Bel article de Vanessa Serret et Mohamed Khemissi dans The conversation (27 juillet 2020) : « Rémunération des dirigeants : la transparence ne fait pas tout ». Cet article revient sur le ratio d’équité : non seulement son utilité, mais encore son niveau (20 ? 100 ?…)

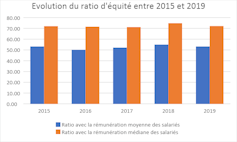

Le ratio d’équité apprécie l’écart entre la rémunération de chaque dirigeant et le salaire (moyen et médian) des salariés à temps plein de son entreprise. Il est prévu un suivi de l’évolution de ce ratio au cours des cinq derniers exercices et sa mise en perspective avec la performance financière de la société. Ces comparaisons renseignent sur la dynamique du partage de la création de valeur entre le dirigeant et les salariés.

(…)

Un premier état des lieux

Sur la base des rémunérations versées en 2019 par les entreprises composant l’indice boursier du CAC 40, les patrons français ont perçu un salaire moyen de 5 millions d’euros, soit une baisse de 9,1 % par rapport à 2018.

Évolution du ratio d’équité par rapport à la rémunération moyenne (bleu) et médiane (orange) des salariés de 2015 à 2019. auteurs

Ce chiffre représente 53 fois la rémunération moyenne de leurs employés (72 fois la rémunération médiane) : un ratio acceptable, selon l’agence de conseil en vote Proxinvest. En effet, selon cette agence, et afin de garantir la cohésion sociale au sein de l’entreprise, le ratio d’équité ne doit pas dépasser 100 (par rapport à la rémunération moyenne des salariés).

Deux dirigeants s’attribuent néanmoins des rémunérations qui dépassent le maximum socialement tolérable à savoir Bernard Charlès, vice-président du conseil d’administration et directeur général de Dassault Systèmes et Paul Hudson, directeur général de Sanofi avec un ratio d’équité qui s’établit respectivement de 268 et de 107.

Notons également que pour les deux sociétés publiques appartenant à l’indice boursier du CAC 40, le ratio d’équité dépasse le plafond de 20 (35 pour Engie et 38 pour Orange) fixé par le décret n° 2012-915 du 26 juillet 2012, relatif au contrôle de l’État sur les rémunérations des dirigeants d’entreprises publiques.

Excellente lecture ce matin de ce billet du Harvard Law School Forum on Corporate Governance : « Legal Liability for ESG Disclosures » (de Connor Kuratek, Joseph A. Hall et Betty M. Huber, 3 août 2020). Dans cette publication, vous trouverez non seulement une belle synthèse des référentiels actuels, mais aussi une réflexion sur les conséquences attachées à la mauvaise divulgation d »information.

Extrait :

3. Legal Liability Considerations

Notwithstanding the SEC’s position that it will not—at this time—mandate additional climate or ESG disclosure, companies must still be mindful of the potential legal risks and litigation costs that may be associated with making these disclosures voluntarily. Although the federal securities laws generally do not require the disclosure of ESG data except in limited instances, potential liability may arise from making ESG-related disclosures that are materially misleading or false. In addition, the anti-fraud provisions of the federal securities laws apply not only to SEC filings, but also extend to less formal communications such as citizenship reports, press releases and websites. Lastly, in addition to potential liability stemming from federal securities laws, potential liability could arise from other statutes and regulations, such as federal and state consumer protection laws.

A. Federal Securities Laws

When they arise, claims relating to a company’s ESG disclosure are generally brought under Section 11 of the Securities Act of 1933, which covers material misstatements and omissions in securities offering documents, and under Section 10(b) of the Securities Exchange Act of 1934 and rule 10b-5, the principal anti-fraud provisions. To date, claims brought under these two provisions have been largely unsuccessful. Cases that have survived the motion to dismiss include statements relating to cybersecurity (which many commentators view as falling under the “S” or “G” of ESG), an oil company’s safety measures, mine safety and internal financial integrity controls found in the company’s sustainability report, website, SEC filings and/or investor presentations.

