Bel article de Vanessa Serret et Mohamed Khemissi dans The conversation (27 juillet 2020) : « Rémunération des dirigeants : la transparence ne fait pas tout ». Cet article revient sur le ratio d’équité : non seulement son utilité, mais encore son niveau (20 ? 100 ?…)

Le ratio d’équité apprécie l’écart entre la rémunération de chaque dirigeant et le salaire (moyen et médian) des salariés à temps plein de son entreprise. Il est prévu un suivi de l’évolution de ce ratio au cours des cinq derniers exercices et sa mise en perspective avec la performance financière de la société. Ces comparaisons renseignent sur la dynamique du partage de la création de valeur entre le dirigeant et les salariés.

(…)

Un premier état des lieux

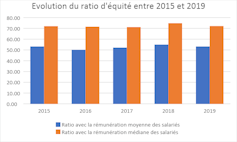

Sur la base des rémunérations versées en 2019 par les entreprises composant l’indice boursier du CAC 40, les patrons français ont perçu un salaire moyen de 5 millions d’euros, soit une baisse de 9,1 % par rapport à 2018.

Évolution du ratio d’équité par rapport à la rémunération moyenne (bleu) et médiane (orange) des salariés de 2015 à 2019. auteurs

Ce chiffre représente 53 fois la rémunération moyenne de leurs employés (72 fois la rémunération médiane) : un ratio acceptable, selon l’agence de conseil en vote Proxinvest. En effet, selon cette agence, et afin de garantir la cohésion sociale au sein de l’entreprise, le ratio d’équité ne doit pas dépasser 100 (par rapport à la rémunération moyenne des salariés).

Deux dirigeants s’attribuent néanmoins des rémunérations qui dépassent le maximum socialement tolérable à savoir Bernard Charlès, vice-président du conseil d’administration et directeur général de Dassault Systèmes et Paul Hudson, directeur général de Sanofi avec un ratio d’équité qui s’établit respectivement de 268 et de 107.

Notons également que pour les deux sociétés publiques appartenant à l’indice boursier du CAC 40, le ratio d’équité dépasse le plafond de 20 (35 pour Engie et 38 pour Orange) fixé par le décret n° 2012-915 du 26 juillet 2012, relatif au contrôle de l’État sur les rémunérations des dirigeants d’entreprises publiques.

Le 2 août 2020, Christiaan de Brauw a publié un intéressant billet sur l’Harvard Law School Forum on Corporate Governance sous le titre « The Dutch Stakeholder Experience ».

Extrait :

Lessons learned

The Dutch experience shows that the following lessons are key to make the stakeholder-oriented governance model work in practice.

Embed a clear stakeholder mission in the fiduciary duties of the board

To have a real stakeholder model, the board must have a duty to act in the interests of the business and all the stakeholders, not only the shareholders. In shareholder models there may be some room to consider stakeholder interests. For example, in Delaware and various other US states, the interests of stakeholders other than shareholders may be considered in the context of achieving overall long-term shareholder value creation. In US states with constituency statutes, the board’s discretion is preserved: the interests of stakeholders other than shareholders can be, but do not have to be, taken into account. A meaningful stakeholder model requires the board to act in the interests of the business and all stakeholders. This is a “shall” duty, in the words of Leo Strine and Robert Eccles (see Purpose With Meaning: A Practical Way Forward, Robert G. Eccles, Leo E. Strine and Timothy Youmans, May 16, 2020). Rather than allowing for the possibility that all stakeholders’ interests will be taken into account; it should create a real duty to do so. Since 1971, boards of Dutch companies have had such a “shall” duty to follow a stakeholder mission, similar to that of a benefit corporation in, for example, Delaware.

