David Larcker, Bradford Lynch, Brian Tayan et Daniel Taylor publient un texte qui revient sur la transparence des ghrandes entreprises américaines en matière de COVID-19 « The Spread of Covid-19 Disclosure » (29 juin 2020). Un document plein de statistiques et de tendances sur la transparence… vraiment intéressant sachant que l’enjeu de la question n’est pas à négliger.

Extrait :

The COVID-19 pandemic presents an interesting scenario whereby an unexpected shock to the economic system led to a rapid deterioration in the economic landscape, causing sharp changes in performance relative to expectations just a few months prior. For most companies, the pandemic has been detrimental. For a few, it brought unexpected demand. In many cases, supply chains have been strained, causing ripple effects that extend well beyond any one company.

How do companies respond to such a situation? What choices do they make, and how much transparency do they offer? How does disclosure vary in a setting where the potential impact is so widely uncertain? The COVID-19 pandemic provides a unique setting to examine disclosure choices in a situation of extreme uncertainty that extends across all companies in the public market. This devastating outlier event provides a rare glimpse into disclosure behavior by managers and boards.

Why This Matters

The COVID-19 pandemic provides a unique opportunity to examine disclosure practices of companies relative to peers in real time about a somewhat unprecedented shock that impacted practically every publicly listed company in the U.S. We see that decisions varied considerably about whether to make disclosure and, if so, what and how much to say about the pandemic’s impact on operations, finances, and future. What motivates some companies to be forthcoming about what they are experiencing, while others remain silent? Does this reflect different degrees of certitude about how the virus would impact their businesses, or differences in managements’ perception of their “obligations” to be transparent with the public? What does this say about a company’s view of its relation and duty to shareholders?

In one example, we saw a consumer beverage company make zero references to COVID-19 in its SEC filings and website, despite the virus plausibly having at least some impact on its business. In another example, we saw a company claim no material changes to its previously reported risk factors when managers almost certainly had relevant information about the virus and the likely impact on sales and operations. What discussion among the senior managers, board members, external auditor, and general counsel leads to a decision to make no disclosures? What should shareholders glean from this decision, particularly in light of peer disclosure?

The COVID-19 pandemic represents a so-called “black swan” event that inflicted severe and unexpected damage to wide swaths of the economy. What strategic insights will companies learn from this event? Can boards use these insights to prepare for other possible outlier events, such as climate events, terrorism, cyber-attacks, pandemics, and other emergencies? Should these insights be disclosed to shareholders?

C’est en pleine période de crise liée à la COVID-19 que le gouvernement du Québec a finalement adopté, le 17 mars 2020, la Loi concernant principalement la mise en œuvre de certaines dispositions des discours sur le budget du 17 mars 2016, du 28 mars 2017, du 27 mars 2018 et du 21 mars 2019 reprenant une partie des mesures qui avaient été annoncées afin de favoriser la transparence corporative et la fiabilité des informations présentées au REQ.

Cette loi modifie entre autres la Loi sur la publicité légale des entreprises (chapitre P-44.1) (la « Loi ») afin de, notamment :

permettre au REQ d’exiger des documents ou informations pour valider l’exactitude des déclarations déposées au REQ ou d’un document transféré à un ministère ou à un autre organisme du gouvernement (article 74.1 de la Loi);

ajouter les noms et domiciles des trois actionnaires qui détiennent le plus de voix à la liste des informations opposables aux tiers de bonne foi (article 98 de la Loi);

élargir la liste des organismes québécois ayant un pouvoir d’enquête qui pourront conclure des ententes avec le REQ afin de communiquer tout ou partie des informations contenues au registre, les mises à jour qui y sont apportées, ainsi que les renseignements ou documents obtenus pour valider l’exactitude des déclarations (article 121 de la Loi);

fixer le délai de prescription d’une poursuite pénale à un an depuis la date de la connaissance par le poursuivant de la perpétration de l’infraction sans qu’il se soit écoulé plus de cinq ans depuis la date de la perpétration de l’infraction (article 163.1 de la Loi);

conférer au ministre responsable, dans certaines circonstances exceptionnelles, le pouvoir de renoncer au paiement d’un droit, d’une pénalité ou de frais (article 79.1 de la Loi).

