Divulgation | Page 6

divulgation financière Gouvernance Normes d'encadrement

Résultat de la consultation du FRC sur la transparence financière en matière de changement climatique

Ivan Tchotourian 20 août 2016

Un groupe de travail du Financial Reporting Council (FRC) a publié fin avril 2016 un bilan de la 1e phase de son travail : « Phase 1 Report of the Task Force on Climate-Related Financial Disclosures (TCFD) ». Qu’en retenir ?

Objectifs

We support the objectives of the TCFD and welcome that it is focussing on financial risks and in particular those that could have a potential impact on future cash flows. We believe that this is important in identifying the boundary of information that would be relevant to investors’ decision-making. As with any project with multiple objectives there will be instances where a trade-off is necessary. Consistent principles are important, but absolute uniformity in disclosures detracts from careful consideration and communication of information that is relevant for its users. Whilst climate related risks will be important to many companies any recommendations must be proportionate and balanced, to avoid excessive focus on one set of risks to the detriment of disclosures of the other principal risks and uncertainties a company faces. Boards must retain responsibility for determining what disclosures, if any, on climate related risks are relevant and material. This requires an understanding of the potential impacts of climate change and legislative responses, and the application of judgement. Identification of factors to be considered by management when making such an assessment will be helpful.

Portée

The recommendation should provide preparers and their boards an understanding of the factors to consider when assessing, mitigating and, where necessary, reporting the climate change risks they might face. Factors to consider might include the sensitivity of its business model to climate related legislation (for example, the existence of low carbon substitute products or processes); the energy use and carbon emissions of the company, its products and suppliers; the company’s investment planning periods; and the geographical location of operations and its distribution channels. High risk sectors could then be used to illuminate those factors.

Utilisateurs

We note from the Phase 1 Report that the intended users for the information goes beyond those making direct investments in companies to those further back in the capital supply chain. We welcome this to ensure more informed capital allocation decisions. However the disclosure recommendations will need to take into consideration the needs of the intended audience and be dependent on the type of preparer as different considerations will apply for climate related risks arising from companies reporting on their own operational activities in their annual report and those investing in a portfolio of assets or advising on investment activities. We also encourage the TCFD to consider the placement of information outside the annual report when recommending disclosures that might go beyond the needs of the annual report’s intended audience. We encourage reporting of more detailed voluntary information for investors or other users outside the annual report so that it does not detract from the key messages.

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière Normes d'encadrement

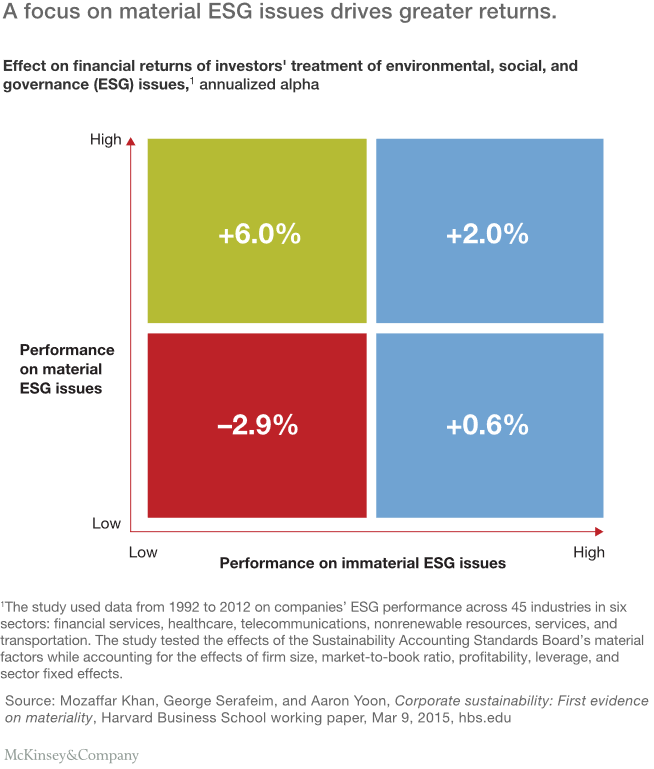

What institutional investors should do next on ESG : un beau rapport !