The stakeholder duty must be clear and realistic for boards in the economic environment in which they operate. To define the contours of such a mission in a clear and practical way is not easy, as the journey of the Dutch stakeholder model shows. Today, the Netherlands has a meaningful and realistically defined fiduciary duty for boards. The primary duty is to promote the sustainable success of the business, focused on long-term value creation, while taking into account the interests of all stakeholders and ESG and similar sustainability perspectives. These principles are broadly similar to the corporate purpose and mission proposed by Martin Lipton and others (see On the Purpose of the Corporation, Martin Lipton, William Savitt and Karessa L. Cain, posted May 27, 2020).

Critics of the stakeholder model sometimes point to the ambiguity and lack of clarity of such a pluralistic model. The developments of the Dutch stakeholder model since its inception show that a pluralistic model can work in practice. By now, Dutch boards’ overriding task is adequately clear and aligned with what is typically expected of a company’s executives: pursuing the strategic direction that will most likely result in long-term and sustainable business success. The Dutch stakeholder model also has a workable roadmap to deal with stakeholders’ interests, particularly if they diverge or cannot all be protected fully at the same time, which necessarily results in trade-offs between stakeholders. A realistic approach to governance acknowledges that a stakeholder model does not mean that boards can or should seek to maximize value for all the stakeholders equally and at the same time. It is simply unrealistic to simultaneously pay (and progressively increase) dividends, increase wages and improve contract terms, while also promoting the success of the business. The Dutch interpretation of the stakeholder model, as developed through practice over decades, boils down to the focus on the sustainable success of the business and long-term value creation. As said above, stakeholders are protected by the board’s duty to prevent disproportionate or unnecessary harm to any class of stakeholders. Boards should avoid or mitigate such harm, for example, by agreeing “non-financial covenants” in a takeover. This makes sense as a way to protect stakeholder interests in a realistic manner, much more so than merely requiring boards—without any further guidance—to create value for all the stakeholders.

A stakeholder-oriented model should also be modern and flexible enough to address and incorporate important developments. The Dutch model is especially well positioned to embrace ESG and similar sustainability perspectives. For example, the Dutch company DSM has successfully illustrated this, while being profitable and attractive for investors. There is growing appreciation that being a frontrunner in ESG is required for sustainable business success. In addition to the fact that ESG is required for continuity of the business model and can often give a company a competitive edge, stakeholders increasingly require it. Simply “doing the right thing”, as an independent corporate goal, is more and more seen as important by (new millennial) employees, customers, institutional investors and other stakeholders.

There is no standard test to determine whether a business has achieved sustainable success. There will be different ways to achieve and measure success for different companies, depending on the respective circumstances. Therefore, the test will always have to be bespoke, implemented by the board and explained to stakeholders.

The Dutch stakeholder model has proven to work quite well in times of crisis, such as today’s Covid-19 crisis, as it bolsters the board’s focus on the survival and continuity of the business. The board must first assess whether there is a realistic chance of survival and continuity of the business. If not, and if insolvency becomes imminent, the board’s duties transform to focus on creditors’ interests, such as preventing wrongful trading and the winding down or restarting of the business in line with applicable insolvency/restructuring proceedings. Driven by the economic reality and the need to survive, in times of crisis, boards typically have more freedom to do what it takes to survive: from pursuing liquidity enhancing measures, implementing reorganizations, suspending dividends to shareholders and payments to creditors and so on. The success of the business remains the overriding aim, and in some cases harm to one or more classes of stakeholders may need to be accepted. In addition, in a true stakeholder model, in times of crisis there may not be sympathy for corporate raiders or activists (so-called “corona profiteers” in the current case) who want to buy listed companies on the cheap. A just say not now defense in addition to the just say no defense will readily be available for boards who are occupied with dealing with the crisis and revaluating the best strategic direction. This idea that during the Covid-crisis protection against activists and hostile bidders may be needed seems to be understood as well by, for example, ISS and Glass Lewis, evidenced by their willingness to accept new poison pills for a one year duration (see, for example, ISS and Glass Lewis Guidances on Poison Pills during COVID-19 Pandemic, Paul J. Shim, James E. Langston, and Charles W. Allen, posted on April 26, 2020).