Interestingly, courts have also found in favor of plaintiffs alleging rule 10b-5 violations for statements made in a company’s code of conduct. Complaints, many of which have been brought in the United States District Court for the Southern District of New York, have included allegations that a company’s code of conduct falsely represented company standards or that public comments made by the company about the code misleadingly publicized the quality of ethical controls. In some circumstances, courts found that statements about or within such codes were more than merely aspirational and did not constitute inactionable puffery, including when viewed in context rather than in isolation. In late March 2020, for example, a company settled a securities class action for $240 million alleging that statements in its code of conduct and code of ethics were false or misleading. The facts of this case were unusual, but it is likely that securities plaintiffs will seek to leverage rulings from the court in that class action to pursue other cases involving code of conducts or ethics. It remains to be seen whether any of these code of conduct case holdings may in the future be extended to apply to cases alleging 10b-5 violations for statements made in a company’s ESG reports.

B. State Consumer Protection Laws

Claims under U.S. state consumer protection laws have been of limited success. Nevertheless, many cases have been appealed which has resulted in additional litigation costs in circumstances where these costs were already significant even when not appealed. Recent claims that were appealed, even if ultimately failed, and which survived the motion to dismiss stage, include claims brought under California’s consumer protection laws alleging that human right commitments on a company website imposed on such company a duty to disclose on its labels that it or its supply chain could be employing child and/or forced labor. Cases have also been dismissed for lack of causal connection between alleged violation and economic injury including a claim under California, Florida and Texas consumer protection statutes alleging that the operator of several theme parks failed to disclose material facts about its treatment of orcas. The case was appealed to the U.S. Court of Appeals for the Ninth Circuit, but was dismissed for failure to show a causal connection between the alleged violation and the plaintiffs’ economic injury.

Overall, successful litigation relating to ESG disclosures is still very much a rare occurrence. However, this does not mean that companies are therefore insulated from litigation risk. Although perhaps not ultimately successful, merely having a claim initiated against a company can have serious reputational damage and may cause a company to incur significant litigation and public relations costs. The next section outlines three key takeaways and related best practices aimed to reduce such risks.

C. Practical Recommendations

Although the above makes clear that ESG litigation to date is often unsuccessful, companies should still be wary of the significant impacts of such litigation. The following outlines some key takeaways and best practices for companies seeking to continue ESG disclosure while simultaneously limiting litigation risk.

Key Takeaway 1: Disclaimers are Critical

As more and more companies publish reports on ESG performance, like disclaimers on forward-looking statements in SEC filings, companies are beginning to include disclaimers in their ESG reports, which disclaimers may or may not provide protection against potential litigation risks. In many cases, the language found in ESG reports will mirror language in SEC filings, though some companies have begun to tailor them specifically to the content of their ESG reports.

From our limited survey of companies across four industries that receive significant pressure to publish such reports—Banking, Chemicals, Oil & Gas and Utilities & Power—the following preliminary conclusions were drawn:

All companies surveyed across all sectors have some type of “forward-looking statement” disclaimer in their SEC filings; however, these were generic disclaimers that were not tailored to ESG-specific facts and topics or relating to items discussed in their ESG reports.

Most companies had some sort of disclaimer in their Sustainability Report, although some were lacking one altogether. Very few companies had disclaimers that were tailored to the specific facts and topics discussed in their ESG reports:

In the Oil & Gas industry, one company surveyed had a tailored ESG disclaimer in its ESG Report; all others had either the same disclaimer as in SEC filings or a shortened version that was generally very broad.

In the Banking industry, two companies lacked disclaimers altogether, but the rest had either their SEC disclaimer or a shortened version.

In the Utilities & Power industry, one company had no disclaimer, but the rest had general disclaimers.

In the Chemicals industry, three companies had no disclaimer in their reports, but the rest had shortened general disclaimers.

There seems to be a disconnect between the disclaimers being used in SEC filings and those found in ESG In particular, ESG disclaimers are generally shorter and will often reference more detailed disclaimers found in SEC filings.

Best Practices: When drafting ESG disclaimers, companies should:

Draft ESG disclaimers carefully. ESG disclaimers should be drafted in a way that explicitly covers ESG data so as to reduce the risk of litigation.

