Valeur actionnariale vs. sociétale

Gouvernance objectifs de l'entreprise parties prenantes Valeur actionnariale vs. sociétale

Can a Broader Corporate Purpose Redress Inequality? The Stakeholder Approach Chimera

Ivan Tchotourian 27 mai 2020 Ivan Tchotourian

C’est sous ce titre que les professeurs Gatti et Ondersma amène à une réflexion critique sur l’ouverture de l’objectif des entreprises à la théorie des parties prenantes : « Can a Broader Corporate Purpose Redress Inequality? The Stakeholder Approach Chimera » (4 mars 2020).

Our paper also rebuts the premise that shareholder primacy is a key contributor to economic stagnation and inequality. To be sure, shareholder primacy may have contributed to concentration and monopsony in labor markets, excessive executive compensation, the decline in workers’ prerogatives, and tax cuts. But so might the stakeholder approach. Note that a stakeholder approach can hardly fix the central drivers of stagnation and inequality. Globalization, technology, and education cannot be addressed by corporate boardrooms alone. Similarly, collective action dynamics suggest that we cannot expect boards to retreat from further concentration. Experiences with constituency statutes and the battles between large corporations and organized labor tell us that boards won’t improve worker protections without regulation. Implementing legislative or regulatory measures would be much more effective in addressing stagnation and inequality than would be a change in corporate purpose.

In fact, stakeholderism is likely counter-productive. It would give corporations both a sword and a shield with which to defend the status quo.

First, managers and directors can play offense by expanding lobbying efforts, purportedly in the interest of all stakeholders, thus risking corporate capture of the reformist agenda. Second, corporations can deploy stakeholderism defensively by arguing that no direct regulation is needed. Like others, we take a cynical view of the Business Roundtable’s Statement on Corporate Purpose and Martin Lipton’s “New Paradigm,” which includes regulatory preemption as an express purpose. Meanwhile, a switch to a stakeholder approach would require diverting momentum for change into significant political capital in order for it to be adopted – and once adopted, enshrined in against further change. Thus, the pursuit of a stakeholder approach would deplete time, energy, and resources necessary to pass reforms to reduce inequality, such as tax, antitrust, and labor measures – precisely the changes most likely to meaningfully distribute power and resources to employees and other weaker constituents.

The Covid-19 pandemic exacerbates this concern. As many businesses cannot survive without government aid, some have accepted conditions for receiving bailout money, primarily with respect to stock buy-backs and dividend payouts. We speculate that, at some point, businesses might find it convenient to simply offer, in exchange for further government relief, a formal adoption of a stakeholder approach in their charter. This would preempt more onerous restrictions while preserving the status quo.

As disastrous as the current economic situation is, it also offers a rare opportunity to rethink and possibly reset certain policies. There is little choice but to depart from the tradition of tinkering with corporate governance and instead identify more effective tools to address inequality (mainly in labor, antitrust, and tax laws). This will undoubtedly require greater collaboration across fields and disciplines.

À la prochaine…

Gouvernance Normes d'encadrement Nouvelles diverses objectifs de l'entreprise

COVID-19 : la fin de la théorie de l’agence ?

Ivan Tchotourian 6 avril 2020 Ivan Tchotourian

Bel article de M. Barker sur LinkedIn intitulé : « The irrelevance of agency theory during the Covid-19 crisis » (5 avril 2020). Il est effectivement temps de revoir le modèle de l’agence et sa place comme paradigme central de toute réflexion sur la gouvernance d’entreprise : d’autres modèles existent, il est bon de le rappeler !

Extrait :

The implicit mistrust between principals and agents must be replaced by a pooling of resources and know-how, and a more cooperative attitude to other stakeholders such as employees and society as a whole.

Corporate governance scholars have developed a range of alternative theoretical paradigms through which to embody this more team-based approach, including stewardship theory, stakeholder theory and resource dependency theory. These frameworks seem to offer a more relevant perspective on what we should demand from corporate governance during the crisis.

A first is that non-executive directors should see themselves as sharing more of a common agenda with management. They must be prepared to work side by side with them in order to overcome the profound challenges being faced by most organisations at the current time.

Second, investors will have to exhibit greater trust in boards and management. Once they are satisfied that the right leadership is in place, they need to let them get on with it.