Teeth to protect the stakeholder mission and appropriate checks and balances

The Netherlands has adopted a model in which matters of strategy are the prerogative of the executive directors under supervision of the non-executive directors or, in the still widely used two-tier system, of the management board under supervision of the supervisory board. Similar to the discretion afforded to directors under Delaware’s business judgment rule, a Dutch board has a lot of freedom to choose the strategic direction of the company. In a dispute, the amount of care taken by the board in the decision-making process will be scrutinized by courts, but normally objectively reasonable decisions will be respected. In the Dutch model the board is the captain of the ship; it is best equipped to determine the course for the business and take difficult decisions on how to serve the interests of stakeholders. Generally, the board has no obligation to consult with, or get the approval of, the shareholders in advance of a decision.

At the same time, in recognition of the significant power that boards have in the Dutch stakeholder model, there should be checks and balances to ensure the board’s powers are exercised in a careful manner, without conflicts of interest and without entrenchment. Non-executive/supervisory directors will need to exercise critical and hands-on oversight, particularly when there are potential conflicts of interest. Further, shareholders and other stakeholders are entitled to hold boards to account: boards need to be able to explain their strategic decisions. Shareholders can use their shareholder rights to express their opinions and preferences. Shareholders can also pursue the dismissal of failing and entrenched boards. Boards need regular renewed shareholder mandates through reappointments. The courts are the ultimate guardian of the stakeholder model. The Dutch Enterprise Chamber at the Amsterdam Court of Appeals, which operates in a comparable manner to the Delaware Chancery Court, is an efficient and expert referee of last resort.

The stakeholder model should not convert to a shareholder model in takeover scenarios. The board should focus on whether a takeover is the best strategic option and take into account the consequences for all the stakeholders. In most cases, the best strategic direction for the business will create the highest valuation of the business. But, and this is a real difference with shareholder models, it should be acknowledged that the stand-alone (or other best strategic) option can be different from the strategic option favored by a majority of the shareholders and the option that creates the most shareholder value. This principle was confirmed by the Dutch Enterprise Chamber in 2017 in the AkzoNobel case.

A meaningful stakeholder model requires teeth. The right governance structures need to be put in place to create and protect the long-term stakeholder mission in the face of short-term market pressure. The reality—in the Netherlands as well as in the US—is that shareholders are the most powerful constituency in the stakeholder universe, with the authority to replace the board. In Dutch practice, various countervailing measures can be used to protect the stakeholder mission. A commonly used instrument is the independent protection foundation, the Dutch poison pill. The independent foundation can exercise a call option and acquire and vote on preference shares. It can neutralize the newly acquired voting power of hostile bidders or activists and is effective against actions geared at replacing the board, including a proxy fight. Once the threat no longer exists, the preference shares are cancelled. These measures have been effective, for example, against hostile approaches of America Movil for KPN (2013) and Teva for Mylan (2015).

Foster a stakeholder mindset, governance and environment

Perhaps the most important prerequisite for a well-functioning stakeholder model is the actual mindset of executives and directors. This mindset drives how they will use their stakeholder powers. Fiduciary duties—also in a stakeholder model—are “open norms” and leave a lot of freedom to boards to pursue the strategic direction and to use their authority as they deem fit. The prevailing spirit and opinions about governance are important, as they influence how powers are interpreted and exercised. As an example, the Dutch requirement that boards need to act in the interest of the company and its business dates from 1971, but that did not prevent boards in the 2000s from seeing shareholders as the first among equals. Today, the body of ideas about governance in the developed world is tending to converge towards stakeholder-oriented governance. This seems to indicate a fundamental change in mindset, not merely a fashionable trend or lip service. Board members with a stakeholder conviction should not be afraid to follow their mission, even if it runs counter to past experience or faces shareholder opposition. Of course, the future will hold the ultimate test for the stakeholder model. Can it, in practice, deliver on its promise to create sustainable success and long-term value and provide better protection for stakeholders? If so, this will create a positive feedback loop in which more boards embrace it.

