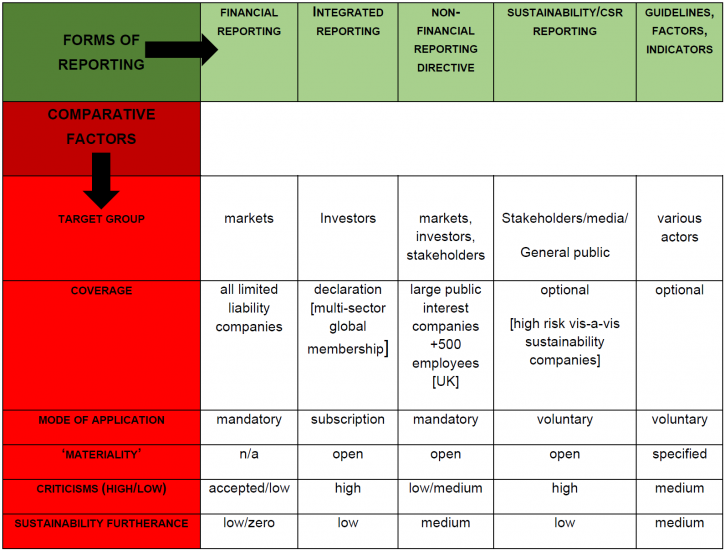

Random and arbitrary compliance with various initiatives makes companies’ sustainable practices ‘less’ rather than ‘more’ transparent. Our paper offers a comprehensive view on different reporting frameworks. It shows that there is a need to provide some clarity in this complex landscape. Fundamentally, the current reporting landscape is unlikely to impact positively on efforts towards sustainability. We suggest in our paper hat the scope of the NFRD, as the most promising of the existing initiatives, should be revisited so as to enhance its contribution to furthering corporations’ sustainable practices. Our paper supports reform of the NFRD which has constituted a positive step in the right direction. What is required now is stronger guidance on what to report and how to report it. Steps are being taken in the right direction towards clarifying metrics around sustainability (World Economic Forum 2020). A standardized and streamlined framework is necessary in order to pin companies down to something more concrete, rather than giving them too much choice on which guidelines, frameworks or recommendations they may opt to follow. Stronger, clearer and more concrete definitions of key concepts are required, as well as clarification of the rights of stakeholders in this area of activity. Proposals for reform that have arisen, with a consultation exercise by the European Commission, (European Commission Consultation 2020) are therefore to be welcomed. We suggest an expansion of the NFRD’s scope and that it represent sustainability as a positive instead of reducing the focus only to negative risks. EU member states and companies should have opportunities for effective compliance with the reporting requirements, with the NFRD better defining the concepts it refers to.

Now the consensual German model of business has suffered multiple mechanical failures. Wirecard, the payments group that bolstered German tech credentials, has imploded in fraud. Bayer is taking up to $11bn in charges mostly triggered by a disastrous US takeover. Once-proud conglomerates Siemens and Thyssenkrupp are shrinking. Volkswagen’s service life shortens each time Tesla’s outlook improves.

(…) Germany, can we talk? “Sure. I’m driving but I’m German so that’s second nature,” jokes an economist via his hands-free, “I don’t think there is any common thread between Wirecard and these other examples.” According to him, the worst accidents occur when German business adopts US ways. Wirecard had a two-tier board structure, like most German businesses. But its supervisory board was seemingly full of corporate yespersons, not vigilant workers as governance rules dictate. And the group was led by a bossy entrepreneur. Kenneth Amaeshi, a professor of business at Edinburgh university, disagrees with such exceptionalism. He believes the Wirecard scandal puts German stakeholder capitalism “in the dock”. It points to a structural weakness of regulation, he says. He is right.

(…) Corporate governance must be overhauled this time.

Supervisory boards must shrink, meet more often and include more independent directors. Regulators must adopt the adversarial approach of US peers. Industrial giants should unbundle further to create a new tier of focused medium-sized businesses. Siemens’ 2018 flotation of Healthineers, a healthcare equipment unit, shows what can be done. Germany’s biggest challenge is spurring investment in disruptive technology. Business has depended on debt finance from risk-averse investors. But there is no lack of equity, as Guntram Wolff of Bruegel, a think-tank, points out. It features as retained corporate earnings rather than footloose investment capital. This is reflected in total equity of some €1.2tn on the balance sheets of Germany’s top 100 quoted companies, according to S&P Global data. Tax breaks are needed to chivvy more of this capital into start-ups and electric vehicle development. It would be a shame to waste two good crises — the meltdown of the German model plus coronavirus. Moreover, support is growing worldwide for stakeholder capitalism, in which social and environmental goals rank alongside profits. Germany just needs to reduce its emphasis on safe jobs for workers and well-networked managers. A little less consensus can make the German model roadworthy again.

