engagement et activisme actionnarial Gouvernance Structures juridiques

Actions à droit de vote multiple : est-ce payant ?

Ivan Tchotourian 24 août 2017

M. Gérard Bérubé revient sur la thématique des actions à droit de vote multiple dans une chronique publiée récemment et intitulée : « La présence de multivotes ne paie pas » (Le Devoir, 24 juin 2017).

La présence d’actions à vote multiple n’ajoute rien à la performance boursière à long terme de l’entreprise, ni ne la plombe. Leur contribution est davantage qualitative.

Le Mouvement d’éducation et de défense des actionnaires a relevé une étude réalisée par le Council of Institutionnal Investors avec l’aide d’un professeur de l’Université de Miami. Cette organisation américaine vouée à la bonne gouvernance des entreprises a analysé les données de 1762 entreprises américaines inscrites en Bourse composant l’Indice Russell 3000 pour déterminer s’il y avait corrélation entre la présence d’actions à vote multiple et la performance à long terme de l’entreprise sous forme de rendement sur le capital investi

(…) Sur le plan qualitatif toutefois, ces actions sont effectivement reconnues pour apporter une vision à plus long terme, pour éloigner les prises de contrôle hostiles et autres tentatives d’investisseurs prédateurs ; pour décourager les assauts spéculatifs d’actionnaires activistes n’ayant pour objectif que la valorisation à court terme de l’actionnaire, sans autre préoccupation pour les autres parties prenantes ; et pour pérenniser la contribution du fondateur ou d’un membre de sa famille dont la compétence serait, faut-il le présumer, reconnue pour assurer la relève.

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance normes de marché rémunération

Shareholders flex their muscles in 2017 AGM season to reduce FTSE pay

Ivan Tchotourian 24 août 2017

Bonjour à toutes et à tous, une récente étude menée sur les entreprises des indices FTSE100 et FTSE250 démontrent que ces dernières subissent de plus en plus la pression pour réduire le montant de la rémunération des hauts-dirigeants : « Shareholders flex their muscles in 2017 AGM season to reduce FTSE pay » (The Investment Association, 16 août 2017).

FTSE100 companies have listened and acted on 2016 investor rebellions, with a 35% decrease in 2017 remuneration resolutions that received over 20% dissent

FTSE250 companies were in the investor spotlight in 2017, with a 100% increase in companies getting 20% or more of votes against their remuneration resolutions compared to 2016

FTSE350 companies overall saw a 300% increase in votes against a Director re-election

6 FTSE350 companies withdrew resolutions on pay ahead of the company AGMs to avoid a shareholder rebellion

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance normes de droit

Directive sur les droits des actionnaires : cela avance

Ivan Tchotourian 22 mai 2017

La directive du Parlement européen et du Conseil modifiant la directive 2007/36/CE en vue de promouvoir l’engagement à long terme des actionnaires fait son chemin. Vous trouverez une synthèse ici écrite par Ed Winter :

On 3rd April 2017, the European Council adopted a revision to the Shareholders’ Right Directive (2007/36/EC) intended to encourage: « transparent and active engagement by shareholders of listed companies ». It affects the more than 8000 listed companies on EU regulated markets, their shareholders and advisers.

The revision reflects the Council’s concern that: (i) shortcomings in corporate governance arrangements for listed companies contributed to the financial crisis and (ii) the pursuit of short-term strategies by investment managers hampers effective shareholder engagement. To address these concerns, the Directives seeks to improve long-termism by shareholders (and their investment advisers), the exercise of shareholders’ rights and the flow of information relating to shareholdings. The Directive, therefore, touches on:

- oversight of directors’ remuneration;

- identification of shareholders;

- easier exercise of shareholders’ rights;

- greater transparency by institutional investors, asset managers and proxy advisors; and

- related party transactions.

Un dossier à suivre…

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance normes de droit rémunération

Rémunération des patrons : loin d’une fronde actionnariale !

Ivan Tchotourian 22 mai 2017

En ce printemps 2017, y a-t-il vraiment une fronde actionnariale contre la rémunération des « patrons » ? Mme Bénédicte Hautefort (éditrice de l’Hebdo des AG) apporte un éclairage intéressant dans le cadre de cet article de L’Hebdo des AG : « Enquête : Les actionnaires contestent-ils la rémunération des dirigeants en 2017 ? »

Les chiffres démontrent, à l’inverse, un soutien fidèle venant d’actionnaires souhaitant plutôt que rien en change ; il y a bien un mouvement de fond vers une baisse des rémunérations (en 2018), mais à l’initiative des entreprises, prenant en compte l’équité sociale, pas sous la pression de leurs actionnaires.