Stakeholder-based governance models remain works in progress. In order to succeed in the long term, models that grant boards the authority to determine the strategy need to stay viable and attractive for shareholders. Going forward, boards following a stakeholder-based model will likely need to focus more on accountability, for example by concretely substantiating their strategic plans and goals and, where possible, providing the relevant metrics to measure their achievements. In reality, stakeholder models are already attractive for foreign investors: about 90% of investors in Dutch listed companies are US or UK investors. In addition, developments in the definition of the corporate purpose will further refine the stakeholder model. In the Netherlands, there has been a call to action by 25 corporate law professors who argue that companies should act as responsible corporate citizens and should articulate a clear corporate purpose.

To make stakeholder governance work, ideally, all stakeholders are committed to the same mission. It is encouraging that key institutional investors are embracing long-term value creation and the consideration of other stakeholders’ interests, for instance by supporting the New Paradigm model of corporate governance and stewardship codes to that effect. However, the “proof of the pudding” is whether boards can continue to walk the stakeholder talk and pursue the long-term view in the face of short-term pressure, either through generally accepted goals and behavior or, if necessary, countervailing governance arrangements. Today, it is still far from certain whether institutional investors will reject pursuing a short-term takeover premium, even where they consider the offer to be undervalued or not supportive of long-term value creation. Annual bonuses of the deciding fund manager may depend on accepting that offer. Until the behavior of investors in such scenarios respects the principle of long-term value creation, appropriate governance protection is important to prevent a legal pathway for shareholders to impose their short-term goals. Therefore, even in jurisdictions where stakeholder-based approaches have been embraced, and are actually pursued by boards, governance arrangements might need to be changed to make the stakeholder mission work in practice. Clear guidance for boards is needed on what the stakeholder mission is and how to deal with stakeholders’ interests, as well as catering for adequate powers and protection for boards.

The Dutch model, which requires a company to be business success-driven, have a “shall duty” to stakeholders that applies even in a sale of the company, and that recognizes that corporations are dependent on stakeholders for success and have a corresponding responsibility to stakeholders, has been demonstrated to be consistent with a high-functioning economy. By highlighting the Dutch system, however, I do not mean to claim that it is unique. For policymakers who are considering the merits of a stakeholder-based governance model, the Dutch system should be seen as one example among many corporate governance systems in successful market economies (such as Germany) that embrace this form of stakeholder-based governance. There is likely no one-size-fits-all approach; each jurisdiction should find the tailor-made model that works best for it, like perhaps the introduction of the corporate purpose in the UK and France. In any event, there is a great benefit in exchanging ideas and learning from experiences in different jurisdictions to find common ground and best practices in order to increase the acceptance and appreciation of stakeholder-oriented governance models.

US governance practices have been, and are, influential around the world. In the 2000s the pendulum in developed countries, including to some extent in the Netherlands, clearly swung in the direction of shareholder-centric governance as championed in the US. In the current environment, if the US system’s focus on shareholders is not adjusted to protect stakeholder interests, it may over time perhaps become an outlier among many of the world’s leading market economies that in one way or the other have adopted a stakeholder approach. Adjustment towards stakeholder governance seems certainly possible in the US, for example through the emerging model of corporate governance, the Delaware Public Benefit Corporation. The benefit corporation seems to have many if not all of the key attributes of the Dutch system and could provide a promising path forward if American corporate governance is to change in a way that makes the US model truly focused on the long-term value for all stakeholders. The question for US advocates of stakeholder governance is whether they will embrace it, or adopt another effective governance change, and make their commitment to respect stakeholders rea

Notre membre de l’équipe et doctorant en cotutelle (Université Laval-Université de Perpignan), Alexis Langenfeld, a obtenu au printemps 2020 une prestigiueuse bourse FRQ-SC pour appuyer la réalisation de sa thèse.