Third, it becomes more important than ever for boards to understand and incorporate into decision-making the different perspectives of groups whose motivation and participation is critical to the survival of the organisation. These will include middle managers, employees, customers, suppliers and the wider community.

Finally, we should not view existing shareholder rights as sacrosanct during the crisis. Shareholder rights are not the same thing as human rights, which should never be seen as negotiable. Rather, they are pragmatic arrangements that have been established in order to underpin the prosperity of the economy as a whole.

À la prochaine…

finance sociale et investissement responsable normes de droit objectifs de l'entreprise

Nouvelle publication sur Contact : discussion sur l’objet social comme véhicule de la RSE

Ivan Tchotourian 3 février 2018 Ivan Tchotourian

Bonjour à toutes et à tous, mon nouveau billet de Contact est maintenant en ligne : « Des lois pour des entreprises plus responsables? – 1re partie » (1er février 2018). Le sujet est hautement brûlant puisqu’il aborde la pertinence de modifier la loi pour imposer la prise en compte de la RSE dans l’objet social des entreprises.

La France réfléchit à une modification de l’objet social de l’entreprise (la définition de ses activités) pour l’ouvrir aux préoccupations de responsabilité sociétale (ci-après « RSE »). Dans le cadre de son « plan d’action pour la croissance et la transformation des entreprises » (loi PACTE) dévoilé le 22 octobre 2017, le gouvernement français souhaite en effet mettre en place d’un statut d’« entreprises de mission » sur le modèle des Benefit corporations américaines (voir ici ). Une mission sur la question de l’objet social des entreprises a été lancée le 5 janvier 2018 afin de faire converger les positions. Ce plan d’action s’inscrit dans plusieurs initiatives (…).

Ces propositions françaises s’orientent autour de 2 idées : modifier le Code civil pour proposer un nouvel objet social ou aller jusqu’à créer une nouvelle forme de société par actions imposant la poursuite d’une mission sociétale (une entreprise hybride).

Pour les juristes canadiens qui se penchent sur les interactions entre les sphères économiques et sociales dans une perspective entrepreneuriale, une interrogation se pose : faudrait-il légiférer pour définir un nouvel objet social et repenser la mission des entreprises pour y intégrer la RSE? Faudrait-il faire place à une société par actions à vocation sociale? En d’autres termes, le Canada devrait-il s’inspirer des initiatives françaises et modifier ses lois (Code civil du Québec ou lois sur les sociétés par actions)?

Je vous laisse découvrir la suite sur Contact !

À la prochaine…

Ivan Tchotourian

devoirs des administrateurs Gouvernance objectifs de l'entreprise Valeur actionnariale vs. sociétale

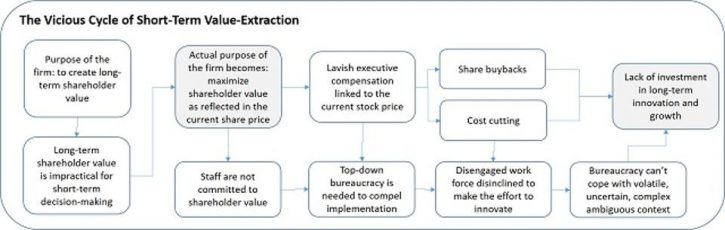

Maximisation de la valeur actionnariale : une belle critique

Ivan Tchotourian 6 février 2017

Bonsoir à toutes et à tous, dans « Resisting The Lure Of Short-Termism: Kill ‘The World’s Dumbest Idea' » publié dans Forbes, Steve Denning revient sur une belle critique de la maximisation de la valeur actionnariale comme objectif des entreprises.

When pressures are mounting to deliver short-term results, how do successful CEOs resist those pressures and achieve long-term growth? The issue is pressing: low global economic growth is putting stress on the political and social fabric in Europe and the Americas and populist leaders are mobilizing widespread unrest. “By succumbing to false solutions, born of disillusion and rage,” writes Martin Wolf in the Financial Times this week, “the west might even destroy the intellectual and institutional pillars on which the postwar global economic and political order has rested.”