Voici un résumé de cette étude sur LinkedIn (ici) :

Trois faits. D’abord, les scores de vote démontent toute « fake news » de fronde actionnariale. Les scores d’approbation des rémunérations (« Say-on-Pay ») sont exactement les mêmes que les années précédentes, à 87% en moyenne. En d’autres termes, les actionnaires approuvent, très largement, les rémunérations proposées par les entreprises.

Ensuite, les chiffres démontrent un raisonnement mécanique des investisseurs dès qu’il s’agit de rémunération : il n’y a pas, aujourd’hui, de réflexion de fond de leur part. Ils sont très influencés par les proxy, même s’ils s’en défendent. Les chiffres le démontrent : les scores les plus bas sont ceux des sociétés qui n’ont pas « coché les cases » demandée par les proxy. Ceux-ci ont chaque fois sanctionné, par exemple, les rémunérations dont les variables leurs semblaient subjectifs, quelles que soient leur valeur absolue et même si la société (et le dividende) surperforme largement le secteur. Ils ont largement approuvé, à l’inverse, des rémunérations variables dont le schéma octroi 100% du bonus au dirigeant qui fait seulement la moyenne de la performance de son peer-group – est-ce vraiment un variable? Il semble que les proxy, au nom de la transparence, aient sacrifié l’émulation, et que les investisseurs approuvent.

Enfin, les votes sur le principe des rémunérations à venir montrent que les investisseurs ne veulent rien changer à ce fonctionnement, pourtant qualifié par beaucoup d’entre eux de superficiel. Cette année, première du vote dit « ex ante », était l’occasion pour les investisseurs d’initier un dialogue de fond sur les principes. Les investisseurs se disaient demandeurs, critiquant souvent publiquement les entreprises pour leur manque de débat sur le fond. Mais pour cette première application de la loi Sapin II, les entreprises, en fait de principes de rémunération, exposent pour la plupart la même mécanique de critères de variables que les années précédentes, sans prise de position sur le lien avec la stratégie, et les investisseurs approuvent très largement. Tout se passe comme s’ils voulaient, au fond, que rien ne change

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance mission et composition du conseil d'administration Nouvelles diverses

Can Staggered Boards Improve Value? Evidence from the Massachusetts Natural Experiment

Ivan Tchotourian 5 avril 2017

We study the effect of staggered boards on long-run firm value, using a natural experiment: a 1990 law that imposed a staggered board on all firms incorporated in Massachusetts.

We find a significant and positive average increase in Tobin’s Q among the Massachusetts treated firms, suggesting that staggered boards can be beneficial for early-life-cycle firms, which exhibit greater information asymmetries between insiders and investors. These results are validated using a larger sample of firms from the Investor Responsibility Research Center.

In exploring possible channels for these effects, we find that the effects are stronger among innovating Massachusetts firms, particularly those facing greater Wall Street scrutiny. The evidence is consistent with staggered boards improving managers’ incentives to make long-term investments.

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance mission et composition du conseil d'administration

Retour sur « le » cas canadien d’activisme : CP Rail

Ivan Tchotourian 31 mars 2017

Yvan Allaire et François Dauphin reviennent sur l’intervention agressive d’activistes chez CP Rail dans un papier publié par l’IGOPP : « Pershing Square, Ackman and CP Rail: A Case of Successful ‘Activism’? » (28 novembre 2016). Si terribles ces activistes ?

Pershing Square Capital Management, an activist hedge fund owned and managed by William Ackman, began hostile maneuvers against the board of CP Rail in September 2011 and ended its association with CP in August 2016, having netted a profit of $2.6 billion for his fund. This Canadian saga, in many ways, an archetype of what hedge fund activism is all about, illustrates the dynamics of these campaigns and the reasons why this particular intervention turned out to be a spectacular success… thus far.