Pour ceux et celles intéressés, son projet de thèse porte sur le sujet suivant : « Responsabilisation des groupes de sociétés et enjeux de RSE ».

Mise en perspective de son sujet :

Aucune obligation juridique ne pèse sur les groupes en tant que tels. En effet, ils ne sont pas reconnus comme des sujets de droit. Or, bien que le droit ignore le groupe de sociétés en tant que personne, économiquement ces structures forment souvent une seule entité dont les activités donnent naissance à des externalités positives (les gains) et négatives (les dommages) . Cette entité est l’entreprise, laquelle n’est pas réellement définie par le droit. Pire, elle est « hors-la-loi » dès lors qu’il s’agit de la sanctionner (…). Or, juridiquement un groupe est constitué d’une multiplicité de sociétés par actions dont les deux caractéristiques principales sont l’autonomie des personnes morales et la responsabilité personnelle des sociétés (…). Ainsi, le droit considère classiquement qu’aucune société membre d’un groupe ne peut voir sa responsabilité engagée pour celui-ci, par exemple en cas de dommage. Conséquemment, cette vision des groupes interroge la capacité du droit à responsabiliser l’entreprise constituée en groupe. Pourtant, même observés sous le prisme juridique, les groupes constituent une unité économique formée par une combinaison de sociétés par actions et doté d’une animation commune sous l’impulsion de la société du groupe détenant le pouvoir : la société tête de groupe (ou société-mère). L’encadrement des groupes de sociétés est, de ce fait, l’un des domaines les plus complexes du droit des affaires (…) et lui pose un véritable défi (…). Les solutions à apporter ne sont en rien évidentes, surtout étant donné que la responsabilité limitée présente à certains égards des avantages (…).

Comment les outils de la RSE couplés à une nouvelle compréhension par le droit de la dynamique des groupes de sociétés (à laquelle la RSE participe) peuvent contribuer à une responsabilisation de ces derniers ? En d’autres mots, de quelle manière le droit contemporain peut réconcilier pouvoir et responsabilité au sein des groupes ?

L’objectif général de la thèse d’Alexis n’est rien de moins que de construire une théorie de la responsabilisation des groupes. À cette fin, il entend démontrer que, si la personnalité morale ne constitue pas un obstacle à la responsabilisation des groupes de société, celle-ci doit être dépassée au moyen de nouveaux concepts. Par la suite, Alexis va établir que la conceptualisation de ces nouveaux concepts nécessite d’avoir recours aux outils normatifs de la RSE.

Quand on connaît la difficulté d’obtenir de telles bourses (6 bourses attribuées seulement dans le programme étudiant international), cela pose le bonhomme (on me pardonnera l’expression !). En tous les cas, c’est une chance unique de le codiriger et un plaisir !

Beau rapport de Vitor Gaspar, Paulo Medas, John Ralyea, Les entreprises publiques à l’ère de la COVID-19 (Fonds Monétaire International, 7 mai 2020). Une belle manière de situer les entreprises publiques sur l’échiquier économique et de mieux comprendre pourquoi la gouvernance de l’entreprise doit être comprise avec l’entreprise publique !

Extrait :

Dans le plus récent Moniteur des finances publiques, nous nous penchons sur ces entreprises publiques. Comment ont-elles évolué au cours des dernières décennies ? Comment les pays peuvent-ils en tirer le maximum ? Dans un scénario idéal, elles aident les pays à atteindre leurs objectifs économiques et sociaux. Dans le scénario du pire, elles doivent être secourues à grands frais par l’État et freinent la croissance économique. Tout dépend de la qualité de leur gouvernance et de leur responsabilisation.

