autres publications Gouvernance Normes d'encadrement normes de droit normes de marché

Governance goes green : à lire !

Ivan Tchotourian 6 juillet 2016

Beau rapport du cabinet Weil, Gotshal & Manges LLP qui montre que la RSE ne peut plus être ignoré par les entreprises : « Governance Goes Green ».

It’s not just us tree-huggers. Increasingly, institutional investors, pension plans and regulators are calling for (and in some cases requiring) companies to assess and report on the sustainability of their business operations and investments. Climate change and other environmental concerns are at the forefront of these calls. Institutional investors are focusing on sustainable business practices – a broad category in which environmental and social risks, costs and opportunities of doing business are analyzed alongside conventional economic considerations – as a key factor in long-term financial performance. Sustainability proponents are looking to boards of directors and management to integrate these considerations into their companies’ long-term business strategies.

Éléments essentiels à retenir :

- Institutional investors increasingly regard environmental and other sustainability issues as strategic matters for companies.

- Shareholders continue to submit environmental and other sustainability proposals, successfully garnering attention and prompting companies to make changes, despite their failure to win majority votes.

- Independent organizations are developing standards for sustainability and environmental reporting to provide investors with consistent metrics for assessing and comparing the sustainability of companies’ practices.

- Sustainability and environmental reporting remains in the SEC’s sights as it evaluates the effectiveness of current disclosure requirements and considers changes for the future.

À la prochaine…

Ivan Tchotourian

autres publications divulgation financière Normes d'encadrement

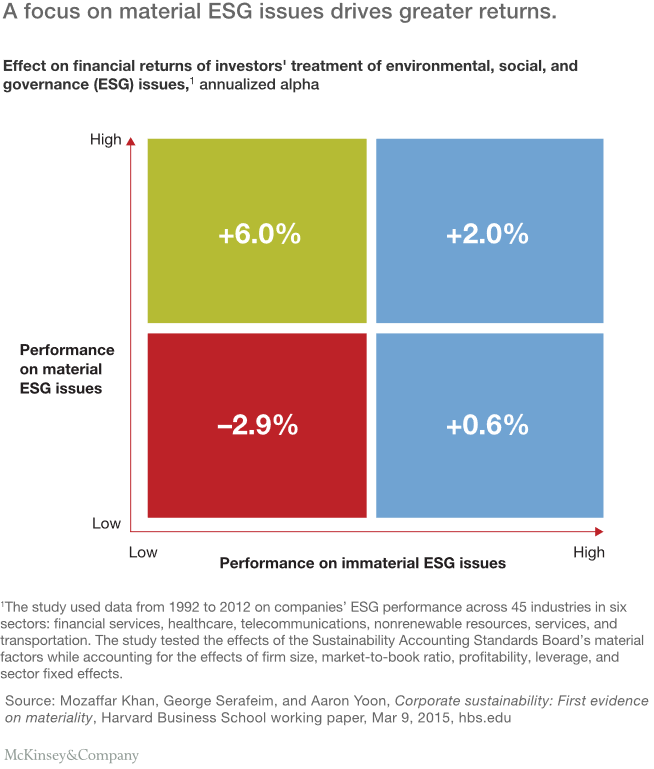

What institutional investors should do next on ESG : un beau rapport !

Ivan Tchotourian 26 juin 2016

C’est sous ce titre que le cabinet McKinsey (sous la plume de Jonathan Bailey, Bryce Klempner et Josh Zoffer) publie un excellent rapport en juin 2016 : « Sustaining sustainability: What institutional investors should do next on ESG ».

Mainstream institutions have made progress integrating environmental, social, and governance factors into their investing, but they still have far to go. Six ideas can take them to the next level.