The first step in resisting the pressures of short-termism is to correctly identify their source. The root cause is remarkably simple—the view, which is widely held both inside and outside the firm, that the very purpose of a corporation is to maximize shareholder value as reflected in the current stock price (MSV). This notion, which even Jack Welch has called “the dumbest idea in the world,” got going in the 1980s, particularly in the U.S., and is now regarded in much of the business world, the stock market and government as an almost-immutable truth of the universe. As The Economist even declared in March 2016, MSV is now “the biggest idea in business.”

À la prochaine…

Ivan Tchotourian

Gouvernance Valeur actionnariale vs. sociétale

Le court-terme dénoncé

Ivan Tchotourian 14 juin 2016

Belle tribune de M. Gérard Bérubé dans Le Devoir du 11 juin : « Les ravages du court terme ». Ce dernier revient sur ce qu’il appelle – à juste titre – le diktat qui se se trouve pérenniser par une politique de rémunération des hauts dirigeants basée sur des indicateurs incitant à la performance à court terme. Comme l’auteur le note, « on pense à un bénéfice par action cible et à un objectif de rendement total pour l’actionnaire ».

Le cri du coeur est venu cette semaine d’un cabinet de services comptables. PwC a dit s’inquiéter de la vision à court terme des actionnaires. PwC faisait le bilan 2015 de l’industrie minière. Une année « caractérisée par une dégringolade générale ». Les 40 plus grandes sociétés minières ont enregistré collectivement une perte nette pour la première fois. Leur capitalisation boursière a fondu de 37 %, effaçant « tous les gains réalisés durant le supercycle des matières premières ». Le cabinet d’ajouter : « À l’échelle mondiale, on s’inquiète de la vision à court terme des actionnaires, qui se concentrent sur la variation des prix des matières premières et privilégient les rendements à court terme plutôt que l’horizon de placement à long terme indispensable dans le domaine minier. »

À la prochaine…

Ivan Tchotourian

Normes d'encadrement Nouvelles diverses objectifs de l'entreprise Valeur actionnariale vs. sociétale

Les profits des entreprises : un problème ?

Ivan Tchotourian 8 avril 2016

Larry Summers s’interroge dans un article du 3 mars 2016 sur les problèmes que soulèvent les profits records des entreprises américaines : « Corporate profits are near record highs. Here’s why that’s a problem ».

As the cover story in this week’s Economist highlights, the rate of profitability in the United States is at a near-record high level, as is the share of corporate revenue going to capital. The stock market is valued very high by historical standards, as measured by Tobin’s q ratio of the market value of the nonfinancial corporations to the value of their tangible capital. And the ratio of the market value of equities in the corporate sector to its GDP is also unusually high. All of this might be taken as evidence that this is a time when the return on new capital investment is unusually high. The rate of profit under standard assumptions reflects the marginal productivity of capital. A high market value of corporations implies that “old capital” is highly valued and suggests a high payoff to investment in new capital. This is an apparent problem for the secular stagnation hypothesis I have been advocating for some time, the idea that the U.S. economy is stuck in a period of lethargic economic growth.

À la prochaine…

Ivan Tchotourian

Gouvernance Nouvelles diverses objectifs de l'entreprise

Un anniversaire à oublier ?

Ivan Tchotourian 11 février 2016

La journaliste du magazine Challenges Alice Mérieux revient dans le cadre d’un article intéressant (« ArcelorMittal a dix ans : le bilan désastreux d’une fusion ») sur les 10 ans de la fusion importante qui a eu lieu au début des années 2000 entre Arcelor et Mittal… tout cela pour un bilan bien mitigé quelques années plus tard !

Drôle d’anniversaire. A dix ans, la fusion du sidérurgiste Mittal Steel avec son rival européen Arcelor, n’a toujours pas fait la preuve de son efficacité. Le géant fusionné, ArcelorMittal, annonce aujourd’hui des pertes nettes monumentales de près de huit milliards de dollars. Et lance un vaste plan de réduction de sa dette de quatre milliards de dollars grâce à une lourde augmentation de capital – de trois milliards de dollars – et la cession d’une participation dans l’équipementier Gestamp – pour un milliard de dollars de plus. A vue de nez, le bilan de l’OPA apparaît pour le moins sombre.

À la prochaine…

Ivan Tchotourian