(…)

Les rapports entre les États et les entreprises publiques ne vont pas toujours de soi. Les États confient à ces entreprises des objectifs ou des mandats précis : distribuer l’eau potable ou l’électricité, ou construire des routes que le secteur privé ne jugerait pas rentables. Cependant, il arrive souvent que ces mandats ne soient pas suffisamment financés, ce qui a des conséquences pour la population. Les entreprises publiques ne sont pas à la hauteur dans de nombreux pays en développement où plus de 2 milliards de personnes n’ont pas accès à un approvisionnement en eau potable sûr et plus de 0,8 milliard de personnes, à une source fiable d’électricité.

Les banques publiques sont un autre exemple. Certains pays comme le Brésil, le Canada, l’Allemagne et l’Inde ont récemment demandé aux banques publiques de participer aux efforts déployés pour atténuer les retombées de la pandémie. Pourtant, les antécédents de nombreuses banques publiques au chapitre du développement économique (leur principal objectif) sont peu convaincants, car elles prennent parfois des risques excessifs, ce qui accroît la vulnérabilité des économies et des populations à d’éventuelles crises.

La surveillance des entreprises publiques est aussi problématique. Nombre de pays ne possèdent simplement pas la capacité requise. L’opacité des activités des banques et autres entreprises publiques demeure un obstacle à la responsabilisation et à la surveillance, et rend possibles l’accumulation et la dissimulation de dettes considérables que les États doivent ensuite éponger, à des coûts qui dépassent parfois 10 % du PIB.

(…)

À une époque où les États doivent répondre à des besoins croissants tout en composant avec une dette élevée, le principe fondamental des entreprises publiques devrait être d’éviter le gaspillage de ressources publiques. Voici quatre recommandations à l’intention des pays soucieux d’améliorer les résultats de leurs entreprises publiques :

Il convient de réévaluer périodiquement la pertinence des entreprises publiques pour s’assurer que les contribuables en obtiennent pour leur argent. L’Allemagne, notamment, procède à des examens biennaux. La raison d’être des entreprises publiques dans les secteurs concurrentiels, comme le secteur manufacturier, est douteuse, car les entreprises privées sont en général plus efficientes lorsqu’il est question de fournir de produits et de services.

Les pays doivent encourager les gestionnaires à accroître leur rendement et inciter les organismes compétents à bien surveiller les entreprises publiques. La transparence totale de ces dernières est essentielle au renforcement de leur responsabilisation et à la réduction de la corruption. L’intégration de ces entreprises dans les objectifs relatifs au solde budgétaire et à la dette encouragerait davantage la discipline budgétaire. Certains pays, comme la Nouvelle-Zélande, ont déjà mis en place plusieurs éléments de ces pratiques.

Les États doivent aussi doter les entreprises publiques de moyens financiers suffisants pour s’acquitter de leur mandat économique et social, comme en Suède. Cet aspect est fondamental en situation de crise, car les banques publiques et les entreprises de services publics disposent alors des ressources nécessaires pour, entre autres, subventionner l’octroi de prêts et la distribution d’eau et d’électricité pendant une crise comme l’actuelle pandémie, et promouvoir des objectifs de développement.

La création de conditions de concurrence équitables entre les entreprises publiques et les entreprises privées aurait aussi des effets positifs, car elle favoriserait les gains de productivité et freinerait les velléités protectionnistes. Certains pays, notamment l’Australie et ceux de l’Union européenne, limitent déjà le traitement préférentiel accordé aux entreprises publiques. À l’échelle mondiale, il serait probablement possible de s’entendre sur des principes généraux qui encadreraient le comportement international des entreprises publiques.

Hier, le plus grand d’investissement au monde (BlackRock) a posté sur son site Internet son rapport sur son approche en matière de durabilité : « Our approach to sustainability ».