Les entreprises faisant affaire au Québec devront donc s’attendre à devoir démontrer la véracité des informations à être déclarées au REQ en transmettant, par exemple, des copies des résolutions dûment adoptées ou de toute autre documentation corporative. À cet effet, nous soulignons l’importance de toujours préparer et conserver les documents corporatifs nécessaires et conformes aux obligations légales requises par la loi constitutive de votre société au soutien des éléments qui doivent être déclarés au REQ.

L’étendue des documents pouvant être demandés demeure toutefois incertaine et certains se questionnent à savoir si le REQ pourrait, par exemple, exiger d’obtenir copie d’une convention unanime des actionnaires intervenue.

La question est importante, puisque comme auparavant, le REQ peut communiquer en tout ou en partie les informations et documents recueillis avec un ministère, un organisme ou une entreprise du gouvernement avec lequel le REQ a, au préalable, conclu une entente. La Loi prévoyait déjà ce droit avant l’arrivée des nouvelles modifications entre autres pour certains ministères et organismes comme Revenu Québec. Les modifications adoptées à la Loi ajoutent maintenant à cette liste :

les organismes municipaux visés à l’article 5 de la Loi sur l’accès aux documents des organismes publics et sur la protection des renseignements personnels (chapitre A-2.1);

les organismes dont le personnel est nommé suivant la Loi sur la fonction publique (chapitre F-3.1.1), et;

“The future of business will be different,” surmised a director on a recent virtual board roundtable hosted by RSR Partners, “in ways we can’t anticipate in this moment. Our board is focused on assessing whether all our directors are truly ready for what’s coming.”

Over the past few months, RSR Partners hosted more than a dozen roundtables for sitting directors, providing a forum for the participants to share what their boards are learning as they navigate the current crisis and pivot into the “new normal.” While tackling topics as diverse as commercial strategy, operations, health and safety, and the future of business, one theme was pervasive throughout the discussions: leadership and stakeholders will be looking to the boardroom for guidance, and board members not only need to have the requisite experience and skills to confidently provide direction, but the leadership characteristics that will allow them to be effective.

Fundamentally, the global business disruption and current uncertainty has created a need for a higher level of involvement from board members. “This is a time to have board members who have experienced really tough issues, such as major ecessions, difficult mergers, major cost cutting, insolvency and bankruptcy, and top management departures, along with experience in reinventing companies, including supply chain, product engineering and simplification, digital transformation, offshore manufacturing and procurement, sale of subsidiaries, and comprehensive refinancing,” stated Edward A. Kangas, former Chairman and CEO of Deloitte Touche. “This is not a time for deep thinking. It’s time for people with real experience who know how to oversee and support management in a time of crisis and reinvention.” (Mr. Kangas currently serves on the following boards: Deutsche Bank USA Corp., Intelsat SA, VIVUS, Inc., and Hovnanian Enterprises, Inc.).

Characteristics of Directors Who Succeed in the “New Normal”

From a practical perspective, there is now a higher premium placed on a director’s proven ability to navigate a business through a crisis while mitigating risk and understanding how and when to pull the levers that will impact balance sheets. The demand to optimize results, sustain business, and adapt to changes in a regional and global market has increased alongside the time commitment and attention to detail required of directors to address these issues. Normal requirements for sound governance, audit oversight, compensation strategies, business performance goals, and succession of key leadership have continued to be paramount during the crisis. However, what the current crisis has forced boards to recognize is that a combination of specialized and diversified skillsets and characteristics will produce good corporate governance in and after 2020.

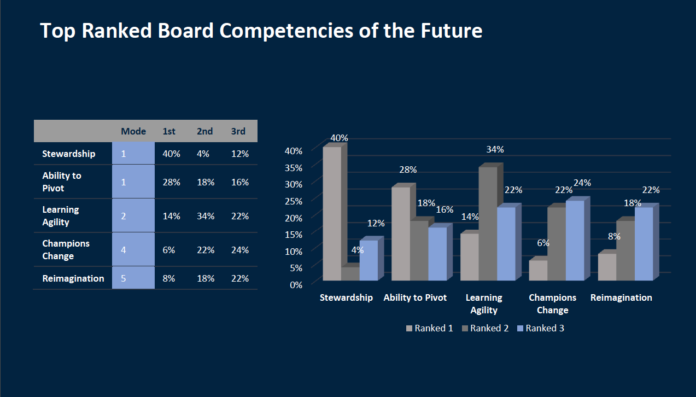

In addition to listening to the characteristics discussed in the recent roundtables, RSR Partners polled more than 250 public company board members of Fortune 50-1000 companies to identify the traits they hope to see emerge in this generation of board members. The results indicated that stewardship, the ability to pivot and learn agility, to be a champion of change, and to be capable of reimagination will be most needed by the directors charged with steering their boards in the “new normal.”