Ivan Tchotourian 26 juin 2016

C’est sous ce titre que le cabinet McKinsey (sous la plume de Jonathan Bailey, Bryce Klempner et Josh Zoffer) publie un excellent rapport en juin 2016 : « Sustaining sustainability: What institutional investors should do next on ESG ».

Mainstream institutions have made progress integrating environmental, social, and governance factors into their investing, but they still have far to go. Six ideas can take them to the next level.

Voici les 6 étapes énoncées :

- Require uniform corporate ESG-reporting standards based on the principle of materiality

- Build a shared ESG-rating system for external managers

- Work together to engage with corporations

- Stress-test portfolios for ESG risk factors

- Use a long-term ESG outlook to unlock new investment opportunities

- Confront the skepticism and misunderstanding that surround ESG head-on

À la prochaine…

Ivan Tchotourian

divulgation financière Gouvernance Normes d'encadrement

Gouvernance, qualité du « reporting » et performance boursière

Ivan Tchotourian 15 mars 2016

Par l’intermédiaire de son blogue (ici), Jacques Grisé propose une analyse intéressante de M. Félix Zogning sur les liens entre gouvernance, qualité de reporting et performance des entreprises.

Son article, paru sur le site de l’Ordre des administrateurs agréés du Québec (OAAQ) en janvier 2016, fait une excellente analyse de l’efficacité des pratiques de gouvernance eu égard à l’amélioration de la divulgation des informations et à la performance boursière de l’entreprise.

Accéder à cet article : « Gouvernance, qualité du « reporting » et performance boursière ».

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière mission et composition du conseil d'administration Normes d'encadrement normes de droit

Divulgation extra-financière en Angleterre : quel bilan ?

Ivan Tchotourian 3 février 2016

Le Climate Disclosure Standards Board a publié un bilan de la divulgation extra-financière des entreprises dans les domaines environnemental et des gaz à effet de serre du FTSE500 (ici), suite à la réforme introduite au Company Act 2006 en 2013 (Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013).

Voici quelques chiffres extraits de ce bilan :

Principal risks : 41% of companies consider environmental risks in their analysis of the principal risks to their company.

KPIs : 27% of companies make use of environmental KPIs. Of those that do, the majority use one of four main categories of KPIs based on: GHG emissions, energy, water or waste management (Figure 1).

Future development : 42% of companies identify environmental matters when considering the future development, performance or position of their company.

Environmental policies : 87% of companies disclosed environmental policies, 78% disclosed their policies and provided an indication of the effectiveness of those policies.

Environmental impacts : 90% of companies disclosed information regarding the environmental impacts of their business operations (Figure 2). Of the 10% that did not, 70% provided an explanation as to why that information was omitted.

GHG emissions : The Regulations require the disclosure of total annual GHG emissions (CO2e) for which a company is responsible. 90% of companies disclosed their total annual GHG emissions. 77% of companies disclosed the breakdown of both Scope 1 and 2 GHG emissions. 41% of companies disclosed omitted emission sources and explained the reasons for omission. Of the companies who explained omissions, the majority (44%) cited materiality as the main reason for omission (Figure 3). The sources of GHG emissions omitted by companies varied widely. Figure 4 shows the range of general categories of information omitted.

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière Normes d'encadrement

Information extra-financière : les conseils des CPA

Ivan Tchotourian 1 octobre 2015

Bonsoir à toutes et à tous, Une nouvelle publication des Comptables professionnels agréés du Canada (CPA Canada) traite de l’évolution de l’information d’entreprise, en particulier en ce qui concerne les questions relatives au développement durable. Le guide de CPA Canada intitulé « L’évolution de l’information d’entreprise : Exposé sur l’information sur le développement durable, l’information intégrée et l’information sur les questions environnementales, sociales et de gouvernance » aide les sociétés ouvertes à comprendre les trois ensembles de lignes directrices concernant l’information d’entreprise volontaire élaborés par :

- la Global Reporting Initiative (GRI);

- l’International Integrated Reporting Council (IIRC);

- le Sustainability Accounting Standards Board (SASB).

La communication de l’information d’entreprise sur le développement durable est envisagée de différentes manières dans les trois ensembles de lignes directrices présentés. Rappelons que cette information, de même que l’information intégrée, est essentiellement volontaire au Canada, et va au-delà de ce qu’exigent les autorités de réglementation en valeurs mobilières en matière sociale et environnementale.

À la prochaine…

Ivan Tchotourian