Voici les 6 étapes énoncées :

- Require uniform corporate ESG-reporting standards based on the principle of materiality

- Build a shared ESG-rating system for external managers

- Work together to engage with corporations

- Stress-test portfolios for ESG risk factors

- Use a long-term ESG outlook to unlock new investment opportunities

- Confront the skepticism and misunderstanding that surround ESG head-on

À la prochaine…

Ivan Tchotourian

autres publications Gouvernance normes de droit normes de marché Structures juridiques Valeur actionnariale vs. sociétale

Pourquoi les entreprises deviendraient-elles des B Corp ?

Ivan Tchotourian 20 juin 2016

En voilà une question allez-vous me répondre et pourtant… Un récent article du Harvard Business Review de Suntae Kim, Matthew Karlesky, Christopher Myers et Todd Schifeling intitulé « Why Companies Are Becoming B Corporations » aborde la question de face.

2 raisons essentielles sont identifiées :

- First, as large established firms have ramped up their corporate social responsibility efforts, small businesses that have long been committed to social and environmental causes want to prove that they are more genuine, authentic advocates of stakeholder benefits.

- The qualitative evidence, gathered from firms’ B corporation application materials, revealed that certifying firms believed “the major crises of our time are a result of the way we conduct business,” and they became a B Corporation to “join the movement of creating a new economy with a new set of rules” and “redefine the way people perceive success in the business world.”

So why do certain firms (and not others) choose to identify as B Corporations? Individual leaders are partly why some organizations broaden their purpose beyond maximizing shareholder value. We might look to Sir Richard Branson, who in 2013 co-launched the “B Team,” publicly decrying corporations’ sole focus on short-term profits and calling for a reprioritization of people- and planet-focused performance. We might also consider leaders of firms like Ben & Jerry’s or Patagonia (both B Corporations) that have prioritized societal and environmental agendas.

Clearly, such leaders can be important catalysts of social change. However, the explosive growth of B Corporations seems also to be driven by broader trends and changes in the corporate landscape that cannot be explained by individuals’ actions alone.

Two of us (Suntae Kim and Todd Schifeling) conducted research to build a more robust understanding of the rise of B corporations. By qualitatively examining the internal motives of firms in the process of becoming a B corporation, and quantitatively testing key factors in these firms’ external industry environment – including the shareholder- and stakeholder-focused behaviors of their corporate competitors – we found that there are at least two major underlying reasons why firms choose to seek B Corporation certification.

À la prochaine…

Ivan Tchotourian

autres publications devoirs des administrateurs Gouvernance normes de droit Nouvelles diverses

Publication au Bulletin Joly Bourse : retour sur Theratechnologies

Ivan Tchotourian 7 juin 2016

Bonjour à toutes et à tous, je viens de publier au Bulletin Joly Bourse une analyse de la décision de la Cour suprême Theratechnologies inc. c. 121851 Canada inc. (2015 CSC 18). Sous le titre « Responsabilité civile sur le marché secondaire : premières précisions de la Cour suprême canadienne sur l’autorisation judiciaire préalable », je reviens sur les enseignements de cette importante décision d’avril 2015 en termes de protection des investisseurs par le biais des recours collectifs.

Rendue le 17 avril 2015, la décision de la Cour suprême canadienne Theratechnologies inc. c. 121851 Canada inc. apporte des précisions intéressantes sur le régime de responsabilité de nature civile relevant du droit des valeurs mobilières. Au travers de cet arrêt, la plus haute instance du pays se prononce pour la première fois sur les conditions d’autorisation de ce recours introduit en 2007.

À la prochaine…

Ivan Tchotourian

autres publications mission et composition du conseil d'administration normes de droit

Incertitudes sur les conséquences de la féminisation des CA

Ivan Tchotourian 31 mai 2016

ECGI publie un nouveau papier ECGI Finance Series 466/2016 consacré à la féminisation des CA intitulé : « Women on Boards: The Superheroes of Tomorrow? » (par Renée Adams).

Can female directors help save economies and the firms on whose boards they sit?