Extrait :

This past January, BlackRock wrote to clients about how we are making sustainability central to the way we invest, manage risk, and execute our stewardship responsibilities……Our efforts around sustainability, as with all our investment stewardship activities, seek to promote governance practices that help create long-term shareholder value for our clients, the vast majority of whom are investing for long-term goals such as retirement. This reflects our approach to sustainability across BlackRock’s investment processes, in which we use Environmental, Social, and Governance factors in order to provide clients with better risk-adjusted returns, in keeping with both our fiduciary duty and the range of regulatory requirements around the world. As a result, we have a responsibility to our clients to make sure companies are adequately managing and disclosing sustainability-related risks, and to hold them accountable if they are not.

(…) While this report focuses on climate-related issues, our investment stewardship approach to sustainability is much broader. It encompasses other environmental issues, such as sustainable practices in agribusiness. Our stewardship also includes topics that have been central to many companies’ license to operate, particularly over the past few months, such as human capital management and diversity and inclusion. The COVID-19 crisis, and more recently the protests surrounding racial injustice in the United States and elsewhere, have underscored the importance of these issues and a company’s commitment to serving all of its stakeholders.

(…) In January, we asked companies to publish disclosure aligned with the Sustainability Accounting Standards Board (SASB) standards, which includes disclosing the racial and ethnic profile of their U.S. workforce. In the second half of 2020, as we assess the impact of companies’ response to COVID-19 and associated issues of racial equality, we will be refreshing our expectations for human capital management and how companies pursue sustainable business practices that support their license to operate more broadly. We also will continue to emphasize the importance of diversity in the board room and will consider race, ethnicity, and gender as we review a company’s directors.

Dans l’Harvard Law School Forum on Corporate Governance, un article intéressant – et court – apporte un bel éclairage sur la gestion des parties prenantes : « A Hierarchy of Stakeholder Needs » (de Sarah Keohane Williamson, FCLTGlobal, 22 juin 2020).

Extrait :

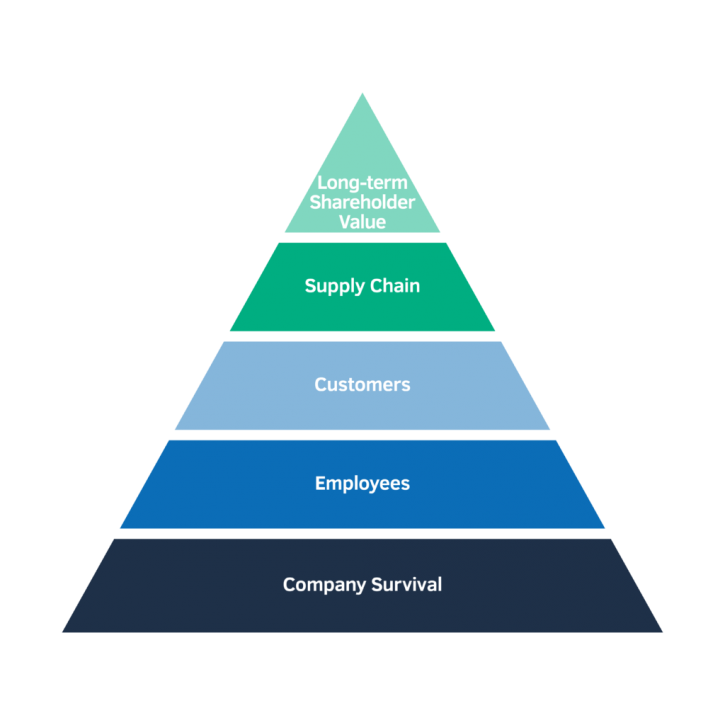

Amid the extraordinary circumstances and economic difficulties brought on by COVID-19, companies in 2020 are faced with decisions on how to best serve the many stakeholders that rely on them—customers, investors, suppliers, employees, and so on. Each group has its own distinct needs and contributions to the company’s overall success, and companies recognize that these groups build on each other to serve their purpose.