State that ESG data is non-GAAP. ESG data is usually non-GAAP and non-audited; this should be made clear in any ESG Disclaimer.

Have consistent disclaimers. Although disclaimers in SEC filings appear to be more detailed, disclaimers across all company documents that reference ESG data should specifically address these issues. As more companies start incorporating ESG into their proxies and other SEC filings, it is important that all language follows through.

Key Takeaway 2: ESG Reporting Can Pose Risks to a Company

This article highlighted the clear risks associated with inattentive ESG disclosure: potential litigation; bad publicity; and significant costs, among other things.

Best Practices: Companies should ensure statements in ESG reports are supported by fact or data and should limit overly aspirational statements. Representations made in ESG Reports may become actionable, so companies should disclose only what is accurate and relevant to the company.

Striking the right balance may be difficult; many companies will under-disclose, while others may over-disclose. Companies should therefore only disclose what is accurate and relevant to the company. The US Chamber of Commerce, in their ESG Reporting Best Practices, suggests things in a similar vein: do not include ESG metrics into SEC filings; only disclose what is useful to the intended audience and ensure that ESG reports are subject to a “rigorous internal review process to ensure accuracy and completeness.”

Key Takeaway 3: ESG Reporting Can Also be Beneficial for Companies

The threat of potential litigation should not dissuade companies from disclosing sustainability frameworks and metrics. Not only are companies facing investor pressure to disclose ESG metrics, but such disclosure may also incentivize companies to improve internal risk management policies, internal and external decisional-making capabilities and may increase legal and protection when there is a duty to disclose. Moreover, as ESG investing becomes increasingly popular, it is important for companies to be aware that robust ESG reporting, which in turn may lead to stronger ESG ratings, can be useful in attracting potential investors.

Best Practices: Companies should try to understand key ESG rating and reporting methodologies and how they match their company profile.

The growing interest in ESG metrics has meant that the number of ESG raters has grown exponentially, making it difficult for many companies to understand how each “rater” calculates a company’s ESG score. Resources such as the Better Alignment Project run by the Corporate Reporting Dialogue, strive to better align corporate reporting requirements and can give companies an idea of how frameworks such as CDP, CDSB, GRI and SASB overlap. By understanding the current ESG market raters and methodologies, companies will be able to better align their ESG disclosures with them. The U.S. Chamber of Commerce report noted above also suggests that companies should “engage with their peers and investors to shape ESG disclosure frameworks and standards that are fit for their purpose.”

Voilà une belle question abordée dans ce billet du Harvard Law School Forum on Corporate Governance« What Board Members Need to Know about the “E” in ESG » (par Sheila M. Harvey, Reza S. Zarghamee et Jonathan M. Ocker, 9 juillet 2020) !

Extrait concernant les CA :

Board Responsibilities

Traditionally, a company’s board will manage corporate governance risks and executive compensation. The practical need to expand these responsibilities to account for environmental stewardship and risk management is a relatively new phenomenon, and many boards are not yet up to speed.

The first step toward properly addressing environmental matters is for the board to collaborate with management to identify the different ways in which the company’s businesses and operations interface with environmental issues. The aim here is to think expansively. For purposes of ESG, environmental matters extend beyond regulatory compliance and impacts on natural resources to include concepts such as environmental justice, carbon footprints, supply chains and product stewardship.

Consistent with this approach, an equally broad realm of potential environmental risks also should be considered. These may include the potential to cause environmental contamination and natural resource damages, which may trigger not just cleanup liabilities but also disclosure requirements in financial statements. Also relevant is the potential for business operations to be disrupted by environmental factors such as climate change.

Once potential environmental risks are identified, assessments should be made regarding their materiality and the existence of standing corporate policies and procedures to address them. Where such policies are lacking, they should be developed and implemented. Moreover, determinations should be made about how the company will present itself to investors, regulators and society to adequately inform them of potential environmental risks, avoid reputational harm and increase long-term value.