Policy makers seem to think so. Numerous countries have implemented boardroom gender policies because of business case arguments. While women may be the key to healthy economies, I argue that more research needs to be done to understand the benefits of board diversity. The literature faces three main challenges: data limitations, selection and causal inference. Recognizing and dealing with these challenges is important for developing informed research and policy. Negative stereotypes may be one reason women are underrepresented in management. It is not clear that promoting them on the basis of positive stereotypes does them, or society, a service.

À la prochaine…

Ivan Tchotourian

autres publications Normes d'encadrement objectifs de l'entreprise Valeur actionnariale vs. sociétale

La valeur actionnariale au rancart !

Ivan Tchotourian 31 mai 2016

Belle tribune de la professeure Lynn A Stout : « The Myth of Maximizing Shareholder Value » (OpenEdNew, 23 mai 2016).

By the end of the 20th century, a broad consensus had emerged in the Anglo-American business world that corporations should be governed according to the philosophy often called shareholder primacy. Shareholder primacy theory taught that corporations were owned by their shareholders; that directors and executives should do what the company’s owners/shareholders wanted them to do; and that what shareholders generally wanted managers to do was to maximize « shareholder value, » measured by share price. Today this consensus is crumbling. As just one example, in the past year no fewer than three prominent New York Times columnists have published articles questioning shareholder value thinking. Shareholder primacy theory is suffering a crisis of confidence. This is happening in large part because it is becoming clear that shareholder value thinking doesn’t seem to work, even for most shareholders.

Je vous laisse lire la suite…

Pour rappel, j’avais eu l’occasion de faire une recension du très bel ouvrage de Lynn A Stout dans la Revue international de droit économique – 2013/3 ((t. XXVII)) – : ici.

Lynn A. STOUT, The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations and the Public, Berrett-Koehler Publishers, 2012

1 – Un sujet d’une grande actualité

2 – Remise en cause de la norme de primauté actionnariale

3 – Les actionnaires d’aujourd’hui

4 – Mise en perspective de l’ouvrage

À la prochaine…

Ivan Tchotourian

autres publications normes de droit

Utilisation des médias sociaux : l’AMF accompagne les sociétés de gestion de portefeuille et les émetteurs de titres de créance structurés

Ivan Tchotourian 29 mai 2016

L’Autorité des marchés financiers (AMF) France a mené une consultation publique sur l’utilisation des médias sociaux par les sociétés de gestion de portefeuille, les émetteurs de titres de créance structurés et les distributeurs de produits financiers. Elle précise sa doctrine sur le sujet.

Les participants à la consultation ont soutenu l’initiative de l’AMF. Ils ont, par ailleurs, indiqué qu’il n’était pas souhaitable de créer un cadre réglementaire spécifique sur le sujet. L’AMF confirme que les règles encadrant la communication sur les médias dits « traditionnels » s’appliquent également à la communication sur les médias sociaux. Néanmoins, afin d’accompagner les sociétés de gestion (SGP), les émetteurs de titres de créance structurés (ETC) et les distributeurs dans l’utilisation de ces médias, en France, l’AMF précise les règles applicables et émet quelques recommandations de bonnes pratiques.

Les clarifications apportées à la doctrine de l’AMF visent à :

- Attirer l’attention des SGP, des ETC et des distributeurs de produits sur le fait que leur responsabilité ou celle de leurs salariés peut être engagée par les informations qu’ils publient sur les médias sociaux, mais aussi par les informations qu’ils relayent sans en être eux-mêmes les auteurs (par exemple un retweet sur Twitter) ;

- Rappeler que certaines pratiques commerciales peuvent être assimilées, en France, à des pratiques commerciales trompeuses et donc être sanctionnées ;

- Inciter les SGP et les ETC à se doter de règles d’organisation interne en matière de communication sur les médias sociaux (par exemple, en imposant une séparation entre les comptes utilisateurs personnels et professionnels) ;

- Recommander l’archivage des messages publiés sur ces médias afin de traiter d’éventuelles réclamations (par exemple, celles provenant de leurs clients).

À la prochaine…

Ivan Tchotourian