Selon une étude révélée par le Financial Times, peu suspect d’anticapitalisme primaire, les dividendes de 2019 pourraient compromettre la survie de bien des entreprises en 2020. 37 % des sociétés qui composent l’indice américain S&P 500 ont versé, en 2019, des dividendes (ou procédé à des rachats d’actions, ce qui est équivalent) pour un montant supérieur à l’ensemble de leurs bénéfices nets de l’année. C’est un peu moins en Europe, autour de 29 %.

Or, un tiers des entreprises a versé en 2019 plus que ce qu’elles ont gagné. Elles payent maintenant d’avoir cédé au court terme, note Philippe Escande, éditorialiste économique au « Monde ».

In this short essay (…), I take issue with the relevance and effectiveness of ’corporate purpose’ as a form of private ordering (eg, as a bylaws provision), or in other sources of soft-law (self-regulation in corporate governance codes, declarations of business associations, etc). I challenge whether these are, in fact, effective tools to induce greater commitment toward stakeholders.

(…) My possible disagreement with Mayer and other similar approaches and initiatives—or, more precisely, with a possible reading of these approaches and initiatives—lays in the excessive trust and emphasis that has been reserved to formulas concerning the purpose of the corporation and their possible consequences. Mayer argues that the corporate contract should include a reference to stakeholders and general social interests beyond value for shareholders, suggesting that this simple trick would have a meaningful impact on business conduct.

(…) The reasons are obvious.

First, these formulas are so broad, vague and ephemeral that they cannot possibly represent a compass for corporate action; they cannot provide meaningful guidance for virtually any specific corporate decision that implies a (legitimate) tradeoff between the interests of different stakeholders. Also, as precedents show, these formulas can be used even less to invoke the violation of directors’ duties and their liability. This conclusion is inevitable because the very essence of the agency relationship, the crucial function of a director or executive, is exactly mediating and balancing the different and often conflicting interests that converge on the corporation in an uncertain and evolving scenario. The idea of constraining the necessary discretion of directors within the boundaries of a simple purpose declaration is no better than the idea of writing in the contract with a painter that her work must be a masterpiece. Such an attempted shortcut to real value is self-evidently flawed.

Second, multiplying the goals and interests that directors must or can pursue, if it can have any effect at all, by definition increases their flexibility and discretion and makes it easier to justify, ex ante and ex post, very different choices. Without being cynical, from this perspective it is not surprising that these formulas are often welcomed, if not sponsored, by business associations and interest groups linked to managers, executives and entrenched shareholders.

Third, self-regulation and private ordering are often a way to avoid or delay the adoption of more stringent statutory or regulatory provisions. The former might be more or less effective, but they might also create an illusion of responsibility. The risk of putting too much trust into the beneficial consequences of these formulas is a disregard for more biting mandatory provisions, which may be necessary to avoid externalities and other market failures.

Petit panorama provenant de la Harvard Law School Forum on Corporate Governance des sujets sensibles auxquelles le Conseil d’administration doit être conscient !

Set out below are some key areas for companies and boards to consider as they seek to better understand and optimize the link between value and values, and as they assess how the current challenges present both risks and opportunities for the corporation’s pursuit of its purpose.

L’article s’intéresse aux problématiques suivantes :

Inégalités sociales et économiques ;

Parties prenantes ;

Covid-19 ;

Intelligence artificielle et nouvelles technologies ;

Si les marchés et les infrastructures ont bien fonctionné durant la crise sanitaire, les déséquilibres initialement présents se sont accentués et les tensions géopolitiques demeurent. Au-delà des nombreux défis que présente le financement de la relance économique post-Covid 19, une nouvelle vulnérabilité en soi, la cartographie met en avant une montée des risques pour la stabilité financière avec une possible nouvelle correction des marchés et la solvabilité dégradée de nombreuses entreprises.

Vous pouvez accéder au communiqué de presse ici, ainsi qu’au document complet juste ici.

À noter ici que l’information extrafinancière fait figure de risque !

Un besoin croissant de données extra-financières comparables et de qualité, non satisfait pour le moment et qui présente des risques pouvant obérer le développement pérenne de la finance durable […] La définition d’un reporting plus contraignant, faisant l’objet d’une harmonisation maximale, dans le cadre de la prochaine révision de la directive extra-financière, pourrait de ce point de vue également contribuer à des améliorations significatives.