rights.

The movement’s vigorous response to Snap Inc.’s hugely successful IPO was unsurprising. The Council of Institutional Investors (CII), the trade organization that has represented the movement since its founding in 1985, has promoted as a bedrock principle a ‘one share, one vote’ policy. Dual class share structures clearly violate this policy and are an obvious threat to the power of the movement. That is, a public company that provides control to insiders through a dual class share structure can more easily resist the demands of the movement.

In my paper, ‘A Private Ordering Defense of a Company’s Right to Use Dual Class Share Structures in IPOs’, I rely on Zohar Goshen and Richard Squire’s newly proposed ‘principal-cost theory’ to argue that dual class shares in IPOs is a value enhancing result of private ordering, making the movement’s renewed advocacy unwarranted.

Récemment, dans un article publié sur le blogue Contact de l’Université Laval (« Snapchat et le capital-actions à classe multiple », 8 mars 2017), j’ai soulevé les doutes sur ce genre de structuration du capital sans toutefois pleinement exclure la pertinence de créer plusieurs catégories d’actions.

Les questions sont donc nombreuses et justifient que les analystes soient réservés. L’effet Snap Inc. sera-t-il durable? Les actionnaires qui ont investi leur argent en acceptant les risques vont-ils être gagnants? Je ne parierais pas ma chemise là-dessus…

Il y a une certitude dans ce monde d’incertitude: le capital-actions à classe multiple a un bel avenir, encore plus lorsqu’il est utilisé de manière innovante et que des investisseurs acceptent le jeu. Tous les doutes sur la légitimité d’aménager la structure de capital d’une entreprise ne sont pas levés, même si le cas Snap Inc. démontre que les investisseurs (du moins certains) ne sont pas si attachés à la démocratie actionnariale et que le capital-actions à classe multiple peut servir des intérêts court-termistes.

À la prochaine…

Ivan Tchotourian

divulgation financière engagement et activisme actionnarial Gouvernance

Changement climatique : BlackRock met la pression sur les entreprises

Ivan Tchotourian 15 mars 2017

En voilà une nouvelle ! Le gérant américain d’actifs BlackRock a fait savoir qu’il entendait s’intéresser à la manière dont les entreprises géraient les problèmes liés au changement climatique : « Exclusive: BlackRock vows new pressure on climate, board diversity » (Reuters, 13 mars 2017).

BlackRock Inc(BLK.N), which wields outsized clout as the world’s largest asset manager, planned on Monday to put new pressure on companies to explain themselves on issues including how climate change could affect their business as well as boardroom diversity.

The move by BlackRock, a powerful force in Corporate America with $5.1 trillion under management, could bolster efforts like climate-risk disclosure practices developed by the Financial Stability Board, the international body that monitors and makes recommendations about the global financial system.

BlackRock, which holds stakes in most major U.S. corporations, identified its top « engagement priorities » for meetings this year with corporate leaders in documents to be posted on its website on Monday, with climate risk and boardroom diversity on the list. Reuters received advance copies of the materials.

Quand on connaît le poids de ce gérant d’actifs, il y a peut-être de l’avenir pour le changement climatique !

À la prochaine…

Ivan Tchotourian