(…) Survival for the company itself represents the basic need of the hierarchy. A company’s first priority has to be ensuring it is resilient (and liquid) enough to outlast the crisis. If this need is not met, there are no employees, customers, or other stakeholders to serve. Hard decisions may have to be made to ensure the long-term survival of the enterprise that will affect other tiers of needs—closing stores, furloughing employees, or postponing dividends to investors. Once the basic need is met, however, and the company is a going concern, the company can reorient its focus.

Employees look to their employer for security in more ways than one—financial, to be sure, but also physical. Many companies addressed this area first in its response to COVID-19—89% of respondents to a recent FCLTGlobal survey indicated that employee health and safety was its top priority. (…)

Once the house is in order, customers’ needs can follow. Just as customers depend on a company’s products, the company relies on a consistent, repeatable client base to stay in operation. Like before, this tier is dependent on the one that precedes it—if there were no company, or no employees to keep it running, there would be no customers to serve.

(…) Once customers’ needs are met and business can continue, the supply chain must be maintained. COVID-19 has presented a real challenge in terms of supply for many companies, particularly when sourcing products from countries that are in strict lockdowns.

(…) Then, finally, the company is able to achieve long-term value for its shareholders. Meeting the preceding needs—viability through liquidity, employee wellbeing, extraordinary customer care, and supply chain continuity—may have resulted in near-term shortfalls for shareholders by way of lower earnings or a temporary pause in issuing dividends.

À leur habitude, Sophie-Emmanuelle Chebin et Joanne Desjardins offrent un billet très intéressant : faut-il faire la place à une célébrité dans son CA ? (« Vedettes au CA: une pratique qui suscite l’intérêt! », Les affaires.com, 8 juillet 2020) Une belle question que je ne m’étais pas posée tant je crois davantage dans la compétence qu’à la notoriété. Toutefois, leur billet me fait réfléchir…

Extrait :

Voici quelques recommandations pour tirer le meilleur parti de ces additions au sein du CA :

Gérer les attentes de part et d’autre

Il est essentiel d’avoir les discussions d’usage sur l’intérêt et la disponibilité de cette personne pour la charge d’administrateur. Personne ne veut d’un administrateur fantôme au sein de son CA, peu importe que cette personne soit connue ou non !

Il est aussi recommandé de clarifier auprès de l’administratrice vedette son rôle et les attentes quant à sa contribution. Sera-t-elle ambassadrice de l’organisation ou jouera-t-elle un rôle plus effacé sur la place publique? Devra-t-elle partager son réseau? Il est aussi crucial d’aborder la question des prises de position publiques de cette personnalité dans l’espace médiatique. Sans la museler, il faudrait éviter que ses prises de positions publiques portent ombrage à la réputation de l’entreprise et de sa marque.

En s’assurant que les attentes du CA et celles de l’administratrice sont alignées, on maximise les chances de bâtir une relation fructueuse et durable.

Mettre à profit leurs compétences

Comme pour tout administrateur, il est essentiel de mettre en valeur les compétences uniques de cette personne pour l’engager dans les travaux du CA. Révélée au monde pour son interprétation du personnage d’Hermione Granger dans l’adaptation cinématographique de la saga « Harry Potter », ce sont les prises de position d’Emma Watson à l’égard de la mode éthique qui lui ont valu d’être nommée présidente du comité de développement durable de Kering, compagnie mère de Gucci.

La dynamique au CA

La présence d’une personnalité publique au sein du CA peut modifier la dynamique des discussions. Le grand défi pour ces administrateurs est de ne pas asphyxier les réflexions des CA que l’on souhaite larges et inclusives. Parmi les autres administrateurs, personne n’est à l’abri d’être groupie, d’être subjugués par les prises de positions de cette personne ou de devenir moins expressif de peur du jugement de cette personnalité connue. Aussi, il faut être à l’affût de l’impact que cette nouvelle personne peut avoir sur les débats du CA.