There is no one-size-fits-all solution, and companies have different environmental profiles. Each will have to find its own way, but the board should make sure that management devotes the appropriate resources to addressing environmental matters, understands environmental disclosure requirements and standards and ranking systems, and takes a proactive approach to protecting the company’s reputation from an environmental standpoint.

This is a multifaceted paradigm that requires open lines of communication between management and the board at all times. Moreover, because not every board member can be an ESG expert, we recommend that the appropriate committee be tasked in its charter with spearheading the environmental risk area for the board.

Points à retenir :

Corporate boards should partner with management to ensure appropriate and regular oversight of environmental issues critical to the long-term economic success and reputation of the company.

Either the board or an authorized committee should receive briefings on environmental matters/risks that may jeopardize a company’s reputation and corrective action undertaken to address those risks.

Management should monitor environmental disclosures and rankings of peer firms and consult with the board on how to improve their company’s standing relative to competing firms and in terms of stakeholder expectations.

David Larcker, Bradford Lynch, Brian Tayan et Daniel Taylor publient un texte qui revient sur la transparence des ghrandes entreprises américaines en matière de COVID-19 « The Spread of Covid-19 Disclosure » (29 juin 2020). Un document plein de statistiques et de tendances sur la transparence… vraiment intéressant sachant que l’enjeu de la question n’est pas à négliger.

Extrait :

The COVID-19 pandemic presents an interesting scenario whereby an unexpected shock to the economic system led to a rapid deterioration in the economic landscape, causing sharp changes in performance relative to expectations just a few months prior. For most companies, the pandemic has been detrimental. For a few, it brought unexpected demand. In many cases, supply chains have been strained, causing ripple effects that extend well beyond any one company.

How do companies respond to such a situation? What choices do they make, and how much transparency do they offer? How does disclosure vary in a setting where the potential impact is so widely uncertain? The COVID-19 pandemic provides a unique setting to examine disclosure choices in a situation of extreme uncertainty that extends across all companies in the public market. This devastating outlier event provides a rare glimpse into disclosure behavior by managers and boards.

Why This Matters

The COVID-19 pandemic provides a unique opportunity to examine disclosure practices of companies relative to peers in real time about a somewhat unprecedented shock that impacted practically every publicly listed company in the U.S. We see that decisions varied considerably about whether to make disclosure and, if so, what and how much to say about the pandemic’s impact on operations, finances, and future. What motivates some companies to be forthcoming about what they are experiencing, while others remain silent? Does this reflect different degrees of certitude about how the virus would impact their businesses, or differences in managements’ perception of their “obligations” to be transparent with the public? What does this say about a company’s view of its relation and duty to shareholders?

In one example, we saw a consumer beverage company make zero references to COVID-19 in its SEC filings and website, despite the virus plausibly having at least some impact on its business. In another example, we saw a company claim no material changes to its previously reported risk factors when managers almost certainly had relevant information about the virus and the likely impact on sales and operations. What discussion among the senior managers, board members, external auditor, and general counsel leads to a decision to make no disclosures? What should shareholders glean from this decision, particularly in light of peer disclosure?

The COVID-19 pandemic represents a so-called “black swan” event that inflicted severe and unexpected damage to wide swaths of the economy. What strategic insights will companies learn from this event? Can boards use these insights to prepare for other possible outlier events, such as climate events, terrorism, cyber-attacks, pandemics, and other emergencies? Should these insights be disclosed to shareholders?

Random and arbitrary compliance with various initiatives makes companies’ sustainable practices ‘less’ rather than ‘more’ transparent. Our paper offers a comprehensive view on different reporting frameworks. It shows that there is a need to provide some clarity in this complex landscape. Fundamentally, the current reporting landscape is unlikely to impact positively on efforts towards sustainability. We suggest in our paper hat the scope of the NFRD, as the most promising of the existing initiatives, should be revisited so as to enhance its contribution to furthering corporations’ sustainable practices. Our paper supports reform of the NFRD which has constituted a positive step in the right direction. What is required now is stronger guidance on what to report and how to report it. Steps are being taken in the right direction towards clarifying metrics around sustainability (World Economic Forum 2020). A standardized and streamlined framework is necessary in order to pin companies down to something more concrete, rather than giving them too much choice on which guidelines, frameworks or recommendations they may opt to follow. Stronger, clearer and more concrete definitions of key concepts are required, as well as clarification of the rights of stakeholders in this area of activity. Proposals for reform that have arisen, with a consultation exercise by the European Commission, (European Commission Consultation 2020) are therefore to be welcomed. We suggest an expansion of the NFRD’s scope and that it represent sustainability as a positive instead of reducing the focus only to negative risks. EU member states and companies should have opportunities for effective compliance with the reporting requirements, with the NFRD better defining the concepts it refers to.