Les hedge funds n’échappent pas à la vague verte qui submerge le monde de l’investissement, des banques centrales aux gérants d’actifs. Marshall Wace, le redoutable hedge fund anglais , va lancer un nouveau fonds de 1 milliard de dollars selon le « Financial Times ». Il achètera les sociétés vertueuses qui respectent l’environnement, les droits sociaux et affichent une bonne gouvernance. Il sanctionnera les mauvais élèves en les vendant à découvert et exclura de son univers d’investissement les « actions du péché » (armement, tabac…). Lansdowne, un des principaux concurrents de Marshall Wace, va fermer un de ses principaux fonds pour cause de contre-performance. Va-t-il lui aussi « se mettre au vert » et lancer un fonds ISR ?

Les hedge funds veulent opportunément profiter de l’engouement massif pour l’investissement socialement responsable. Ils diversifient leurs stratégies, sources de revenus et clientèle tout en redorant leur image.

Le Ministère du travail américain soumet à commentaire une proposition inquiétante pour l’investissement responsable. Cette proposition est détaillée dans l’Harvard Law School Forum on Corporate Governance : « DOL Proposes New Rules Regulating ESG Investments » (7 juillet 2020).

Extrait :

The Department of Labor (“DOL”) has proposed for public comment rules that would further burden the ability of fiduciaries of private-sector retirement plans to select investments based on ESG factors and would bar 401(k) plans from using a fund with any ESG mandate as the default investment alternative for non-electing participants.

The proposed rules would prohibit a retirement plan fiduciary from making any investment, or choosing an investment fund, based on the consideration of an environmental, societal or governmental factor unless that factor independently represents a material economic investment consideration under generally accepted investment theories or serves as a tiebreaker in what the DOL characterizes as the rare case of economically equivalent investments. In order to select an investment with an ESG component, the plan fiduciaries would be required to compare investments or strategies on “pecuniary” factors such as diversification, liquidity and rate of return. Specific documentation would be required for the tiebreaker justification and for the selection and monitoring of an investment alternative in a 401(k) plan that includes ESG in its mandate or fund name. Most significantly, the proposed rules would prohibit a 401(k) plan from providing a qualified default investment alternative (“QDIA”) with an ESG component, no matter how small, even if that investment alternative satisfies the pecuniary factor requirements.

As businesses start to look beyond the COVID-19 crisis, the EY Global Integrity Report 2020 reveals divisions on the repercussions for company ethics as a result of the pandemic.

The findings are part of a survey of almost 3,000 respondents from 33 countries up to February 2020, analyzing the ethical challenges companies face in turbulent times. An additional 600 employees across all levels of seniority were surveyed at the height of the COVID-19 crisis in April in companies across six countries – China, Germany, Italy, the UK, India and the US.

The majority (90%) of respondents surveyed during the crisis believe that disruption, as a result of COVID-19, poses a risk to ethical business conduct, but there is a concerning disparity between boards, senior management and employees on the implications for compliance. While 43% of board members and 37% of senior managers surveyed believe the pandemic could lead to change and better business ethics, only 21% of junior employees appear to agree.

The survey highlights that signs of an integrity disconnect at different levels within organizations were evident even before the pandemic with more than half of board members (55%) believing management demonstrate professional integrity, but only 37% of junior employees sharing the same sentiment. In addition, over half of board members (55%) believe there are managers in their organization who would sacrifice integrity for short term gain.

La crise de la COVID-19 met en relief l’importance de l’investissement responsable. Deux consultantes expertes dans le domaine invitent les comités de retraite à préparer les bonnes questions à poser à leurs gestionnaires de portefeuille.