(…) In this day and age, the CP case teaches us that no matter its size or the nature of its business, a company is always at risk of being challenged by dissident shareholders, and most particularly by those funds which make a business of these sorts of operations, the activist hedge funds. Of course, a number of critical features of this saga can be singled out to explain the particular success of this intervention, but this is not the focal point of this post. After all, a widely held company with weak financial results and a stagnating stock price will inevitably attract the attention of these funds

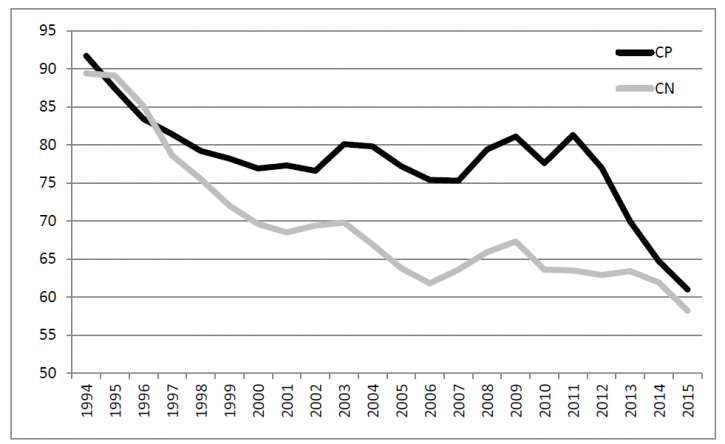

But the puzzling question and it is an unresolved dilemma of corporate governance remains: how come the board did not know earlier what became apparent very quickly after the Ackman/Harrison takeover? Why would the board not call on independent experts to assess management’s claim that structural differences made it impossible for CP to achieve a performance similar to that of other railroads? The gap in operating ratio between CP and CN had not always been as wide. In fact, as shown in Figure 1, CP had a lower operating ratio than CN during a period of time in the 1990s (Of course, CN was a Crown corporation at that time). The gap eventually widened, reaching unprecedented levels during Fred Green’s tenure (…)

How could the board have known that performances far superior to those targeted by the CEO could be swiftly achieved?

Lurking behind these questions is the fundamental flaw of corporate governance: the asymmetry of information, of knowledge and time invested between the governors and the governed, between the board of directors and management. In CP’s case, the directors, as per the norms of “good” fiduciary governance, relied on the information provided by management, believed the plans submitted by management to be adequate and challenging, and based the executives’ lavish compensation on the achievement of these plans. The Chairman, on behalf of the Board, did “extend our appreciation to Fred Green and his management team for aggressively and successfully implementing our Multi-Year plan and creating superior value for our shareholders and customers.” That form of governance is being challenged by activist investors of all stripes.

Their claim, a demonstrable one in the case of CP, is that with the massive amount of information now accessible about a publicly listed company and its competitors, it is possible for dedicated shareholders to spot poor strategies and call for drastic changes. If push comes to shove, these funds will make their case directly to other shareholders via a proxy contest for board membership.

Corporate boards of the future will have to act as “activists” in their quest for information and their ability to question strategies and performances.

À la prochaine…

Ivan Tchotourian

engagement et activisme actionnarial Gouvernance mission et composition du conseil d'administration Nouvelles diverses rémunération

Shareholders ready to show their hand over executive pay

Ivan Tchotourian 31 mars 2017

Alors rébellion ou pas des actionnaires ? Alors que les documents des entreprises commencent à être rendus publics (pour des raisons de sollicitation de procuration), les chiffres de la rémunération des hauts-dirigeants le sont tout autant ! Faut-il croire aux propos optimistes des journalistes du Financial Times (« Shareholders ready to show their hand over executive pay« ) ?

It will not be a quiet season. Investors have already won several small victories, forcing some UK companies to backtrack on pay decisions. Now they have the scent of blood.

This month global companies including BP and some of the biggest UK banks will divulge how much they awarded top executives last year, setting the scene for potentially fractious showdowns with investors.

Last year, a majority of investors rejected plans at seven of the biggest US companies and three of the UK’s largest groups. This year is expected to be an even bigger rebellion.

(…) A new mood on executive awards has already swept through Europe. Last year investor support for pay proposed by German companies dropped from 90 per cent to 76 per cent for large companies.

Opposition has also increased in the Netherlands, Switzerland and France “because executive pay is seen to have become excessive,” says Georgina Marshall, head of research at voting adviser, ISS. The outlier is the US where more than three-quarters of proposals won 90-plus per cent support last year. However, even there criticism of excessive rewards is mounting.The mood in the UK has become particularly tense, however. There were as many shareholder revolts against UK pay plans last year as there were during 2012’s so-called “shareholder spring”, according to Manifest data.

À la prochaine…

Ivan Tchotourian