In particular, securities regulators should make pay ratio disclosures mandatory to improve transparency of executive pay packages at public companies. Pay ratio disclosures reveal the difference in the total remuneration between a company’s top executives and its rank and file workers….

The impact of the losses on shareholders will be significant. Investors, however, are being forced to rely on news reports to try to understand how the crisis is impacting companies in their portfolios and how those companies are responding. The SEC must act to require companies to provide consistent, reliable data to investors about the economic impact of the pandemic on their business, human capital management practices, and supply chain risks. These disclosures should include:

Workplace COVID-19 Prevention and Control Plan—Companies should disclose a written infectious disease prevention and control plan including information such as the company’s practices regarding hazard identification and assessment, employee training, and provision of personal protective equipment.

Identification, Contact Tracing, and Isolation—Companies should disclose their policies for identifying employees who are infected or symptomatic, contact tracing and notification for potentially exposed employees and customers, and leave policies for infected employees who are isolating.

Compliance with Quarantine Orders and phased reopening orders—Companies should disclose how they are complying with federal, state, and local government quarantine orders and public health recommendations to limit operations.

Financial Implications—Companies should disclose the impact of the COVID-19 pandemic on their cash flows and balance sheet as well as steps taken to preserve liquidity such as accessing credit facilities, government assistance, or the suspension of dividends and stock buybacks.

Executive Compensation—Companies should promptly disclose the rationale for any material modifications of senior executive compensation due to the COVID-19 pandemic, including changes to performance targets or issuance of new equity compensation awards.

Employee Leave—Companies should disclose whether or not they provide paid sick leave to encourage sick workers to stay home, paid leave for quarantined workers, paid leave at any temporarily closed facilities, and family leave options to provide for childcare or sick family

Health Insurance—Companies should disclose the health insurance coverage ratio of their workforce and whether the company has a policy to provide employer-paid health insurance for any employees who are laid off during the COVID-19 pandemic.

Contingent Workers—Companies should disclose if part-time employees, temporary workers, independent contractors, and subcontracted workers receive all the protections and benefits provided to full-time company employees, including those outlined above.

Supply Chains-Companies should disclose whether they are current on payments to their supply chain vendors. Timely and prompt payments to suppliers will help retain suppliers’ workforces and ensure that a stable supply chain is in place for business operations going forward.

Workers’ Rights-Companies should disclose their policies for protecting employees who raise concerns about workplace health and safety from retaliation, including whistleblower protections and contractual provisions protecting workers’ rights to raise concerns about workplace conditions.

Political activity—Companies should disclose all election spending and lobbying activity, especially money spent through third parties like trade associations and social welfare 501(c)4 organizations.

Prior to the onset of COVID-19, it was often argued that human rights, worker protection and supply chain matters were moral issues not relevant to a company’s financial performance. As millions of workers are laid off and supply chains unravel, the pandemic has proven that view wrong. Businesses that protect workers and consumers will be better positioned to continue operations and respond to consumer demand throughout the pandemic. The disclosures outlined above will provide investors with important information to help them understand how COVID-19 is impacting the companies they are invested in. In addition, by requiring these disclosures, the Commission has the opportunity to encourage companies to review their current practices and consider whether updates are necessary in light of recent events. The process of preparing these disclosures may help some public companies to recognize that their current practices are not sufficiently robust to protect their workers, consumers, supply chains and, as a result, their investors’ capital given the impact of the pandemic.